BTE Newsletter #24: 10 Thoughts On the Wave of Private Credit Redemptions

Good morning everyone, and Happy Tuesday once again.

First things first, episode 10 of the podcast with Julian Klymochko is now live. His firm, Accelerate Financial Technologies, has a set of ETFs that focus on alternative strategies. One of them invests in Private Credit vehicles (so-called public Business Development Companies), so the topic is quite timely given all that's happening in the asset class. You can listen to the episode (or any of the other episodes) here:

|

|

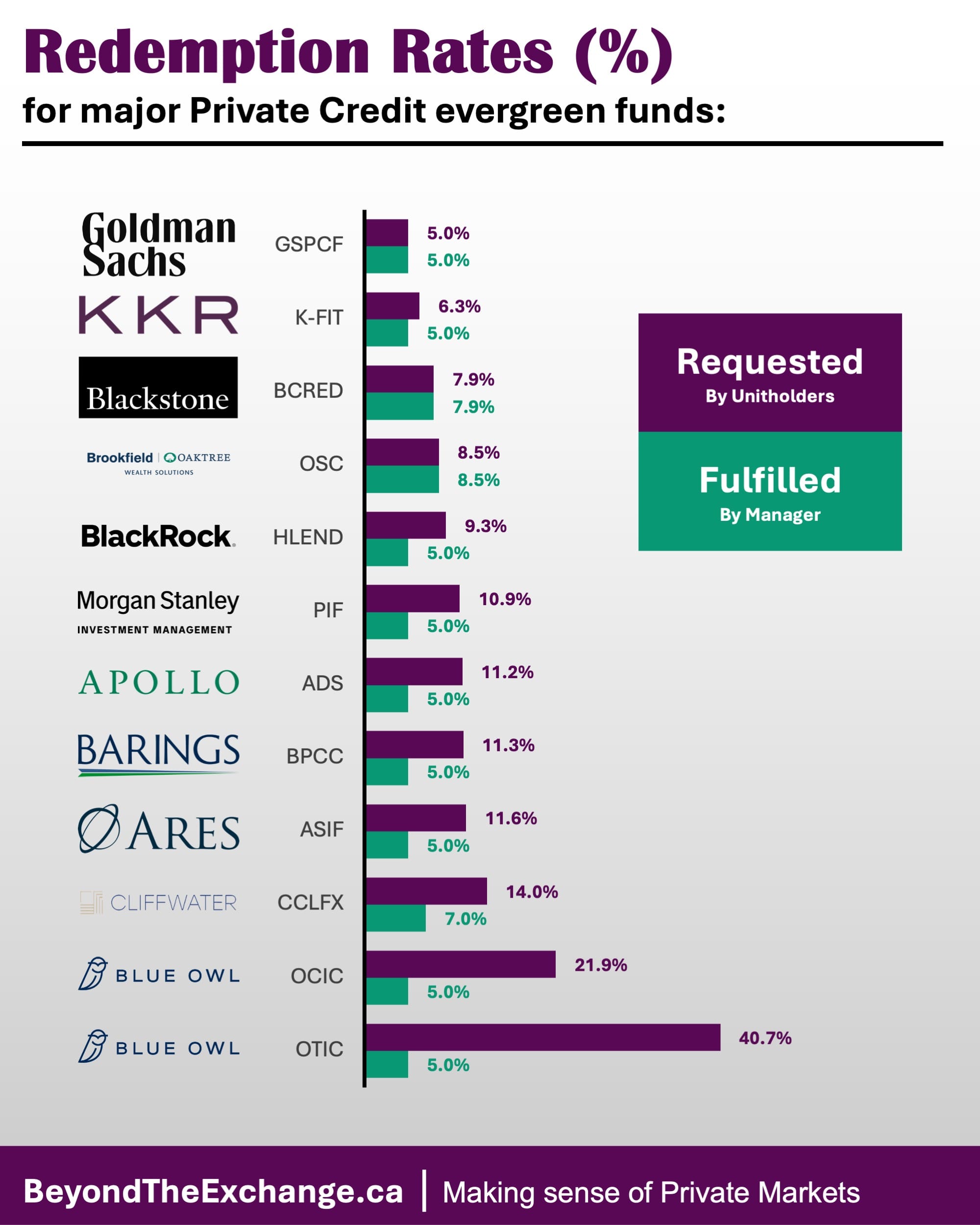

Speaking of Private Credit, for those of you unaware, there has been a wave of redemption requests in the space. And only a handful of firms have met these requests in full. The final firms (including Blue Owl) reported last week, and the numbers aren't particularly flattering:

So with that said, there's a lot to say about what's going on. Below I've organized it into 10 thoughts.

Ben

10 Thoughts on the Private Credit Redemption Wave

1. This is not driven by investment performance.

Taking a step back, there were a few events that led up to this surge in redemptions. Last summer, after a couple of high-profile bankruptcies, pundits repeatedly tied these failures to Private Credit excesses, even though these companies were primarily financed by banks. Then there was Jamie Dimon's famous "cockroaches" quote. Then Blue Owl made its first PR misstep, with a proposal to merge two of its private credit funds. Then a narrative of AI killing software companies took hold in February. Then Blue Owl made its second PR misstep, when it sold a portfolio of private credit assets and moved to wind down one of its funds.

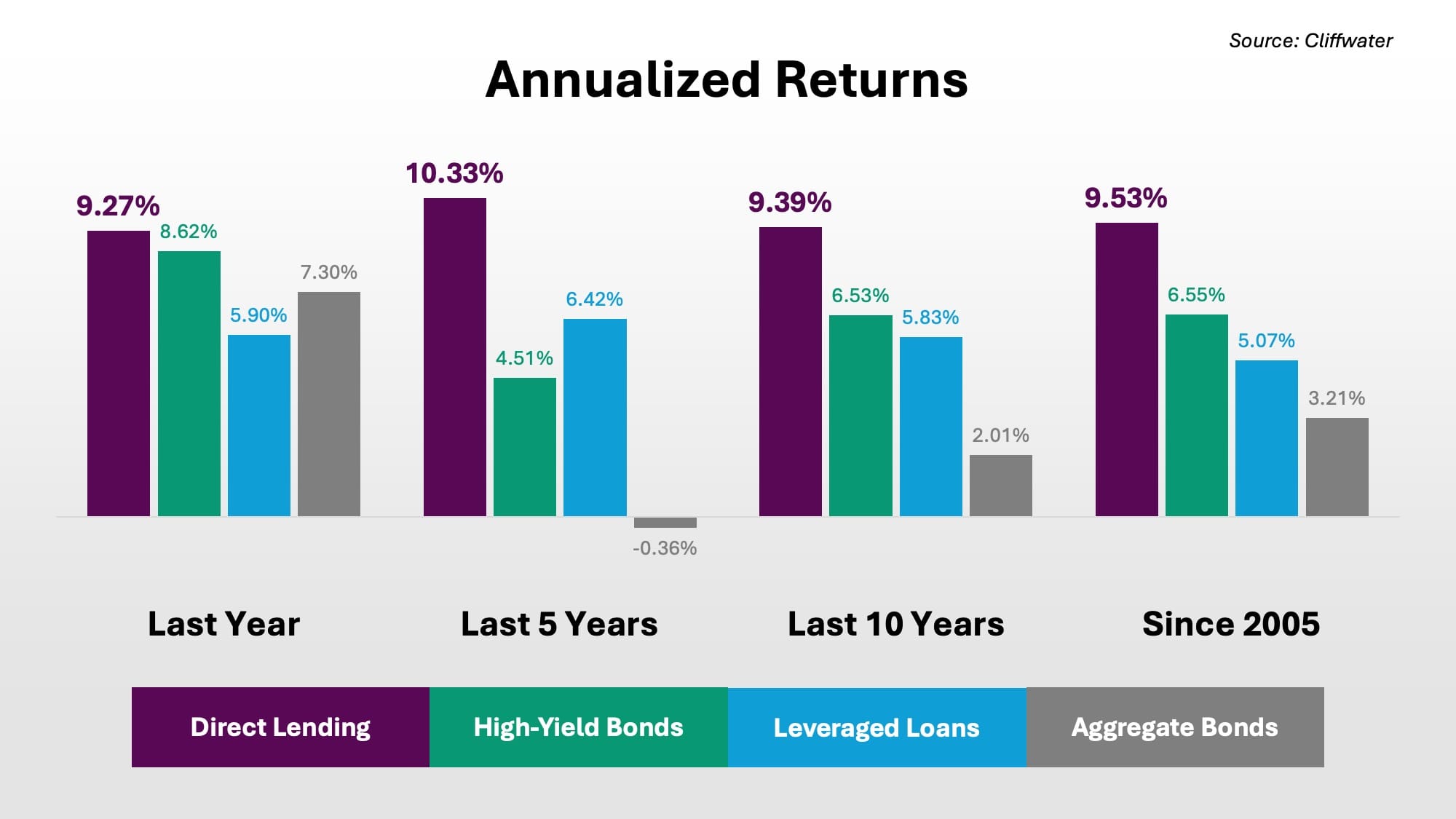

But all the while, investment performance in the space has remained solid. In 2025, the Cliffwater Direct Lending Index (CDLI) once again outperformed high-yield bonds, leveraged loans, and the bond index as a whole. When looking back over longer timeframes, again Direct Lending has performed much better than comparable strategies.

2. There is no sign that the loan portfolios are deteriorating (as a whole).

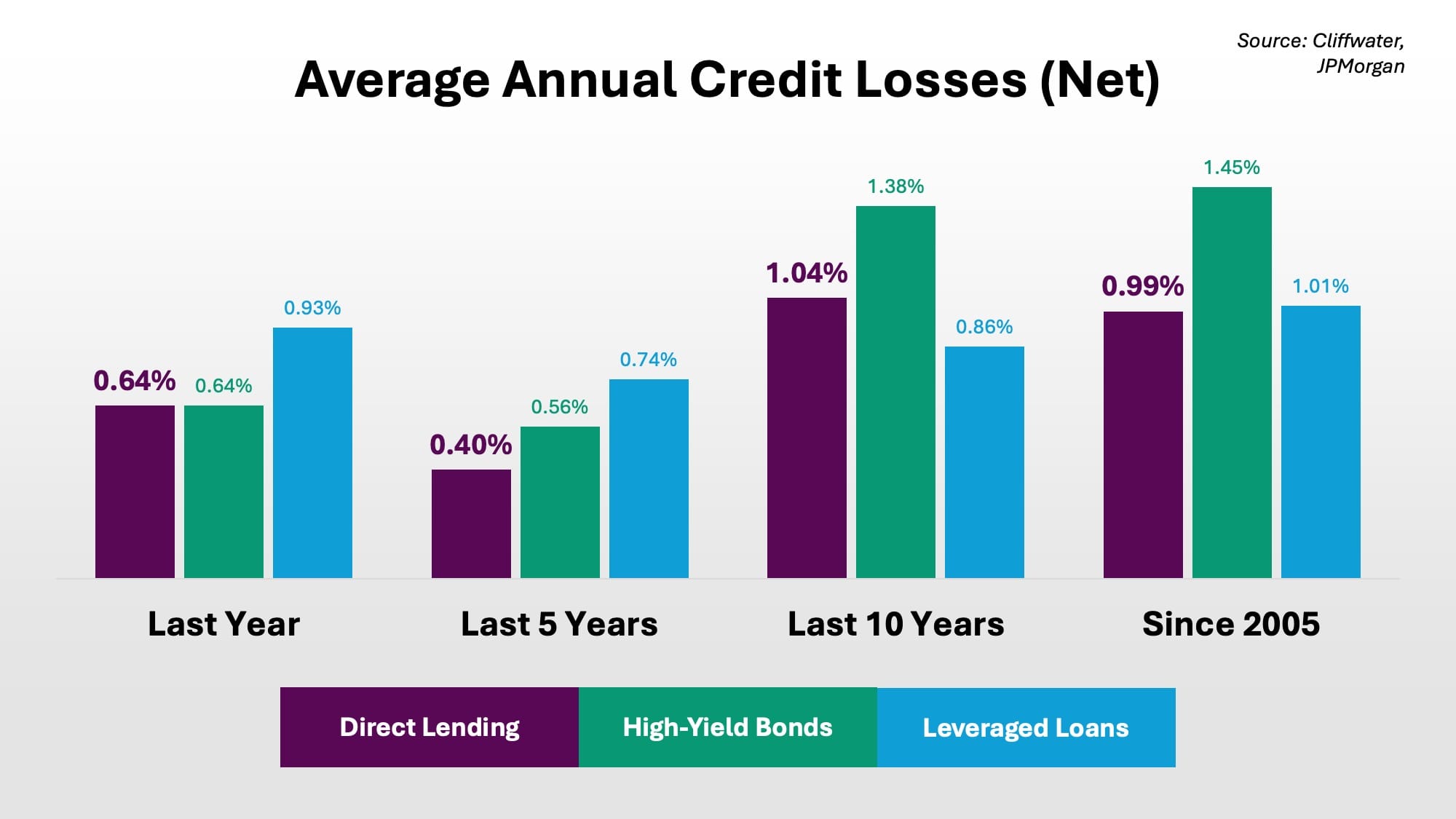

Much has been written about the wave of credit losses that are about to hit private credit. One article from early 2020 even had the provocative headline "High-Yield Was Oxy. Private Credit Is Fentanyl." But much less has been written about actual credit losses in private credit, other than stories about individual loans gone bad.

Again when using Cliffwater data, historical credit losses for Direct Lending have been lower than for comparable asset classes. Losses were also benign last year. Portfolio credit metrics (loan-to-value, % first lien, % delinquent) generally remain quite strong. Some funds are performing worse than others, and there is general consensus that losses will drift upward with the economic cycle, but so far there are very few signs of excess.

3. The AI-is-killing-software narrative is overdone.

I wrote about this idea a few weeks ago for the newsletter. In the public and private markets, investors seem to be painting software companies with a very broad brush. Yet for a number of reasons, one could argue that AI is more of an opportunity than a threat for established software providers.

For starters, incumbent software companies benefit from tremendous switching costs, as they are typically embedded into existing workflows. This is especially the case if they hold proprietary data and/or operate in a heavily regulated industry (such as financial services, healthcare, or the public sector). Meanwhile AI comes with lots of opportunities for software companies, as they embed new AI capabilities in their existing offerings and charge for the added functionality.

The bottom line is that adaptability is more important than ever in the software space. But that could very well be an advantage for PE-owned software providers, as they should be able to move faster than companies in the public markets. And as it relates to private credit, software loans tend to be lower loan-to-value than in other industries. Furthermore, lenders such as Blackstone are saying software is the best-performing sector in their loan portfolio.

4. There are many different forms of Private Credit, and we need to make a greater distinction between them.

I wrote about this idea as well. The spike in redemptions is occurring in Direct Lending, a strategy that typically provides senior-secured, floating rate loans to private equity-backed companies. It's the largest category within Private Credit, and the two terms are often used interchangeably. For simplicity's sake, I do this too, including in the infographic above.

But there are many other flavours of Private Credit, such as asset-based finance (ABF), mortgage investment corporations, and small business lending. The other strategies are not facing the same redemption queue, and they have other advantages over Direct Lending. In particular, other forms of private credit tend to come with shorter term assets, which is especially helpful in generating liquidity in case redemptions surge.

It will be interesting to see if this episode leads to a greater distinction between different strategies within Private Credit. If it does, we may see a market share shift out of Direct Lending and towards strategies such as ABF. If it does not, then other strategies may see a spike in redemptions too.

5. This story is very different than the gatings that have happened in Canada.

At a high level, these Private Credit funds are doing exactly what they are supposed to do. They are all delivering 5% liquidity, with some going a bit overboard. They are certainly not cutting off redemptions altogether, nor are they cutting off cash distributions. And as mentioned earlier, have they have generally posted solid investment performance.

In Canada by contrast, the story has been much worse for many funds, especially in the real estate space. Some funds have cut off redemptions and cash distributions entirely, leaving unitholders feeling completely cut off from their investment. There are also serious questions about assumptions used to value assets in some funds. In the worst cases, there has been fraud.

6. This is proof too many investors got the wrong message going in; advisors need to do better.

As has been established thus far, the wave of redemptions is not caused by poor performance. And while there are concerns about credit quality, those concerns have yet to show up in the numbers. Rather, the suddenness of the redemption spike is very likely due to liquidity concerns; in other words, many investors fear being locked into their investment, and are trying to get their money out while they can. So the rise in redemptions has become self-reinforcing.

But if this is the mindset for these investors, they never should have been in Private Markets in the first place. These funds are meant to offer excess risk-adjusted returns in exchange for liquidity, and while these funds typically offer quarterly liquidity, this feature is never guaranteed. It's up to the advisor to make all this clear before investing their clients' money in these funds (at this point I'll draw attention to the first line in my call to action at the bottom of this newsletter).

But the redemption wave is evidence that these conversations were not happening nearly often enough, and that investors are learning the hard lessons too late.

7. Fund companies can do more to send the right message.

If an investor goes into a Private Markets fund with the wrong expectations, the blame mainly falls on the advisor. But the fund companies need to be part of the solution too.

A good start would be killing the "semi-liquid" label, a term that never should have been used in the first place, as it implies "some liquidity all the time". Fund companies also need to use this episode as an opportunity to better educate advisors, and encourage them not to sell their fund to people who need liquidity. The best companies have put in fundraising caps, to ensure they don't raise too much money too quickly, and other companies would do well to emulate this approach.

8. The media will always paint this industry with the worst brush, and it's up to everyone to deal with it.

Fund companies have argued throughout this whole episode that there is a disconnect between reality and how the press is reporting it. And there is a lot of truth to that, especially when it comes to fund performance and portfolio quality.

But this has always been the case; alarmist headlines for Private Markets have become the norm. This is partly due to the "if it bleeds, it leads" mentality, as negative headlines draw more eyeballs. One could argue it's also due to traditional asset managers, who compete with Private Credit every day, and always happy to pile on.

One should not expect this dynamic to change any time soon. So to complain about it is like complaining about gravity, because both will always be there. It's up to fund companies to deal with it appropriately, mainly by educating the public and helping advisors sell the right funds to the right people.

9. There is no sign (so far) that other asset classes are being affected.

Who knows how this will play out. Anecdotal evidence suggests that other private asset classes have not seen the same surge in redemptions, but this scenario is not out of the question. Investors could easily get nervous and race to pull their money out before gates come up. Alternatively, Private Credit investors may seek liquidity from other strategies out of necessity, such as Private Equity or Private Infrastructure. Because Blue Owl is at the heart of the current redemption cycle, other Blue Owl funds could be the next domino.

Or this could peter out. If the funds continue to perform, and the fund companies regain (some) control of the narrative, the redemption queue may gradually get dealt with over a few quarters. Time will tell.

10. Private Markets will ultimately benefit from the current turmoil.

To be clear, not many people are having fun in the midst of this turmoil (although I do enjoy writing about it). But over the long term, this could be one of the best things to happen in the Private Markets space. A stress event such as this helps to clarify how these products work, and also helps weed out investors that shouldn't have been in these funds in the first place.

One could also argue that such an event was bound to happen eventually; with every new asset class, there's inevitably a shakeout before the industry matures properly. In many ways the industry is lucky this didn't happen during a bear market, or during a recession, both of which could have made for a far worse panic.

Of course the key will be how the industry responds, and whether this is viewed as an opportunity for everyone to improve. If yes, then many individuals could eventually find themselves investing like institutions or family offices, with the same discipline too. Otherwise, one should expect more liquidity squeezes in the years ahead.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/