BTE Newsletter #32: Should Private Credit Reprice Daily?

Good morning everyone, and Happy Tuesday Wednesday.

We're now just over a week away from the webinar I'm hosting on Private Markets. And in the meantime there are a flurry of live events, including two today, one hosted by Capoeira Partners (whose CEO appeared on the most recent podcast episode) and one hosted by Designed Wealth Management. I'll be sure to make an appearance at both, so if any of you are going to either, I hope to see you there.

Meanwhile we've started seeing the latest redemption rates for Private Credit funds, and so far the trend is not exactly ideal. Funds managed by Monroe Partners, Cliffwater and Blackstone have seen these rates increase from last quarter, and the market also got spooked by news from Partners Group's Private Equity fund. But this is still a developing story, so I won't dedicate this newsletter issue to it. Expect some commentary in a week or two.

As for this issue, last month I wrote a summary on some memorable quotes by Apollo CEO Marc Rowan (you can see it here). And I wanted to follow up on one quote in particular, in which he said "When Public Markets reprice, Private Markets should too."

This comment was related to Apollo's plan to price its Private Credit assets daily, which should be completely implemented by September 30. So does this idea make sense? I think it's worth taking a shot at answering that question.

Ben

Upcoming Webinar: June 18th at 11am

As I get set to host my first webinar on Private Markets, I've already been very pleased with the response. The fact remains that this is a new area for many people, and even though I comment on Private Markets every week, there is still broad confusion about how to invest in these strategies effectively. So I'll be sure to answer questions such as:

- How do different asset classes such as Private Equity, Credit, Infrastructure and Real Estate compare?

- What kind of criteria are most useful when evaluating Private Markets funds?

- Is there a minimum dollar amount to qualify for these investments?

To be clear, this is free and welcome to everyone. Guests are also anonymous to each other. I hope to see you there.

Should Private Credit Reprice Daily?

Ever since taking over as CEO of Apollo, Marc Rowan has been very vocal about an inevitable convergence between public and private assets, particularly in credit strategies. He's even argued that before long, you won't even be able to tell the difference between public and private credit.

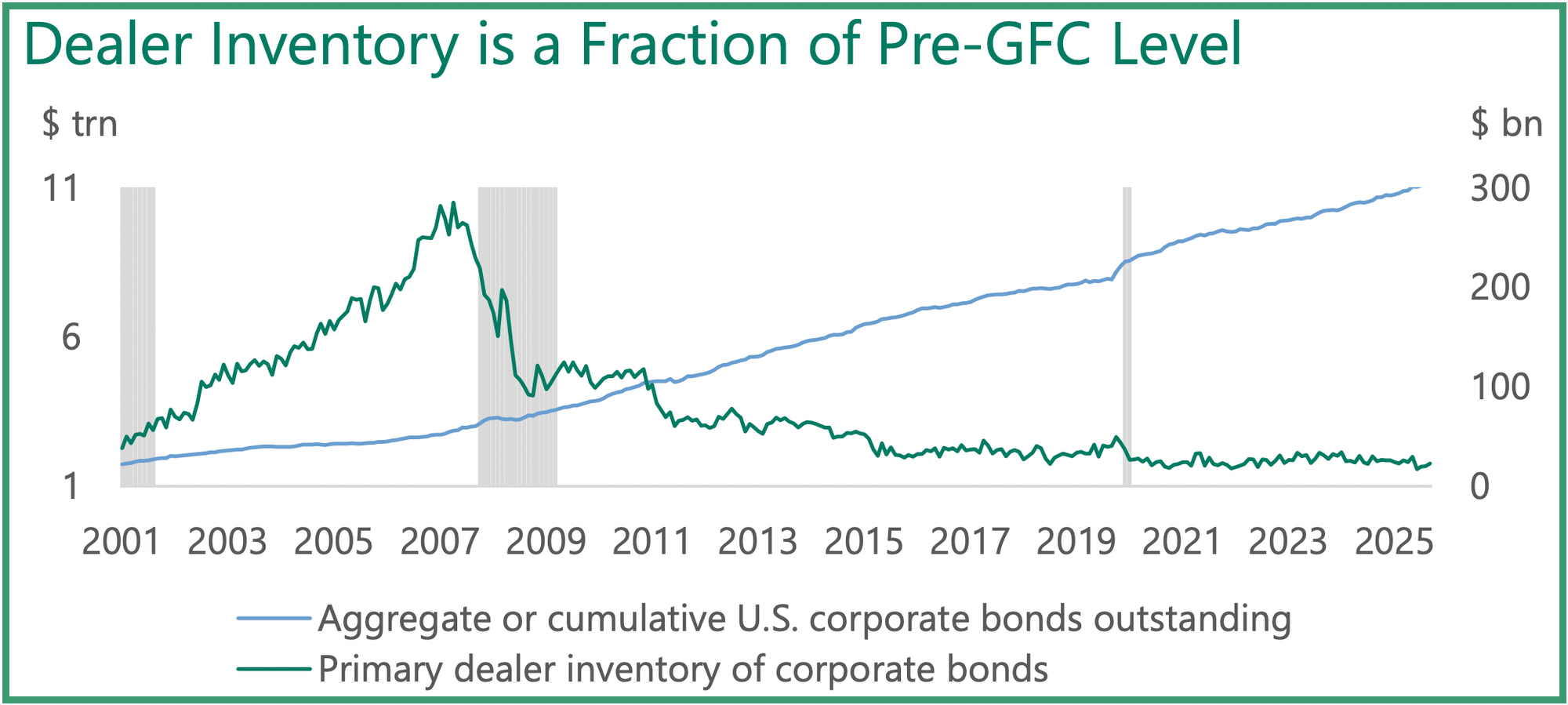

Part of his argument is that liquidity has dried up in public fixed income. After the Global Financial Crisis of 2008-2009, and the Dodd-Frank Act that followed, banks do not devote nearly the same level of capital to bond trading that they once did. This makes little difference most of the time, but shows up during times of stress when trading seizes up and prices move very suddenly.

Meanwhile Private Credit has been moving in the opposite direction. Apollo has led the charge on trading these assets, and others have followed suit. So it was only natural that in early May, Apollo announced that it would bring daily price updates to all investment grade Private Credit by the end of June. Then by the end of September, all of Apollo's credit assets should be priced daily.

The Story of Broadly Syndicated Loans

There are precedents for this trend, and one that Apollo cites is the Broadly Syndicated Loan (BSL) market. These loans are originated by banks, but the end investors are quite disperse (hence the phrase "Broadly Syndicated"). Some of the loans are still held by banks, but they are also held by mutual funds and ETFs. Most go into Collateralized Loan Obligations (CLOs), which divide the loans into new assets with different risk levels. These new assets also go into mutual funds and ETFs, including some offered by the Canadian banks. The result is a disperse market with frequent trading, constant price discovery, and retail investor access.

It wasn't always this way. These same loans used to be very illiquid assets and did not trade regularly; they instead sat on bank balance sheets. But then legendary investment banker Jimmy Lee from JPMorgan (pictured below) helped usher in a new era, initially by simply calling other banks to place trades, but then by pushing for more standardization in these assets. Eventually what followed was essentially a new asset class, one that could make up part of an individual investor's fixed income allocation. Today, trading these loans is a very profitable activity for the major banks.

Repeating History

Fast forward to today, and Apollo is leading a similar charge on Private Credit, setting up a trading desk for the asset class. JPMorgan has followed suit, and while progress has been slow thus far, other banks such as Goldman Sachs and Morgan Stanley are ramping up efforts too. On a related matter, last year Apollo launched the first ever ETFs featuring Private Credit, in partnership with State Street.

What Does the Future Hold?

Total convergence is still a long way off, especially for individual investors. As an Investment Advisor, I can confirm there is a big difference between buying a Private Credit fund and investing in public bonds. But in the institutional world, where the Total Portfolio Approach is gaining traction, there is a growing realization that credit is credit, whether originated by a bank or originated by Apollo.

In any case, this is clearly a natural progression. As any asset class grows in size and becomes more mainstream, buyers and sellers will both want to trade at a market clearing price. In the case of Private Credit, more frequent price discovery and trading could also help bring more investors into the asset class. And with Private Credit investors demanding greater liquidity, conceivably this trend could be a big help down the line.

There is still debate over whether this means Private Credit will lose its edge over public equivalents. KKR co-CEO Scott Nuttall speculated at a recent conference that this may happen. Apollo counters that if they originate an asset, rather than wait for the phone to ring from a counterparty, then that's what will drive investment outperformance. Either way, one should expect the line between private and public credit to keep getting blurrier. And other asset classes may very well follow suit.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/