BTE Newsletter #29: "We are tired of writing $100 million and $150 million checks for the stupidity of others."

Good morning everyone, and Happy Tuesday Wednesday Thursday.

On Friday I recorded episode 12 of the podcast, featuring Capoeira Partners Founder & CEO Kurankye Sekyi-Otu, also known as "Krunch". Capoeira helps emerging alternative asset managers with all aspects of their business, including fundraising, recruiting talent, and operations. So this made for a very interesting conversation, not just about the origin stories of Krunch and Capoeira, but also about the challenges faced by emerging managers looking to grow.

Another update: I’m planning to host a webinar next month on how I build portfolios that incorporate Private Markets. It will be a good opportunity to show how my investment advisory practice actually works, and how it differs from what the industry typically offers. Details to come.

In the meantime, I wanted to put together a newsletter issue dedicated to Marc Rowan quotes. Rowan is the CEO of Apollo Global Management, and has been one of the more outspoken voices across the Private Markets industry in recent years, especially the past month. He's even earned the nickname “The Professor.” After all, Warren Buffett quotes are everywhere, so why not Marc Rowan quotes?

So below I’ve pulled together some of his most notable remarks from just the past month (all except the first one are from Apollo's latest earnings call), along with brief explanations for each to add some context.

The Many Insightful and Entertaining Quotes of Marc Rowan, Just From the Past Month

"If you can’t, as a first lien credit manager, meet 5% redemptions per quarter, I’ll say it frankly: You’re an idiot. This is not that hard to do.”

This comment came while on stage at CNBC's Invest in America Forum, and it's in response to the wave of redemption requests hitting Private Credit evergreen funds (you can see my commentary on the saga here).

He has a point. Any private asset manager has to be careful around liquidity, but Private Credit managers have many tools in the liquidity toolbox. It starts with holding a reasonable sleeve of liquid assets in the portfolio. Furthermore, loans typically get refinanced or repaid every 3-4 years, providing another source of liquidity. Secondary markets can be another tool, as can inflows, although both these avenues can dry up when markets are volatile. Increasing leverage can also be a short-term solution, although this is dependent on having a strong balance sheet at the outset.

This is also where there's a contrast between the U.S. and Canada. If you look at the recent Private Credit redemption wave in the U.S., the managers are still meeting their 5% promise. Meanwhile if you look at Canada, where some funds have suspended redemptions altogether and cut cash distributions ... well now we know what Rowan thinks of them.

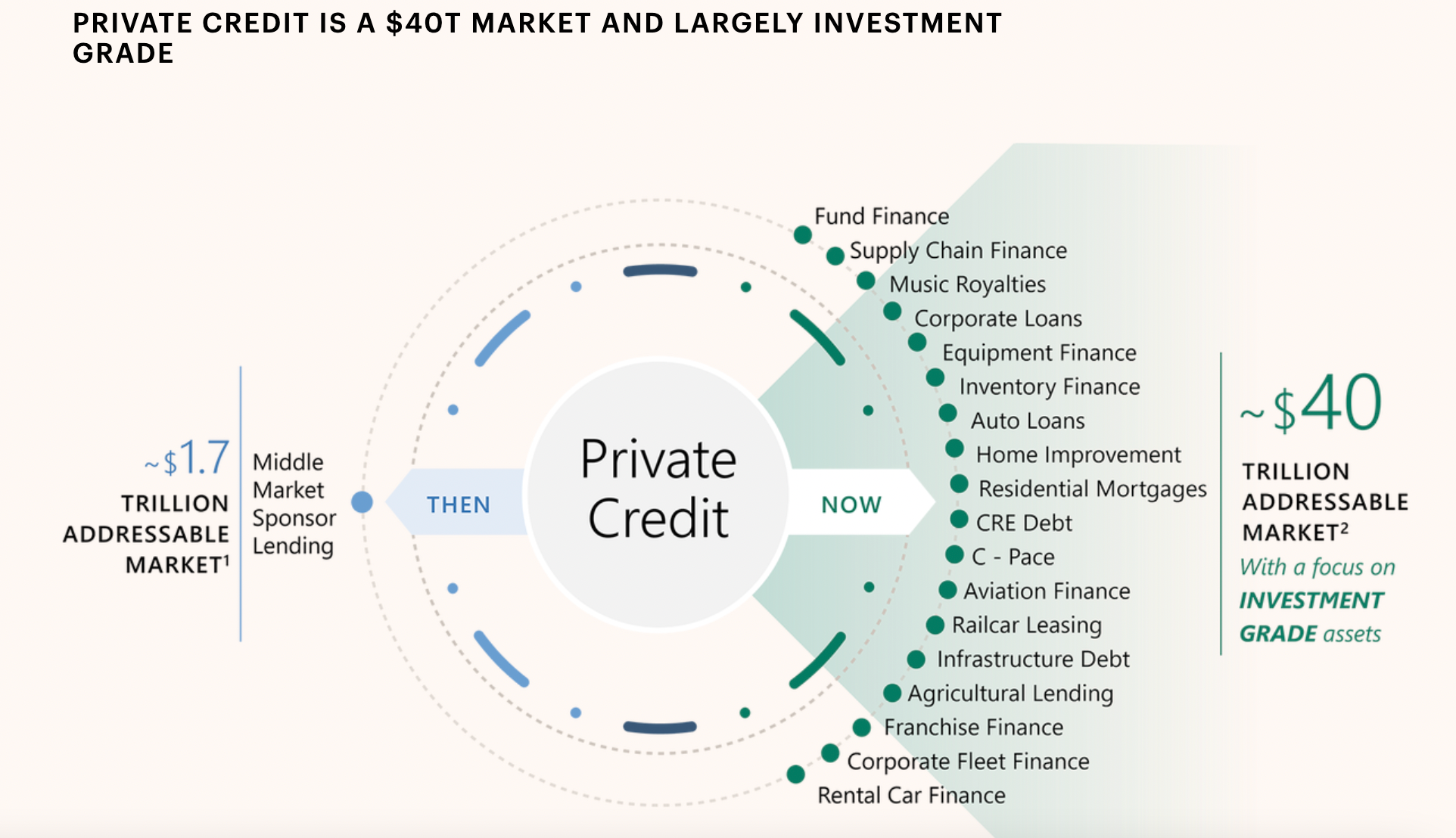

"The obsession with this very narrow corner of the market, this $2 trillion slice, levered lending, is frankly a failure of imagination."

This is a point that Apollo makes a lot, and it's often in the company's investor materials. The words Private Credit and Direct Lending are often used interchangeably (including in this newsletter). But the latter term is this "narrow corner of the market", in which floating rate sub-investment grade financing is provided to (typically private equity-backed) companies. Meanwhile the type of credit that a firm like Apollo can provide has numerous categories, and is typically investment-grade.

"The origination channel is relevant to the jockey, not the horse."

Apollo also makes the point that Private Credit is simply credit that sits outside the traditional banking system and bond markets. And one shouldn't view Private Credit as inherently risky just because of where it originated. It should instead be evaluated just like any other form of credit. Likewise, all credit (public and private) should be evaluated as one broad ecosystem, in which Private Credit is a small slice.

So in this analogy, credit is like horses. And banks or asset managers are like jockeys. In horse racing, people focus and bet on horses, and Rowan's point is that credit should be looked at similarly.

"When public markets reprice, private markets should too."

This was part of a pretty significant announcement, that Apollo will bring daily pricing to Private Credit later this year. The company has argued that this type of thing is inevitable, and has happened in other asset classes in the past.

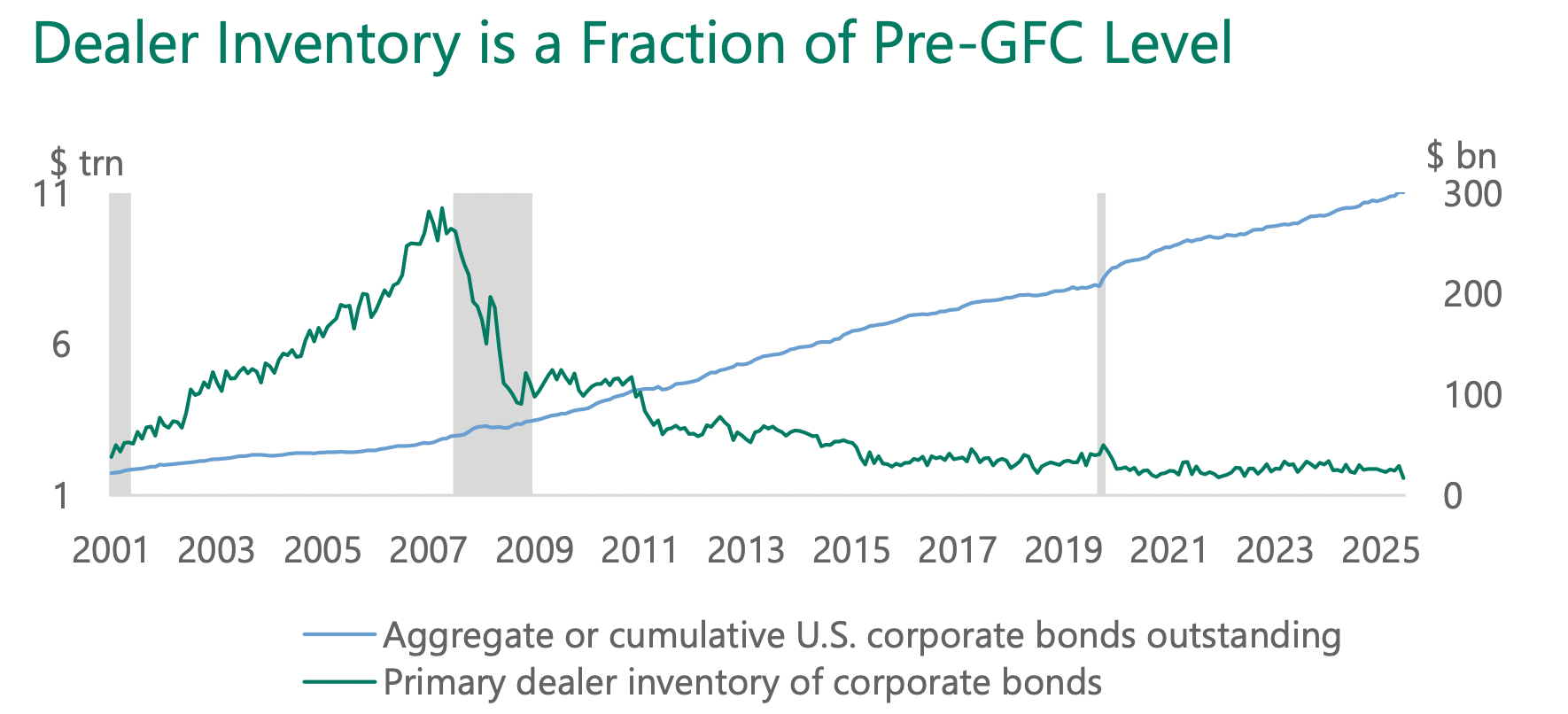

"In our fixed income markets, no one stepped forward to provide liquidity."

Related to the previous point, Rowan argues that liquidity in fixed income is a mirage, and disappears very quickly during periods of stress. The quote is a reference to these very stress periods, such as the onset of COVID.

The reason is quite simple: banks are much less involved in fixed income trading, largely due to restrictions placed on them after the Great Financial Crisis. So as Private Credit becomes more liquid, and Public Credit becomes less liquid, there is a convergence between the two strategies. This is also related to Rowan's jockey/horse analogy.

"I believe the days of buying something at 70 and writing it up to par is nearing an end."

This refers to a practice in secondaries-focused funds, in which a manager will buy a private equity asset at a discount to net asset value, then immediately mark it up to par. It results in a significant short-term gain for investors, but then longer-term performance may suffer. In evergreen funds it can be especially detrimental, as new investors may have to buy in at significantly higher valuations than what the underlying assets recently traded at.

"We watch what's being purchased around our industry, and we kind of shrug our shoulders and just say, like, did we miss it? And I don't think we've missed anything yet."

This refers to mergers & acquisitions made by alternative asset managers, an area where Apollo has not been especially active. Mergers make a lot of sense in theory, as the benefits of scale are becoming increasingly apparent in this industry, but culturally they are difficult to pull off for both traditional and alternative asset managers.

Now with stock prices having traded down more recently, it's understandable Apollo would be more interested in repurchasing its own shares. And when EQT buys a big secondaries player, or KKR buys a sports investor, Apollo does not seem to be getting envious.

"Measuring our industry on AUM is imprecise at best and foolhardy at worst."

Apollo claims that its bottleneck is finding enough good investments to originate; it's not about how much money they can raise, it's about how much they can put to work effectively. So when the press (or investors, or even me) measure success based on fundraising numbers, Rowan is arguing that they (we) are missing the point, and if Apollo can continue investing money effectively then good fundraising will naturally follow.

"We are tired of writing $100 million and $150 million checks for the stupidity of others."

This refers to failures in the insurance industry, where Apollo is a major player through its subsidiary Athene. When an insurer goes under, through state guaranty funds and other protection schemes, Apollo ends up having to foot a significant portion of the bill.

Partly for this reason, Apollo is quite vocal about some of the pitfalls that can befell an insurer. Taking too much credit risk on the asset side, writing bad policies, and getting asset/liability matching wrong are common mistakes. One issue that Apollo has been more vocal about recently has been the Cayman Islands, a jurisdiction that comes with more lax oversight than Bermuda, where Athene and others have traditionally focused.

"Software is the ground zero for issues around AI. That does not mean every software company is at risk. In fact, some may be enhanced. But our view is in the credit market, we are not paid to figure that out"

Of course Rowan would have plenty to say about the disruptive aspects of AI. It's something that I've written about too.

The general consensus is that some companies will survive AI disruption, particularly those with high switching costs, proprietary data, and highly-regulated end markets. For those companies able to adapt quickly, embrace AI, embed new features into their offerings, and even change their pricing model, AI could be a fantastic opportunity.

But of course in credit, the best one can do is get their money back. So it doesn't pay to have a credit portfolio with a few success stories and a few failures. Those bets work better in Private Equity, according to Mr. Rowan, where the home runs can make up for the strikeouts.

"If you are an Ivy League graduate who's in the liberal arts and certain things, you're 10 years out of school, you're making $60,000. If you can level a concrete floor, you're making $250,000."

Rowan's point here is that not just software companies are at risk; professional services firms are too. So in Apollo's Private Credit business, there's more of a skew towards material goods and hard assets, which provide more downside protection in today's world.

Of course this statement hit home for me, because I cannot level a concrete floor, and can hardly do any type of manual labour. But luckily I was never smart enough to go to an Ivy League school either.

"If you just discovered 6 or 8 weeks ago that AI could impact enterprise software, what were you doing for the past 2 years?"

This quote is quite self-explanatory.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/