BTE Newsletter #27: Maybe the Sky Isn't Falling After All

Good morning everyone, and Happy Tuesday once again.

First things first, regarding the podcast, I originally hoped to have the latest episode released on Sunday, featuring Ralph Desando of Yorkville Asset Management. Now I'm hoping to have it ready by later today or tomorrow. The good news is that the next two episodes are scheduled for May, and another two guests are interested in appearing afterwards. For those of you interested in listening to any past episodes, you can find them below. Also for those of you reading this in your email browser, newsletter subscribers can download transcripts for any episode here.

|

|

As for this week's newsletter, I originally hoped to write about Mark Carney's new sovereign wealth fund idea. I thought it would be great to break down the details, perhaps presenting the numbers in graphical form, as I normally like to do. But unfortunately, there aren't any real details to work with, so that will have to wait (if this made you laugh, I want you to know I'm not joking).

Luckily we're right in the middle of earnings season, so there's still plenty to talk about. This brings me back to my old job as an equity analyst, and I do miss the times when a company/stock I picked reported fantastic numbers, and I got to talk about it to the rest of the firm. As for the times when a company/stock I picked missed expectations, and the stock gapped down, and I had to explain what happened ... well, I don't miss that quite so much.

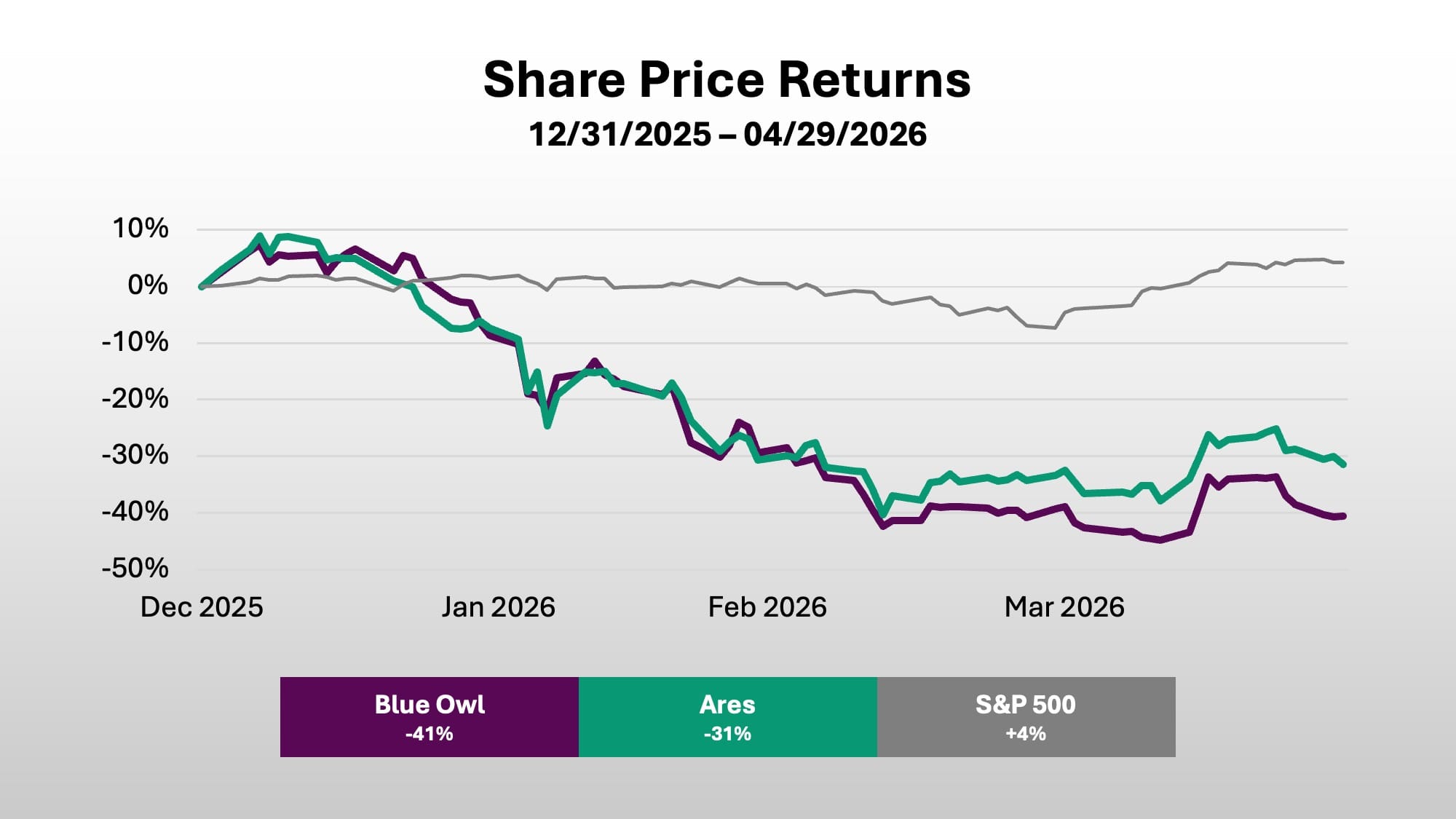

Regarding the alternative asset managers, Blue Owl reported earnings on Thursday and Ares reported on Friday. Both are known primarily for Private Credit, so sentiment was quite negative for each company going into the quarter. But as the title of this newsletter suggests, both were able to exceed their very low expectations.

Ben

A Closer Look at Ares and Blue Owl Results

The quarterly results from Ares and Blue Owl had a few things in common, starting with the sentiment heading into earnings. Both firms are closely associated with Private Credit, a strategy that has been under pressure from negative headlines, bearish forecasts, and rising redemption activity. That sentiment showed up clearly in their stock performance, with Ares down over 30% year-to-date prior to Thursday and Blue Owl down more than 40%.

Investor concerns are serious and quite straightforward. What if the Private Credit redemptions persist? What if retail outflows spread to institutional capital? What if Private Credit outflows spread to other strategies? And what would that mean for earnings power? Are these businesses entering a period of structural decline?

These fears were especially strong for Blue Owl, where a combination of PR missteps and its exposure to software lending have placed it at the centre of Private Credit anxiety.

One quarter alone will not fully resolve those concerns, but both firms did meaningfully steady investor sentiment. The results pointed to three key takeaways:

- These companies operate highly diversified platforms, both by strategy and by client base, with substantial institutional capital providing stability in the face of retail-driven redemptions.

- Outside of retail-oriented private credit, fundraising remained resilient. This suggests that recent headlines have not impaired brand strength or investor confidence to the degree the market had priced in.

- Growth metrics including AUM and distributable earnings remained quite strong, supported by continued inflows and the durability of locked-up capital.

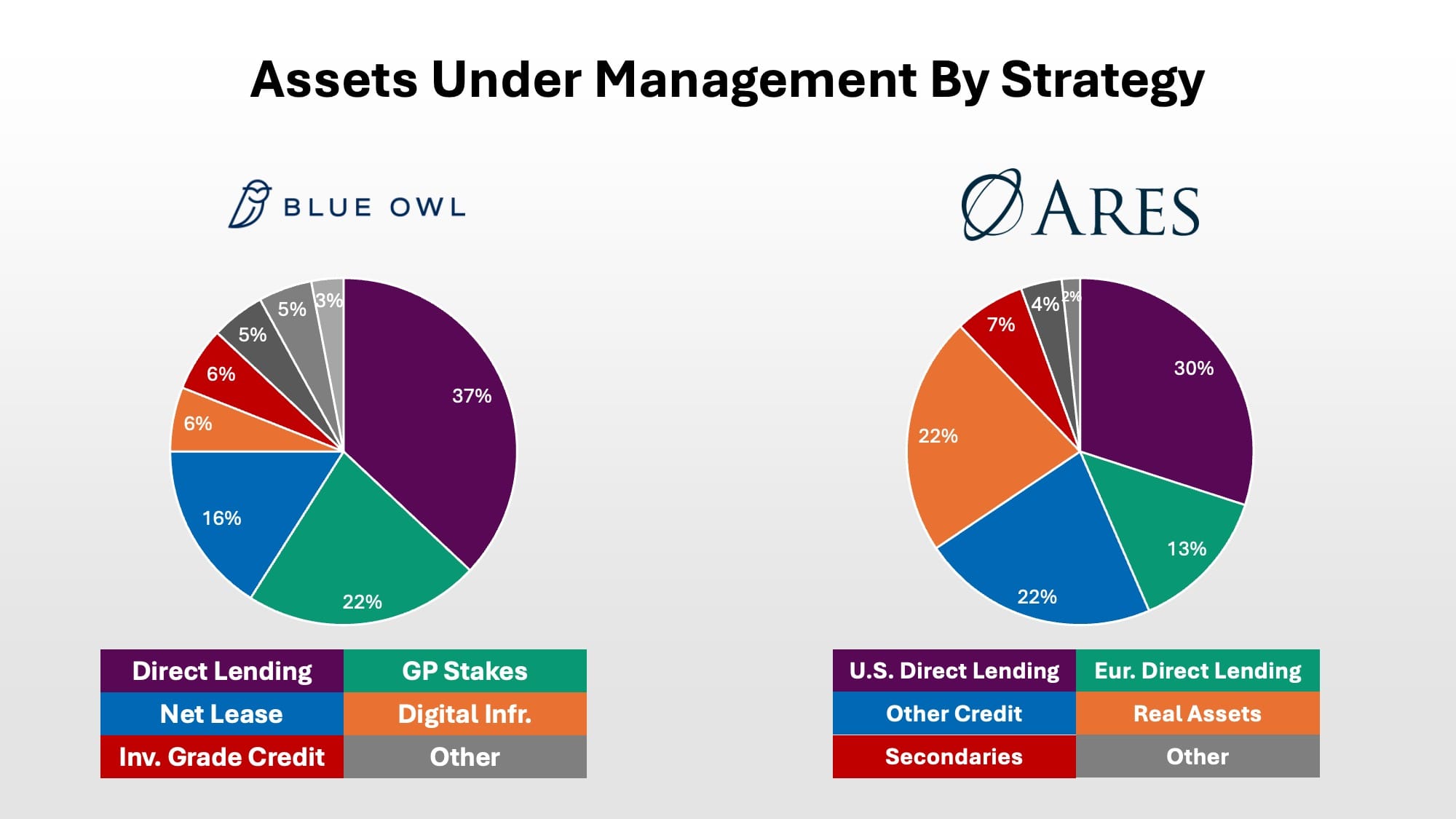

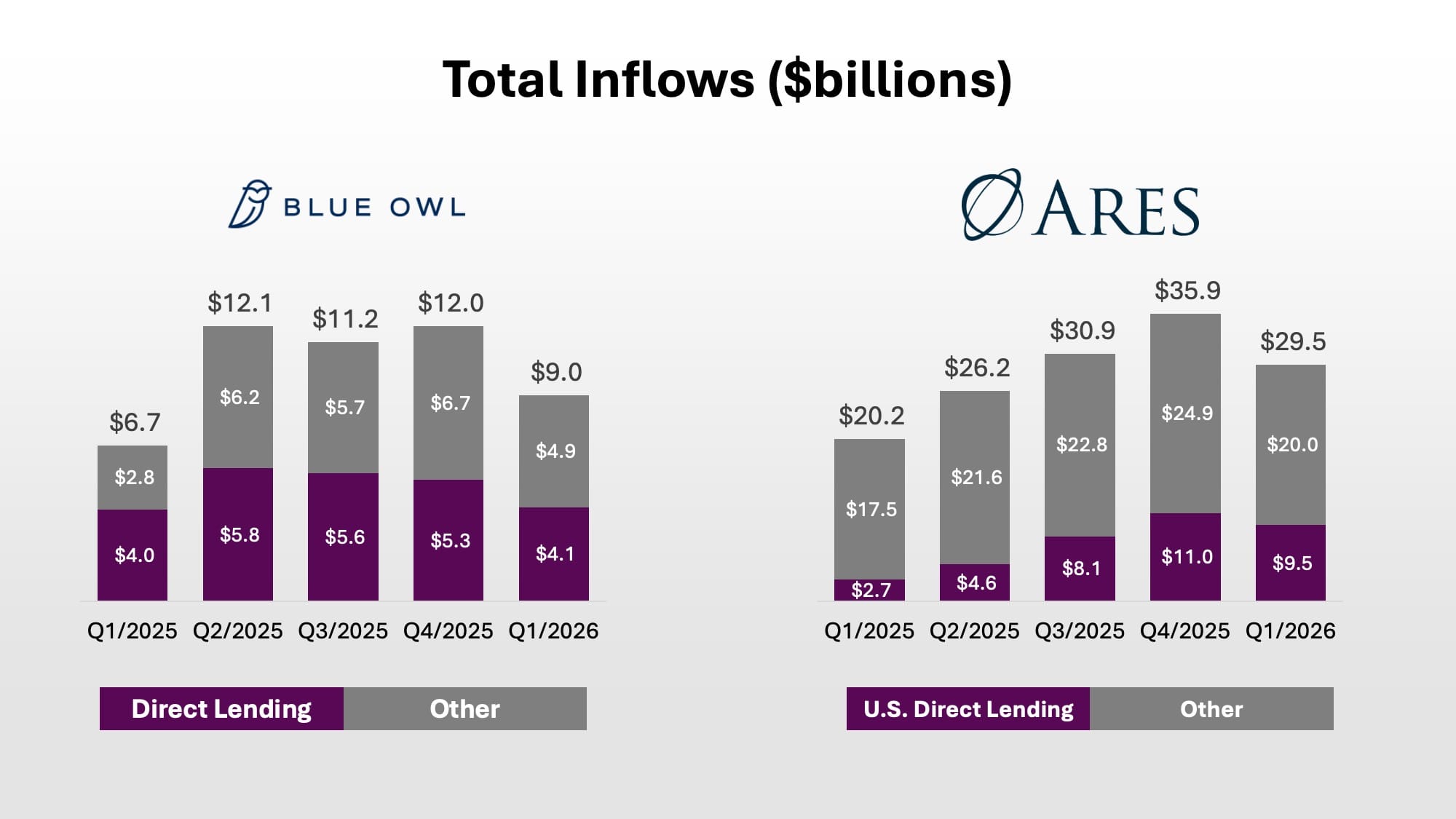

Takeaway #1: A Lot More Than Retail Direct Lending

When headlines highlight a surge in redemptions from certain funds, it's easy to assume that these products define the entire business for both Blue Owl and Ares. But in reality both companies operate far more diversified platforms.

The fact is, these redemption requests have come in retail-oriented Direct Lending funds, but not all of these firms' Direct Lending AUM is with retail investors. And both firms have lots of other strategies as well. In Ares' case, there is additional diversification by geography, with a meaningful Direct Lending business in Europe.

Putting this all together, the Direct Lending funds facing a wave of redemption requests account for a small minority of AUM at both companies. In Blue Owl's case, it's 17%. In Ares' case, it's 4.5%. And it was notable that both companies, for the first time in recent memory, were very explicit in downplaying the role of retail Direct Lending in their overall businesses.

Takeaway #2: Fundraising Is Still Strong

Judging by the headlines, you’d think these firms are in serious decline, especially Blue Owl. In its flagship direct lending fund (OCIC), redemption requests exceeded 20% of net asset value, while its tech-focused counterpart (OTIC) saw requests climb past 40% of NAV. Ares fared somewhat better, but even its flagship fund (ASIF) faced redemptions north of 10%.

In each case, actual redemptions were capped at 5%. Still, the situation raises some serious questions. Could negative sentiment among retail investors spill over to institutions? And does the current turmoil in Direct Lending risk contaminating other strategies?

One quarter does not make a trend, but so far the answer appears to be no. Fundraising totals, while down from the fourth quarter, were still well above year-ago levels. Outside of Direct Lending, fundraising showed no signs of losing momentum, including in other Private Credit strategies such as Asset-Backed Finance. Fundraising from institutional investors also showed little sign of slowing, even in Direct Lending, where clients see an opportunity to deploy capital into a market with wider spreads and therefore higher yields.

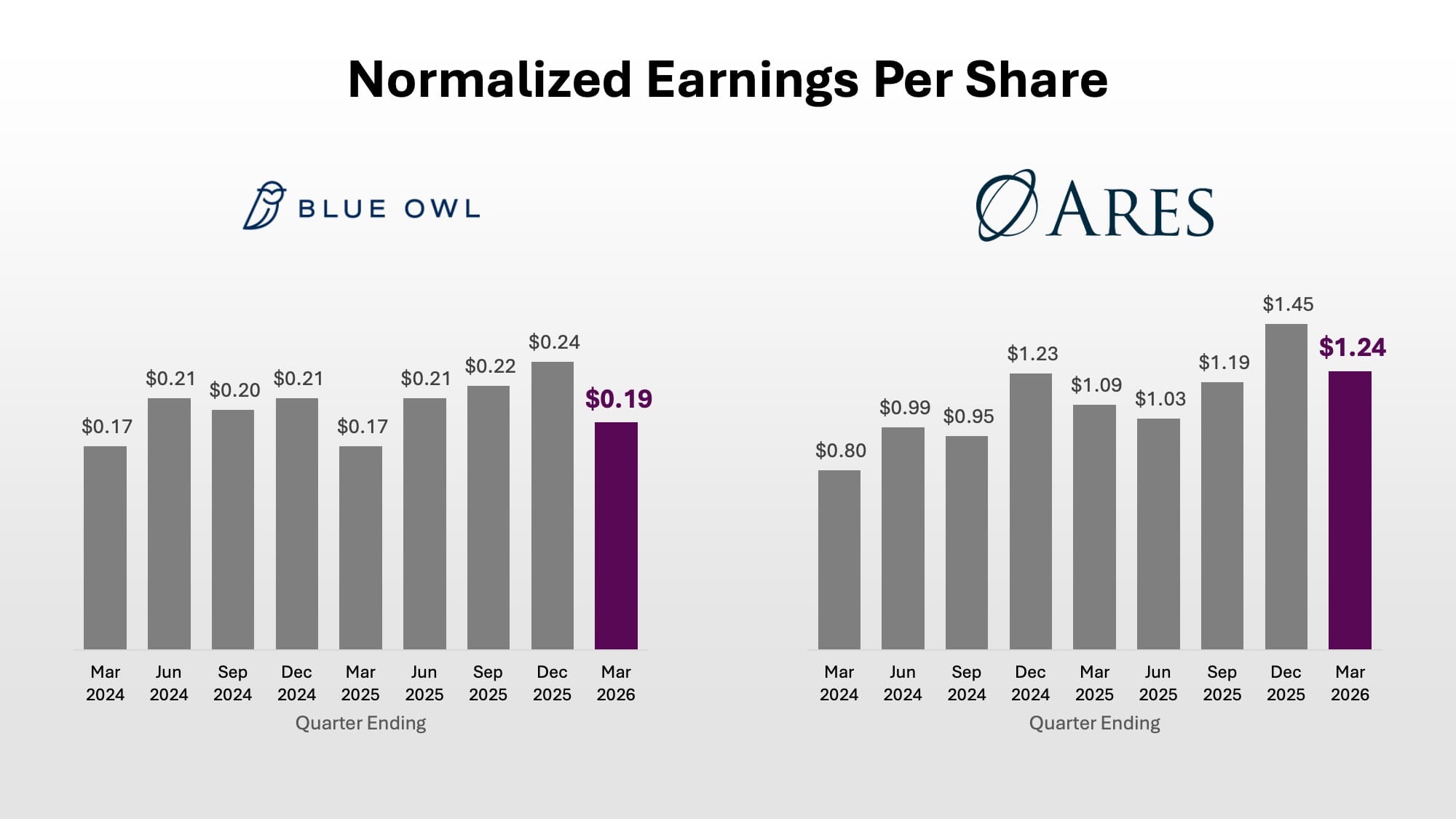

Takeaway #3: These Firms Are Still in Growth Mode

In most industries, if headlines were dominated by stories of 10%, 20%, or even 40% of customers fleeing a flagship product, you wouldn’t expect that business to still be growing at a double digit rate. Yet that is what Blue Owl and Ares are doing, posting year-over-year normalized earnings per share growth of 11% and 14% respectively.

The numbers above have some lumpiness, partly due to seasonality, partly due to inconsistent performance-linked revenue, and partly (particularly in Blue Owl's case) significant M&A activity.

But the point is these are not companies in decline, as the headlines suggest. AUM also grew at double digit rates year-over-year at both firms (14% at Blue Owl and 18% at Ares). This was partly due to continued fundraising success, but also of course due to the benefits of locked-up capital, including the redemption caps in the products dominating the headlines.

Conclusion: A First Step

To be clear, it is still far too soon for Blue Owl or Ares to declare victory, and there are some big question marks surrounding the entire industry. It is still very uncertain how long the redemption queue will last in Direct Lending, and it also remains to be seen how the funds will perform in the new environment. AI disruption in software is still ramping up, and some Direct Lending funds have significant exposure, especially at Blue Owl. In a downside scenario, institutional fundraising could become much more challenging too.

Meanwhile these two companies' share prices ares till deep in the red for the year. In Blue Owl's case, the dividend yield is over 9%, a sign that investors are still very skeptical of the company's future.

That being the case, this quarter's results can be interpreted as a sign that the doomsday scenario is still a long way off for both companies.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/