BTE Newsletter #34: Discount Retailers, Wind Turbines, Data Centres, and Preschool

Good morning everyone, and Happy Tuesday.

First things first: there will be no Beyond The Exchange newsletter next week. Happy Canada Day! And to my American readers, Happy July 4th as well.

Last week featured a couple notable events. One was the iCapital Engage+ Toronto event, in which I hosted a panel on Private Credit. Certainly there was no shortage of topics to discuss, including the new underwriting environment, the idea of Private Credit trading daily, and the increase in redemptions from retail investors this year. Regarding that last subject, I'll have more to say on the matter after the major managers report the latest figures.

The other notable event was my (first) webinar on Private Markets for individual investors. For those of you who missed it, the good news is that the event was recorded. I won't be publishing the recording on this site, but anyone interested can click here to request it via email.

Part of the webinar was a look at four different investments within the Private Markets funds. The case studies really help illustrate what the strategies look to accomplish, so they were certainly worth highlighting on the webinar. For the same reason, they are worthy of a newsletter issue too.

Ben

A Look At Four Different Investments in Private Markets

Private Markets are often thought of as very niche, obscure, or complicated (pick your adjective), and there are other perceptions that apply to each of the strategies.

For instance Private Equity is often thought of as a ruthless business, one in which a manager buys a company, fires half the workforce, sells a bunch of assets, raises prices, and profits at the expense of everyone else. In Private Credit, there's a perception that only bad companies borrow from the Private Markets, since the good ones go to banks or the public markets. In Real Estate, some people automatically associate the asset class with apartment buildings, not knowing about other strategies. As for Private Infrastructure, I encounter people all the time who don't know it's an asset class.

So with that said, the four investments below all sit within Private Markets funds available to Canadian individuals (and on the approved product shelf at my firm, Designed Securities). And they certainly help dispel some of these perceptions.

Private Equity: Action

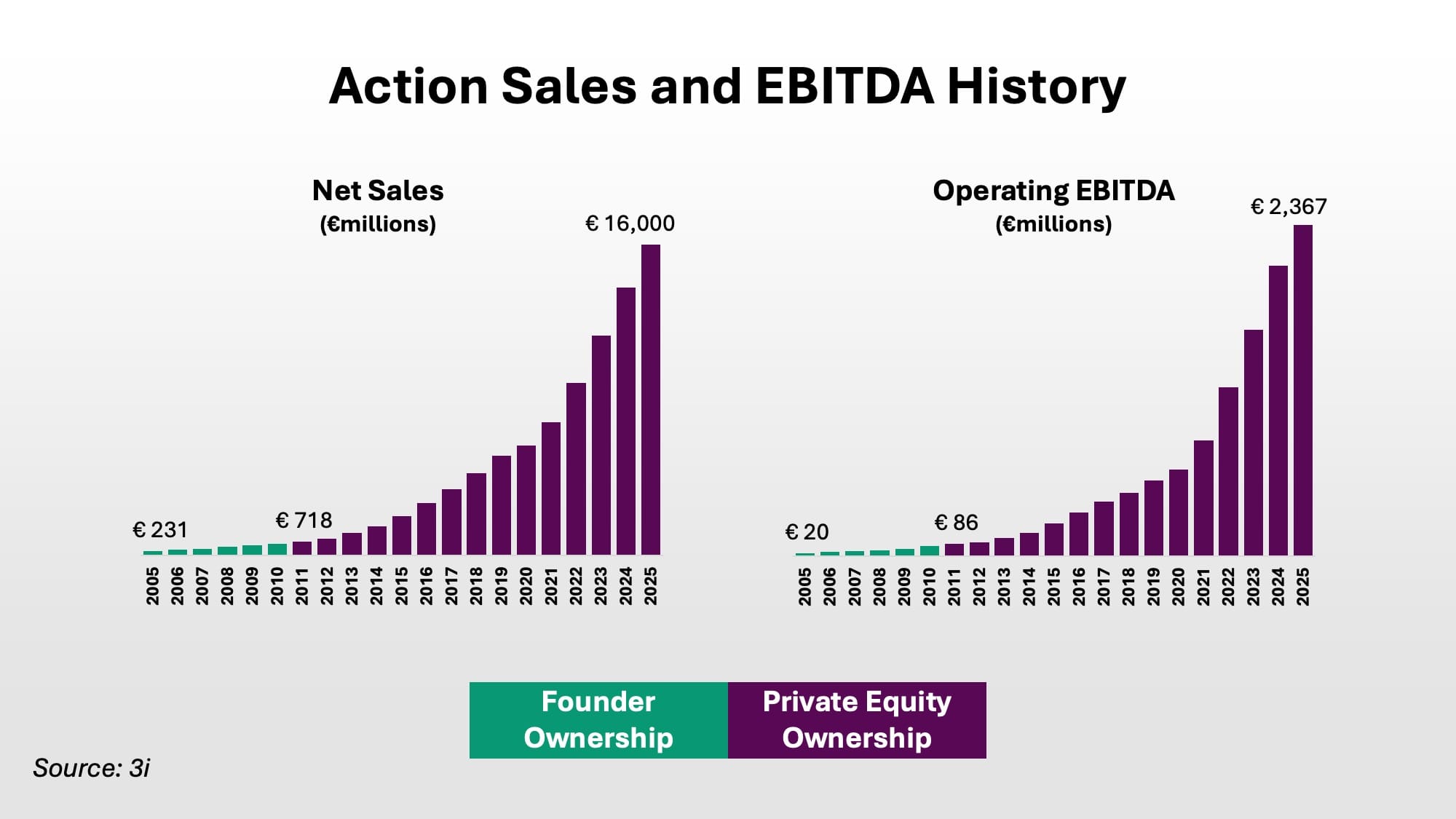

Founded in 1993, Action is a leading discount retailer in continental Europe, with 3,300 stores across 14 countries. In many ways, the company can be thought of as the Dollarama of Europe, as 2/3 of Action's products are priced below €2.

Any investor in Dollarama can appreciate that discount retail can be a fantastic business, especially for the largest players. Costs are very minimal to open a new store, since there's not much need beyond basic shelving. Marketing costs are practically nil as well. The business is very resilient to recessions, since the low prices are more compelling to shoppers when budgets are tight. Larger players benefit from stronger purchasing power, and the business is quite repeatable; it's just a matter of opening more stores.

Private Equity firm 3i bought a majority stake in Action from its founders in 2011, and has overseen substantial growth at the retailer since then. In fact the Action investment has been the defining event in 3i's history, now accounting for about three quarters of the Private Equity firm's investment portfolio.

Action has never been entirely owned by 3i, and one of the smaller co-investors is Neuberger Berman, whose Global Private Equity Access Fund is available to Canadians. Action is the largest investment within that fund.

To be fair, Action is one of Private Equity's clear success stories, and most investments do not work out nearly so well. But it does highlight what Private Equity typically seeks to accomplish, which is not centred on ruthless cost-cutting, indiscriminate price hikes, or other short-term behaviour.

Private Infrastructure: Exus Renewables

Opinions on renewable energy fluctuate wildly with the political environment, but there are some aspects of the asset class that everyone most people can agree on.

For starters, the cost of renewables has fallen drastically, to the point where it is often the most economical form of power production. Secondly, it is a very repeatable business; building another solar panel on another solar field is easier than building a nuclear power plant from scratch. Power generation of any type tends to have a very stable revenue profile. Meanwhile the growth of AI, data centres, and cloud computing are leading to a strong increase in the demand for power.

Exus Renewables builds, owns, and operates renewable energy assets across both Europe and North America, while also providing asset management services to third party renewables operators. Swiss-based asset manager Partners Group announced an investment into Exus in 2023, and has played a major part in the firm's geographic expansion, as well as a new initiative called Exus Digital to work more closely with Data Centres.

It's too early to gauge the success of this investment, but it's already clear Exus is a clear example of what Private Infrastructure seeks to accomplish: devoting capital towards mission-critical assets with stable revenue profiles and long-term growth tailwinds. The strategy typically targets a low-double digit net return profile, which can be very appealing for assets with a clear element of downside protection (although whether individual managers achieve this return is another question).

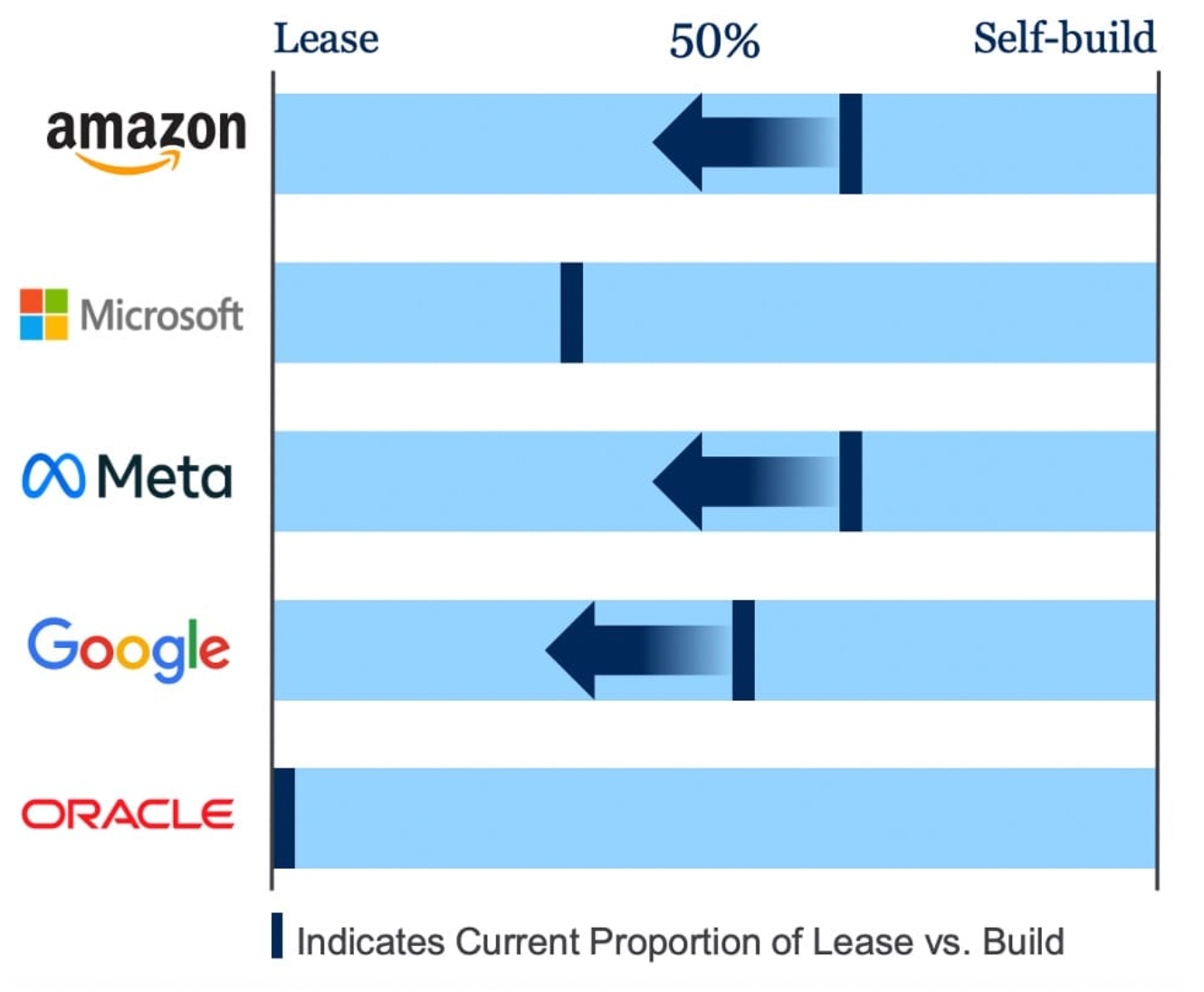

Private Real Estate: Data Centre Partnership in Abilene Texas

In one of my first posts, I looked at why Private Markets are an ideal funding source for digital assets such as data centres. In summary, banks and public bonds markets don't have the same flexibility as private capital, and this flexibility is often what data centre projects require. Meanwhile the hyperscalers only have so much balance sheet capacity to fund the buildout, and for that reason there's a shift towards renting data centres.

In this case, Blue Owl is partnering with a couple other firms, Crusoe and Primary Digital Infrastructure, to build a data centre in Abilene Texas. The scale is immense; there will be 8 buildings across a land area the size of Central Park, and the power available to it would be enough to power all the single family homes in Chicago.

The data centre is being leased to Oracle under a very long-term agreement, so from Blue Owl's perspective, as long as Oracle does not run into financial trouble, this asset should produce very steady cash flows for a long time. Even if Oracle does go bankrupt, then the data centre acts as a very strong source of collateral that could presumably be re-leased to another tenant. In the meantime, the tenant is responsible for maintenance, insurance, and property tax.

So one could think of this asset as a combination between Real Estate and Credit. And for an AI-themed investment, one could argue it's a lot more stable and predictable than the equity of an AI-focused company.

Private Credit: Cadence Education

Private education, particularly early education, can be thought of as an essential service for a lot of people. But ironically, in many ways the industry is still in its infancy. It's extremely fragmented, and sub-scale operators are not known for the latest and best business practices, such as the proper use of technology. Private Equity has thus seen an opportunity to consolidate and modernize this industry.

Cadence Education is one of the leading private operators of early childhood education centres in the United States, serving children aged 6 weeks to 12 years. Private equity firm Apax Partners acquired Cadence in 2020 from Morgan Stanley Capital Partners, and since then Cadence has grown from about 225 facilities to over 300.

The lead lender for this transaction is Blackstone, with a floating-rate loan that is yielding about 9% (as of the end of last year). Hamilton Lane is also one of the lenders (and its Senior Credit Opportunities fund is available at Designed). Presumably Apax could have gotten bank financing for this transaction, but Cadence is a very acquisitive company, so the flexibility of Private Credit is likely a material advantage, and a reason why Cadence is willing to pay a healthy rate on the debt. Apax also acquired Cadence right in the teeth of the pandemic, which may have inhibited the company's ability to get bank financing.

In any case, this is a good example of what Private Credit looks to achieve: lending at a healthy rate to resilient businesses that benefit from flexible capital.

This is not that complicated

While these are just four (cherry-picked) examples, they help illustrate what Private Markets has increasingly become. None of these investments are cases of financial engineering, nor are they roll-of-the-dice bets. They are not looking to make an extra dollar at the expense of employees, customers, or the environment. They are not short-term focused. And one could argue they are not particularly complicated either.

It's true that other investments in Private Markets do not fit this mould; there's a big difference between the best and worst operators. But the same could be said about public markets and founder-led businesses too. Like any form of investing, success ultimately comes down to choosing the right people and the right assets.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/