BTE Newsletter #28: "Retail Private Credit? We hardly even do that at all."

Good morning everyone, Happy Tuesday.

First, a bit of a changeup: rather than hosting, I recently appeared on someone else's podcast.

John De Goey is another advisor at Designed Securities, and to my knowledge he's the only other Designed advisor besides me with a podcast. His is called Make Better Wealth Decisions, featuring interviews with a wide array of thought leaders in the wealth management space, and it's certainly worth a follow. I was fortunate enough to join him for a high-level overview of Private Markets for individual investors. You can listen to it on Apple or Spotify ... or you can see the video version on Youtube.

Meanwhile, earnings season is now effectively complete for the alternative asset managers, and a big focus was on the issues facing Private Credit (Direct Lending) in the retail space (which of course has also been a big focus of this newsletter). More specifically, the managers were very intentional in downplaying the role of this market in their growth plans, which they had not been doing in their previous earnings calls. They were able to do this largely because results in other areas of their businesses were largely unaffected by the noise. Below we take a closer look.

Ben

The Big Takeaways From Earnings Season

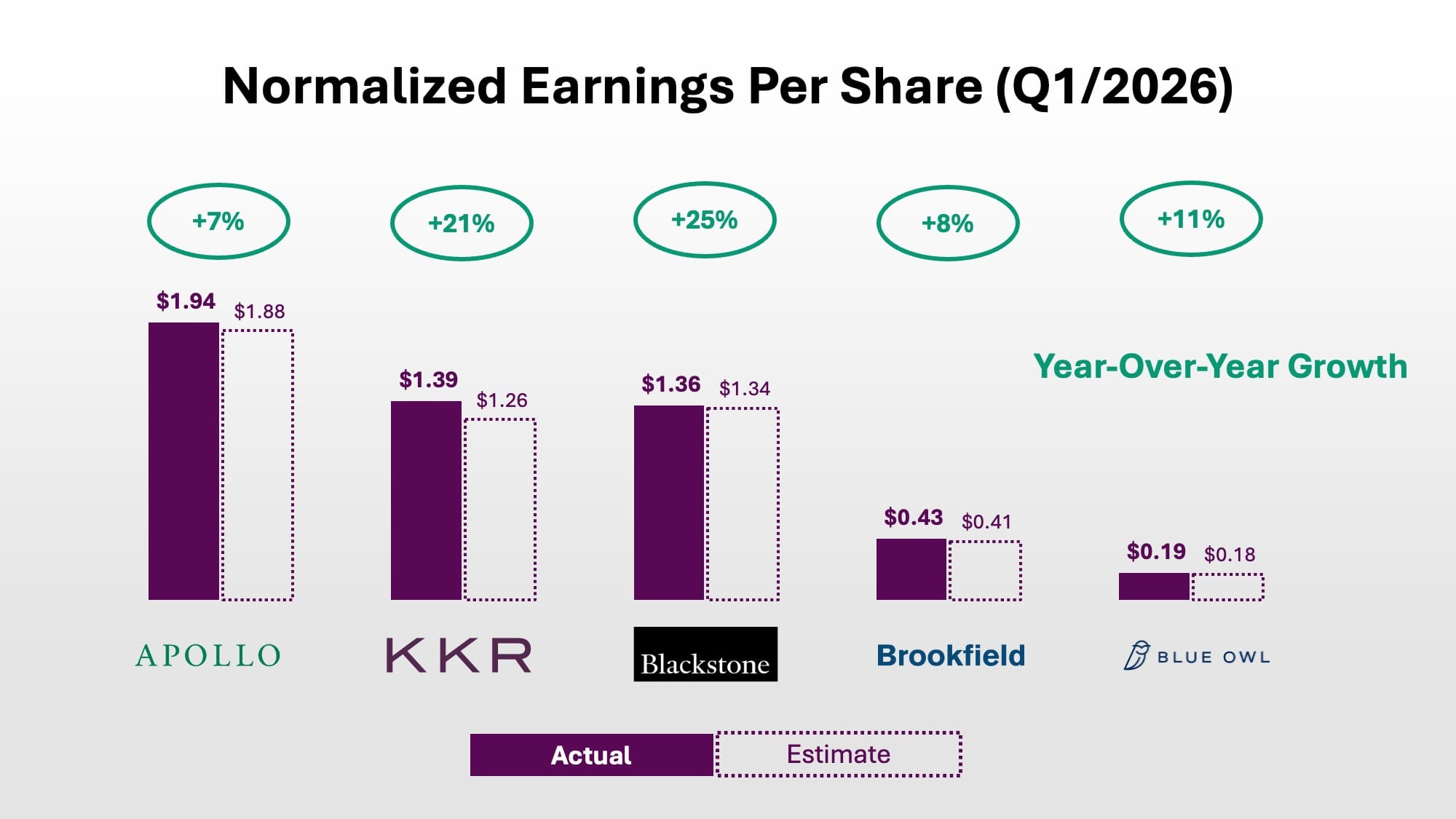

With substantially all of the alternative asset managers having reported earnings, the quarter could broadly be characterized as a relief. The industry has not had a year to remember so far, with negative headlines, redemption queues, and falling share prices. Yet the major managers generally beat earnings estimates and showed healthy year-over-year growth as well.

In terms of presentation tone, a couple of clear themes emerged. First, firms notably downplayed the role of retail Direct Lending, a big shift from last year.

Second, managers emphasized the strength of other strategies, which continue to raise capital despite redemption queues and negative press surrounding retail Direct Lending.

This distinction may be the most important takeaway from the quarter, particularly for Blue Owl. Retail Direct Lending represents a larger portion of its business relative to peers and has faced more acute pressure. In that context, it is not surprising that the company’s shares responded most positively to the earnings results.

Downplaying the Role of Retail Direct Lending

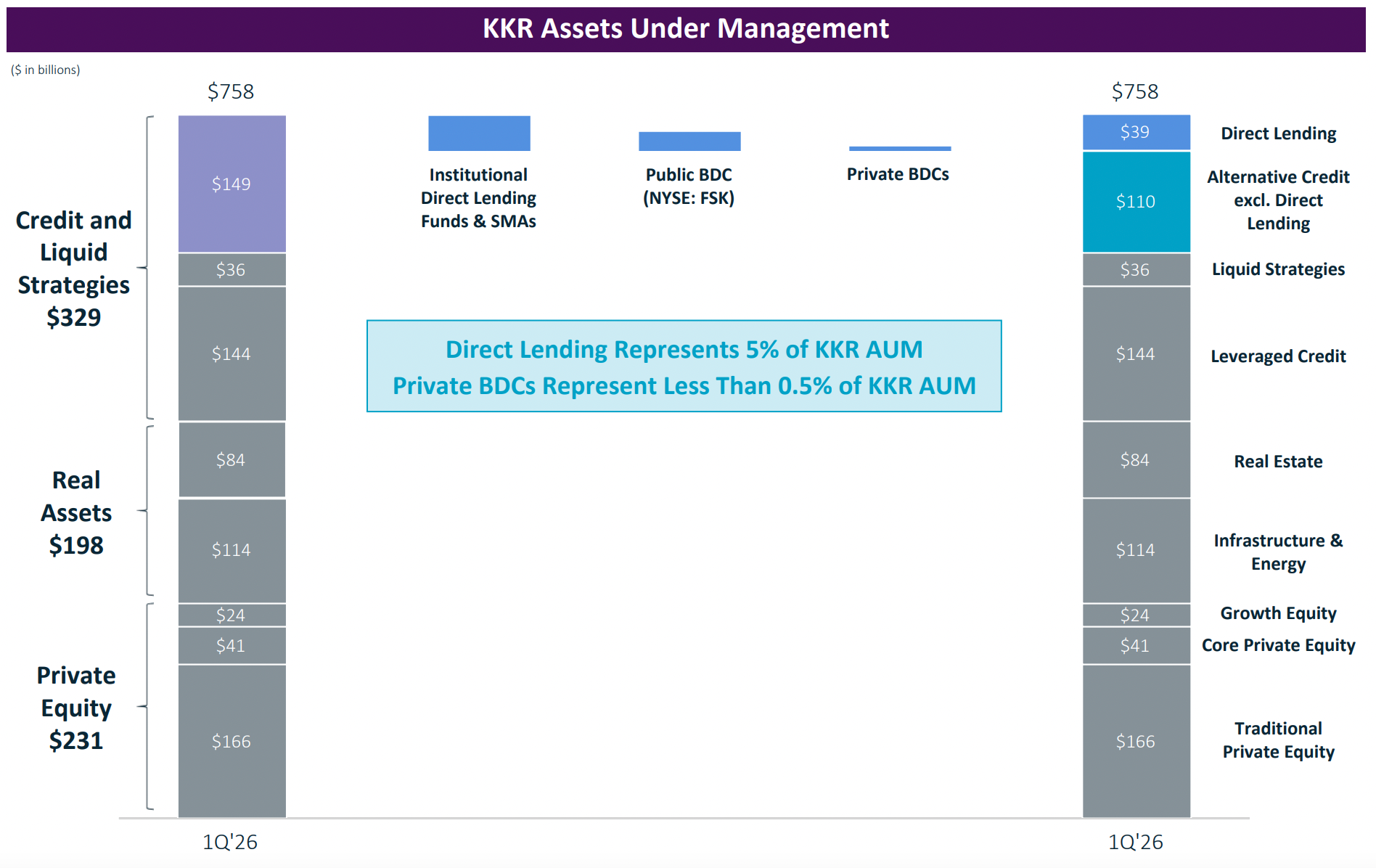

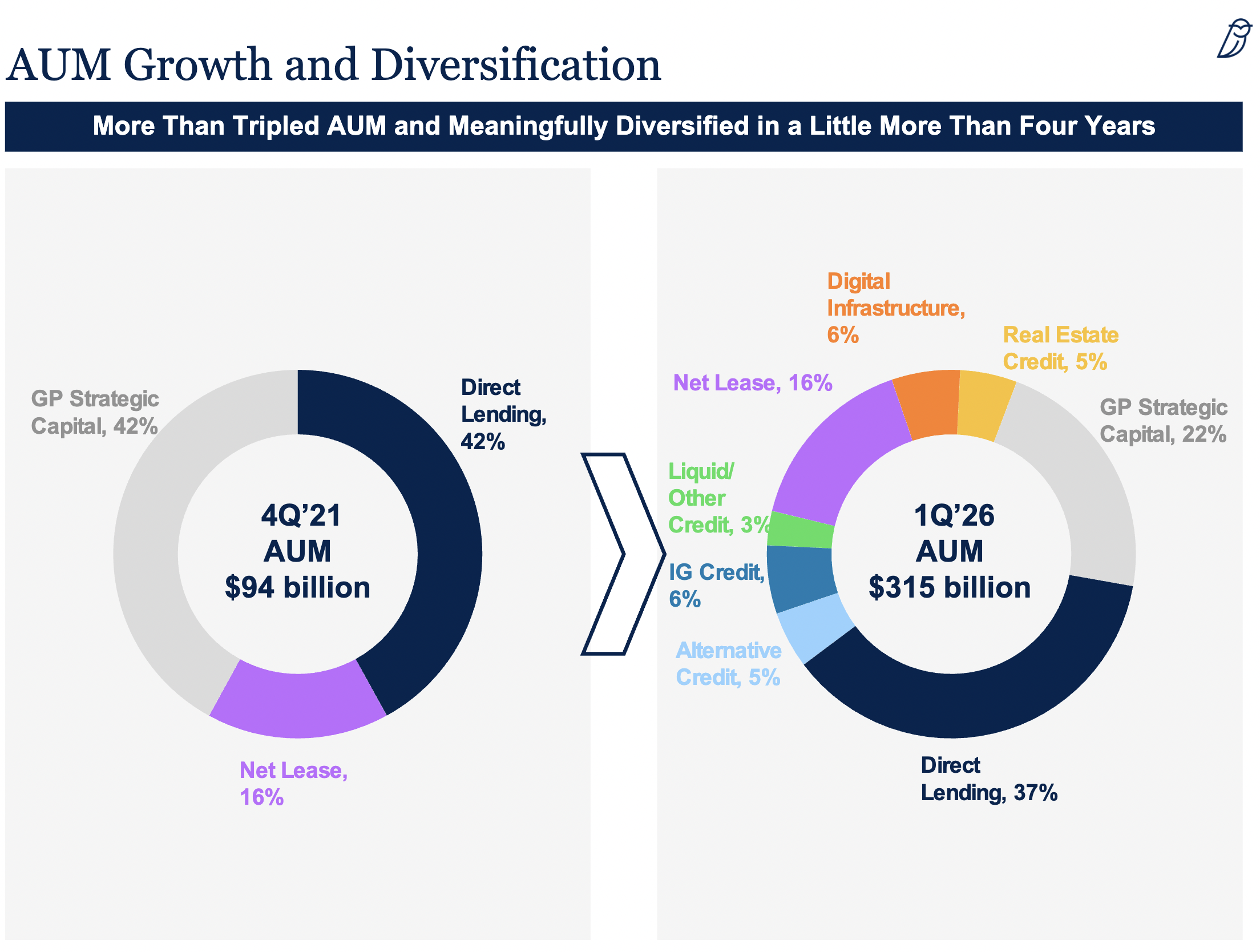

This was the first quarterly results cycle since redemption queues began building up in retail Direct Lending products (if anyone wants to catch up on the subject, I wrote about it here). So it was unsurprising, but still notable, how much the tone of the presentations shifted relative to last year, especially for Blackstone, KKR and Blue Owl. Blue Owl and KKR went as far as adding new slides to highlight the diversification of their platforms:

One could also look at how the firms spoke about their results to get a sense of the shift:

Blackstone:

Q4/2025:

"In Q4, our total sales in the channel exceeded $11 billion, up 50% year-over-year. BCRED [the flagship retail Direct Lending product] led the way with gross sales of $3.3 billion, while net inflows were $1.2 billion. For the full year, BCRED reported record gross sales of over $14 billion."

- President Jonathan Gray

Q1/2026:

"Despite the external noise, our institutional and insurance clients, who represent 75% of our credit platform AUM, have continued to commit large-scale capital to the asset class."

- CEO Steve Schwarzman

KKR:

Q3/2025:

"So $32 billion out of $720-some-odd billion is obviously a relatively small percentage. But we're kind of in the top of the first inning around private wealth. The vehicles that we have, we have vehicles today across all 4 of our major products. So private equity, real estate, infrastructure and credit. But we're seeing really rapid growth. It's ahead of what we thought it would be."

- CEO Scott Nuttall

Q1/2026:

"In total, direct lending is $39 billion or 5% of our AUM. It's an important business for us, but in the framework of KKR, it's of modest size. And with a lot of focus on redemption activity in the wealth space, we note the size of our private BDC footprint in the second bar from the right. It's even smaller, around $3 billion of AUM or 0.4% of our AUM in total."

- Craig Larson, Head of Investor Relations

Blue Owl:

Q3/2025:

"In credit, we raised $5.6 billion, a near record quarter for our credit platform. $3 billion was raised in direct lending of which $2.4 billion came from our non-traded BDCs, OCIC, and OTIC."

- CFO Alan Kirshenbaum

Q1/2026:

"As a reminder, these 2 funds collectively [OCIC and OTIC] comprise less than 17% of our total AUM."

- Co-CEO Marc Lipschultz

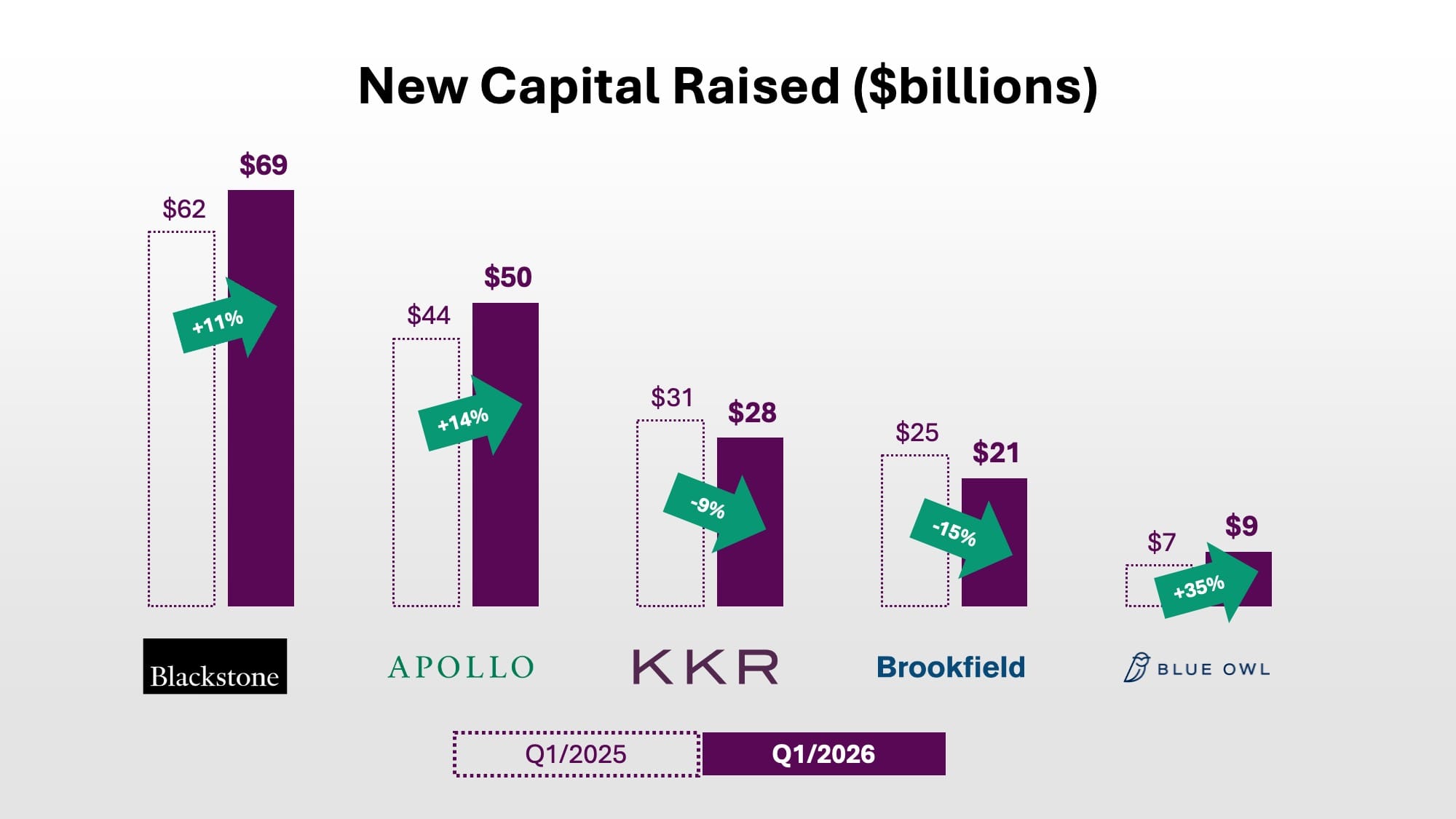

Solid Fundraising In Other Strategies

Part of the reason the firms were highlighting their diversity was the fact that other strategies were largely unaffected; they were still able to generate solid fundraising numbers, and the issues with retail Direct Lending (so far) appear to be isolated. Of those same five firms, three reported solid growth in fundraising year-over-year, while the other two were fundraising for big strategies the year prior (Americas Private Equity at KKR, Real Estate at Brookfield).

The tone was notably upbeat. Even within Direct Lending, managers highlighted growing interest from institutional investors who view the current environment as a contrarian opportunity. With less capital flowing into the space than in prior years, spreads have begun to widen, particularly in areas like software lending. Of course it's far too soon for the alternative asset managers to declare victory, but the fundraising trends certainly could have been a lot worse this quarter.

Back to Reality

In many ways, this quarter marked the first real opportunity for alternative asset managers to respond to the wave of negative press facing the industry. Broadly speaking, the results came in far stronger than the headlines would suggest. Investment performance, fundraising, and profitability have all trended positively over the past decade, and a single quarter of redemption pressure and negative sentiment in one segment did not change those underlying fundamentals.

That said, the more important question is whether this marks a temporary dislocation or the early stages of a more challenging operating environment. Time will tell.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/