BTE Newsletter #31: Not a Good Look For the Canada Pension Plan

Good morning everyone, and Happy Tuesday once again.

First a reminder, I'll be hosting a webinar Thursday June 18th at 11am on building investment portfolios that incorporate Private Markets. And in response to a question I've been getting, all attendees will be anonymous to each other, as is customary for webinars.

Second, podcast episode #12 with Kurankye Sekyi-Otu ("Krunch") of Capoeira Partners is now available on Spotify and Apple Podcasts. He and I talked about his background, what it takes to succeed as an emerging asset manager, and how Capoeira helps these firms. To listen, you can use the links below:

|

|

And finally, the Canada Pension Plan just released its latest annual report, and there's some controversy to say the least. More on that below.

Ben

Upcoming Webinar: June 18th at 11am

While I enjoy writing about the latest Private Markets news here at Beyond The Exchange, I've provided relatively little information about actually building investment portfolios that incorporate Private Markets. That's what this webinar is meant to solve. I'll cover topics such as:

- What kinds of people are most suited for Private Markets?

- How do different asset classes such as Private Equity, Credit, Infrastructure and Real Estate compare?

- What kind of criteria are most useful when evaluating Private Markets funds?

- Is there a minimum dollar amount to qualify for these investments?

I hope to see you there.

What on Earth Is Going On at CPP?

When I pitch my services as an Investment Advisor, I often use CPP as an example. After all, they use a healthy mix of public and private assets, thus building a more complete (and better-diversified) portfolio than one consisting of just stocks and bonds. I consider this to be a strong case.

But when looking at CPP's results, and its recent actions, it's clear the organization has a lot of explaining to do. It starts with recent underperformance versus its benchmark. CPP also changed its benchmark to one with worse numbers, thus making outperformance easier to attain. Then to make matters worse, CPP backdated the new benchmark to determine executive bonuses. Disclosures have also been altered.

Underperformance versus the Benchmark

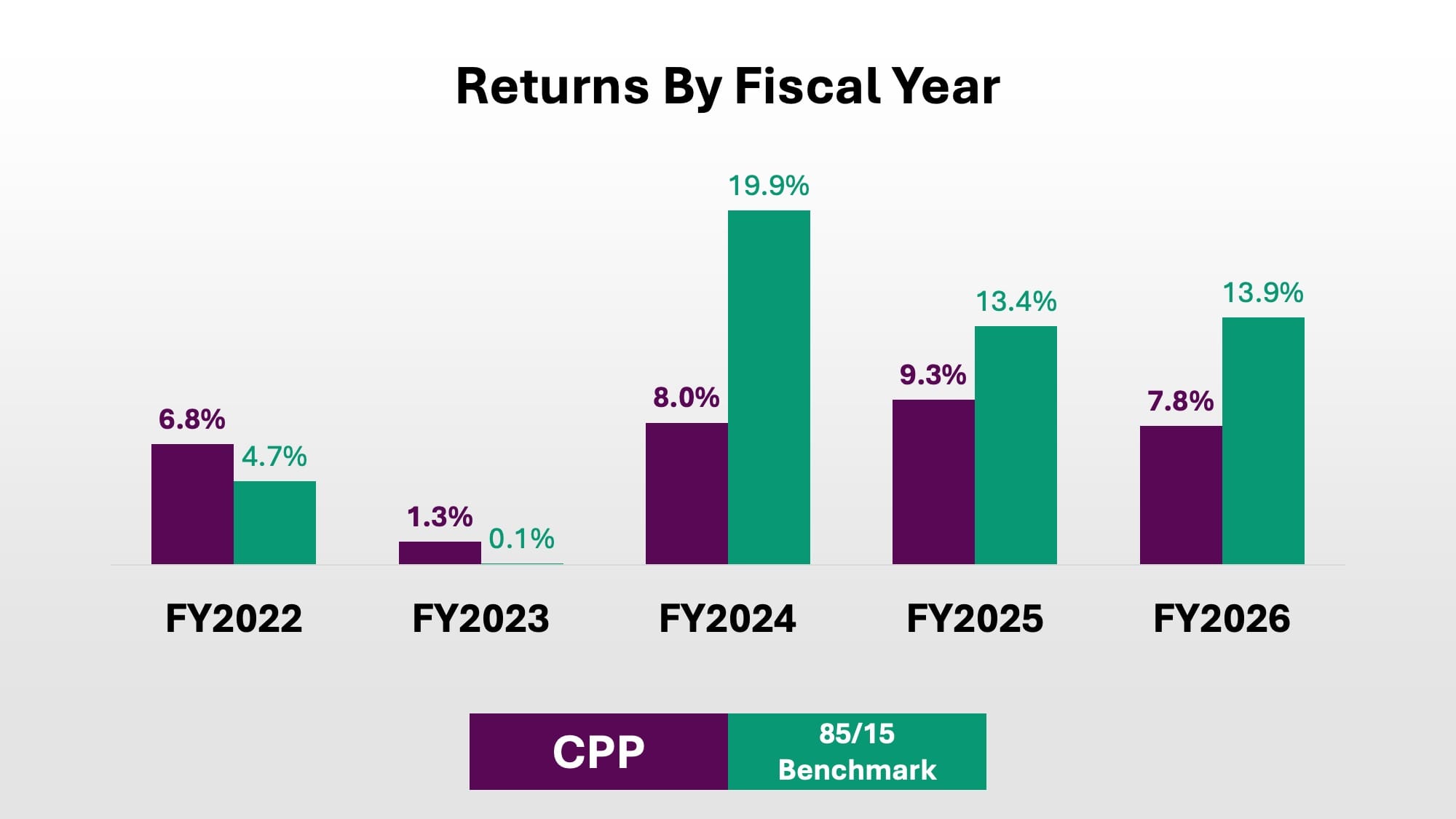

Starting in 2019, CPP set its benchmark "reference portfolios" to consist of 85% global equities and 15% Canadian Government Bonds. These numbers were, and still are, meant to reflect the targeted level of market risk in the CPP portfolio.

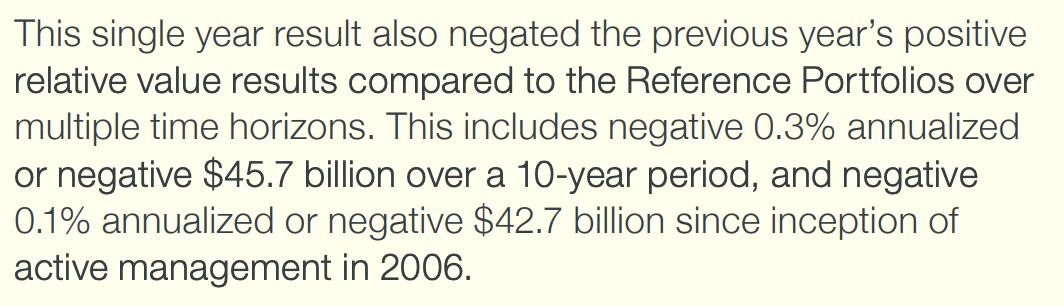

However over the past 5 years, the actual CPP portfolio has only returned 6.6% per year, while the 85/15 benchmark has returned over 10%. This includes steep underperformance for each of the past 3 years:

In many ways, underperformance over the past three years is understandable, even expected. Public equities have been on an absolute tear over that span, driven in large part (but not exclusively) by technology companies and the AI trade. Meanwhile Private Equity has not kept pace, as highly-levered companies with floating rate debt have contended with rising interest rates. Other alternative strategies have also lagged, again largely due to rising rates. For any portfolio with a large allocation to Private Markets, especially one as large and diversified as CPP's, these are massive hurdles to overcome.

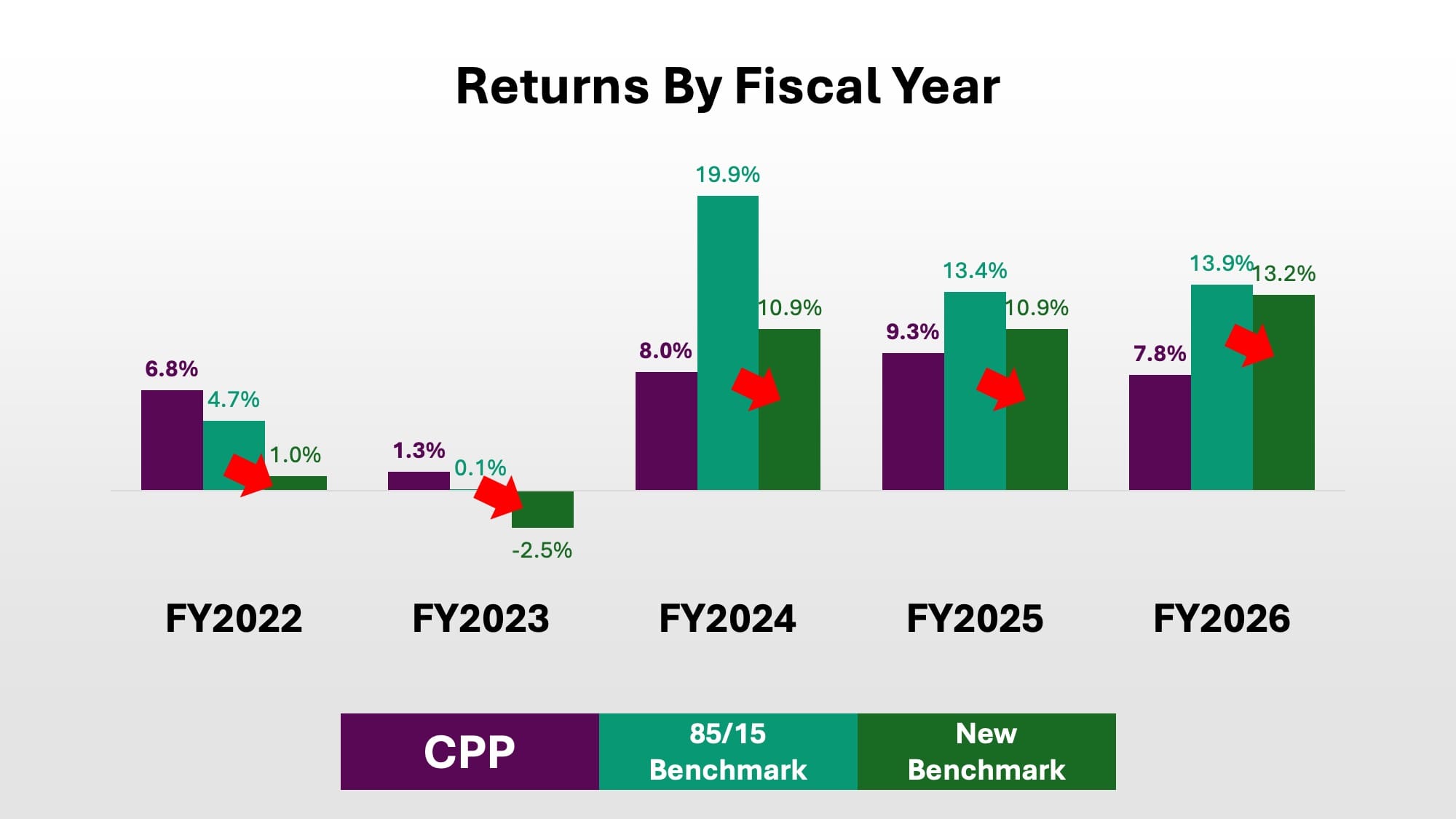

Changing the Benchmark

Last year, CPP adopted new "Benchmark Portfolios" that replaced the 85/15 Reference Portfolios as the "benchmark against which relative performance is measured." Then for good measure, the 85/15 Reference Portfolios were renamed "Market Risk Targets".

One could argue the new benchmark is more appropriate. It is much more broadly diversified, and the underlying exposures more closely align with the private investments at CPP. Furthermore, CPP has argued that adopting the new benchmark was a gradual process over many years, with the final decision being made a year earlier. In other words, this wasn't a knee-jerk decision in response to weak performance.

But the fact remains that the new benchmark is easier to beat than the old one, at least in recent years. And the change was still announced in 2024, a year of sharp underperformance relative to the outgoing benchmark.

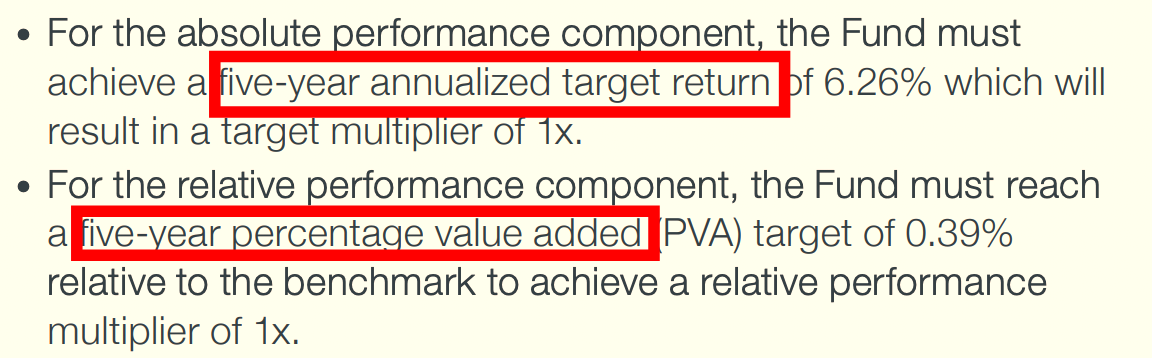

It Pays To Work at CPP

For the purpose of assessing performance, CPP uses its 5-year trailing investment returns. This is for both the absolute and relative performance component:

But here's the problem: for the relative ("value added") component, CPP applied the new benchmark retroactively, which for the record goes against CFA best practices. The action also drew fierce backlash from some prominent industry figures.

Knut Norheim Kjær, the first manager of the Government Pension Fund of Norway, called it "concerning" in a Toronto Star article because "they are able to by themselves change the measurement standard and to pay themselves accordingly...that is not the normal integrity in such a business." In that same article, Claude Lamoureux (who originally established the "Maple 8" model at Ontario Teachers' Pension Plan) said he was "disappointed", adding "To me, that's not something they should have done."

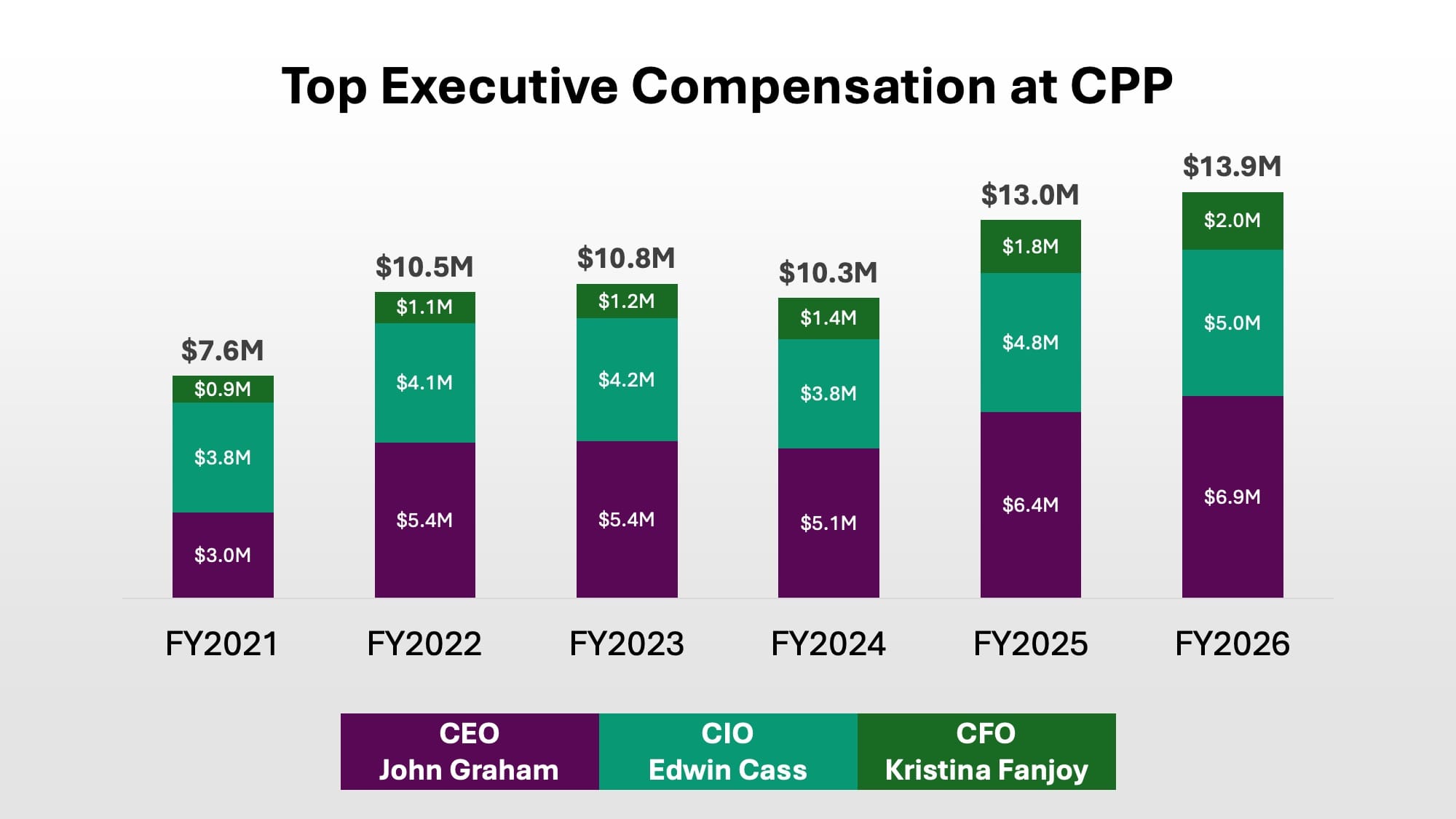

On top of that, in 2025 CPP added a new metric to its performance scorecard, called the "Strategic Objectives Performance Multiplier." In that first year, CPP gave itself a perfect score of 2.0, followed by a 1.8 score for fiscal 2026.

Putting all that together, and compensation for the CEO/CIO/CFO executives has continued to climb during a period of questionable investment performance.

Changing the Messaging

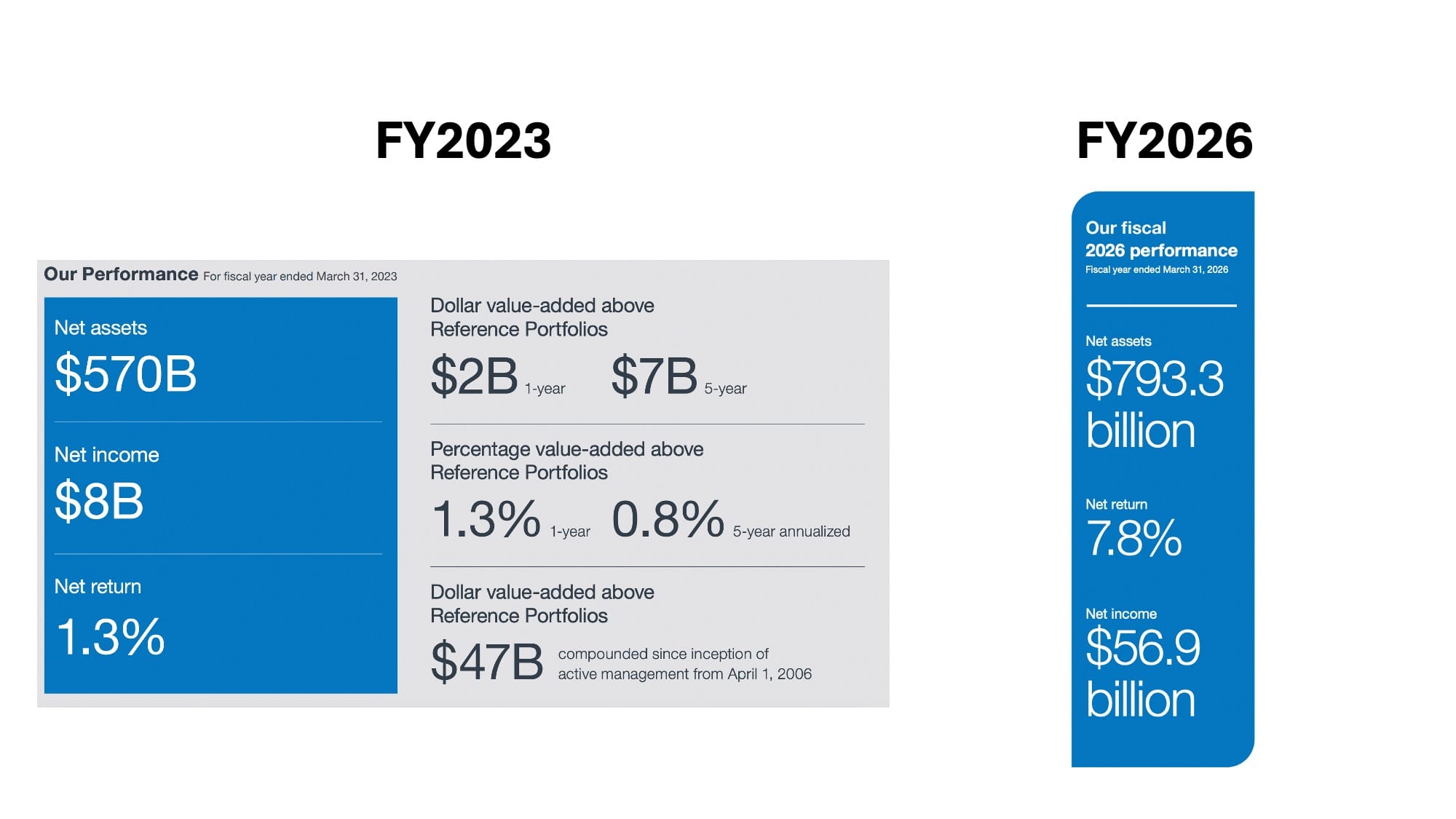

To top it all off, CPP has had a relative lack of transparency or introspection when it comes to their underperformance. Even just looking at the first few pages of their annual reports reveals a stark difference between their last year of outperformance (2023), when there was a lot more detail, and the most recent year:

When digging a little deeper, CPP reported in its FY2024 annual report that since the current strategy's inception (2006), CPP has delivered -0.1% annualized value-add versus the reference portfolios. Then in 2025 and 2026, this level of disclosure was removed altogether.

To some extent, it's unrealistic to expect anyone to shine a light on their own shortcomings; that's not the way the world typically works. But for an organization that is supposed to serve the public interest, we should expect better, especially since more introspection may lead to improved outcomes down the line. Also in retrospect, CPP should not have been so vocal about its outperformance during the good years, if it was not willing to have that same transparency during down years (this is undoubtedly a lesson I should implement for my own practice).

A Higher Standard

This is not meant to be just an angry rant about CPP, nor an exhaustive look at their performance over the past five years. Anyone interested in much more in-depth and critical work on CPP can find Andrew Coyne at the Globe and Mail, "Millenial Moron" on Youtube, or Mathew Kaminski on Substack.

As for me, I still see CPP as an institution with a lot of admirable qualities. It has a sophisticated investment organization with some of the brightest people in the industry, and these people are relatively free from political interference. But as I look to adopt best-of-breed institutional investing in my practice, it's worth calling out instances where even the largest institutions can do a lot better.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/