BTE Newsletter #35: Private Credit's Math Problem

Good morning everyone, and Happy Tuesday once again.

I hope you all had a great Canada Day (or July 4th) week, despite Canada's World Cup loss and despite the absence of a Beyond The Exchange newsletter issue. I took the week off for the holiday, but I assure you there will be no more such crimes until Christmas; you can expect a steady stream of newsletter issues until then. But no promises about our national soccer team.

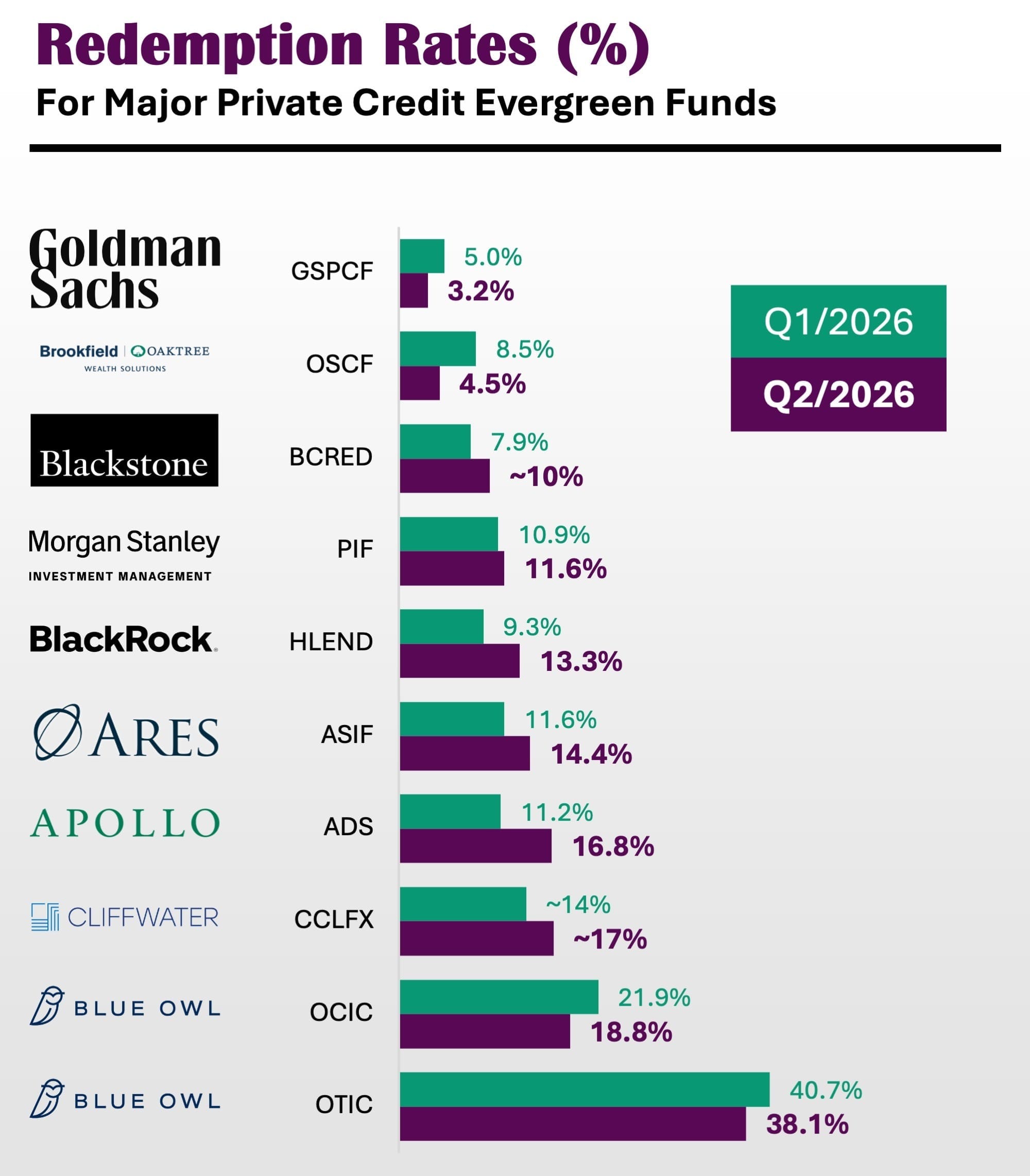

In the meantime, Private Credit managers released the latest redemption figures for their evergreen funds, with the big announcement coming from Blue Owl on Thursday. I first wrote about skyrocketing redemption requests in April, and now with the latest numbers, it's time to update those thoughts.

In other news, episode 13 of the podcast has now been edited, and I hope to have it released soon. Episode 14 has also been recorded, and episode 15 has been scheduled. For those of you looking to listen to past episodes, you can do so here:

|

|

Ben

The Latest on Private Credit Redemptions

One of the defining stories in Private Markets in 2026 has been the surge in redemption requests for retail Private Credit funds.

As a refresher, this story started last year with concerns about two problem loans (that weren't even in Private Credit). Then came a PR misstep from Blue Owl. Then concerns about the "SaaSpocalypse" and what that would mean for Private Credit. Then another PR misstep from Blue Owl. Consequently redemption requests from Private Credit funds spiked, as investors raced to the exits.

All the while, investment performance was still solid, and the funds all honoured an aggregate redemption rate of at least 5%, consistent with their initial promises. But investors were not getting back all the money they wanted, which made for some negative headlines.

When the initial wave of redemption requests came, I gave 10 thoughts on the matter. Now the second round of numbers are in, with somewhat mixed results:

The Good News: This Could Have Been Much Worse

When the redemption requests increased earlier this year, all sorts of bad scenarios became possible. Would these requests keep increasing, as investors raced each other to the exits? Would this sentiment extend beyond Private Credit to other asset classes? Would it extend beyond retail investors to institutions? Would it spread beyond North America to Europe and Asia?

So far, the answers to all these questions appear to be no. Some funds saw increased redemption requests come in, and others did not. Goldman Sachs and Brookfield/Oaktree in particular deserve praise here, since the two firms saw their redemption requests decline from already-low levels.

Blue Owl's numbers are also quite encouraging, even though the company remains at the bottom of the chart above. While redemption requests remain high, a large majority of them (presumably) were unfulfilled requests spilling over from the previous quarter. So the actual number of brand new redemption requests was likely far smaller than Q1's level. With Blue Owl being at the epicentre of this saga, the whole industry should welcome these numbers.

The Bad News: This Will Be a Slog

While the numbers above are encouraging, the industry is also facing a math problem, which again is perfectly illustrated by Blue Owl.

If one looks at Blue Owl Technology Income Corp (OTIC), close to 40% of investors (by dollar amount) want their money back. Meanwhile the fund will only honour a 5% redemption rate, or 13% of the requests actually coming in. That leaves 87% of requests unfulfilled, and in all likelihood, the vast majority of those investors will line back up to redeem in Q3. So even if OTIC doesn't get any brand new redemption requests, the backlog will likely take many quarters to clear up.

And that's a big assumption. This is all happening while OTIC's performance remains solid. What happens if defaults start rising, as the SaaS doomsayers are predicting? What if there's a recession, or a bear market, or a major geopolitical event? What if one of Blue Owl's peers falters, triggering a new wave of investors rushing for the exits across the industry?

Even without those events, there is a self-reinforcing element to excess withdrawal requests. Even if an investor only wants a portion of their investment back, they are incentivized to request much more, since they know only a fraction of that request will be fulfilled. This type of dynamic will likely keep redemption requests high, and there's little that a firm like Blue Owl can do about it.

What Does the Future Hold?

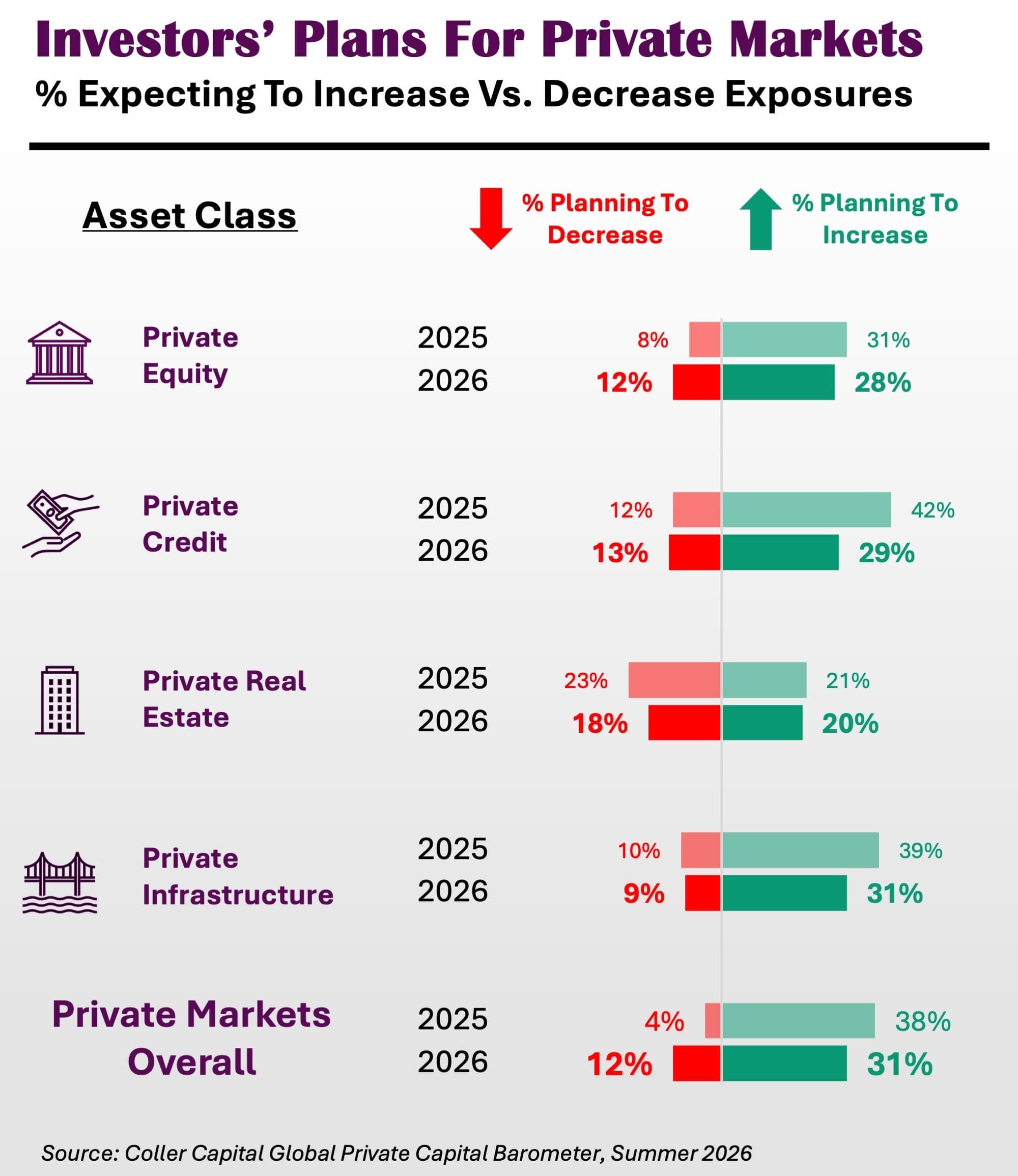

While the backlog will not resolve any time soon, there are a number of silver linings for the industry. For starters, this issue is limited to retail investors, and limited to Private Credit, and limited to North America; there is practically no sign that this problem has spread.

Instead, in Europe (where SaaS loans are less prevalent) this is still a non-event. The issue has not spread to other asset classes such as Private Equity or Private Infrastructure. And institutions have not slowed down allocating to Private Markets, including in Private Credit, where anecdotally speaking some large investors see an opportunity to allocate at a time when capital is more scarce.

So now it appears this will be a long overhang in one specific part of the Private Markets industry, nothing more and nothing less (assuming the market environment doesn't get significantly worse). At some point the managers may choose to deal with the redemptions more aggressively, perhaps by selling assets to raise cash. In the meantime, it will be interesting to hear commentary from the managers during their quarterly earnings calls, starting with Blackstone in just over two weeks.

In the long term, the industry may be better off. If so many investors are racing for the exits right now, simply due to fear of having their money locked up, then arguably these investors should not have gone into Private Markets in the first place. Who knows how many of these investors received bad advice, or didn't understand what they were doing, or were complacent, or a combination of the three. Private Markets has a lot to offer, but only for investors who understand what they are doing and have a long-term time horizon ... if those are the investors that remain in these funds, then that should be better for everyone, including the asset managers.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/