BTE Newsletter #26: The Biggest Private Credit Default Ever

Good morning everyone, Happy Tuesday!

Tomorrow I'll be at the CAASA Family Office Summit, this time just as an attendee, not as a panelist. It certainly would have been nice to be on stage again, but unfortunately they chose Miles Nadal over me (there's always next year). To those of you who are going as well, I'll see you there.

Regarding the podcast, after spending March recording a slew of episodes, I've spent April editing them. I hope to release the last of them this Sunday, and it features Ralph Desando of Yorkville Asset Management. A preview of that conversation is at the bottom of this newsletter. To listen to any of the episodes, or better yet subscribe, Apple/Spotify links are here:

|

|

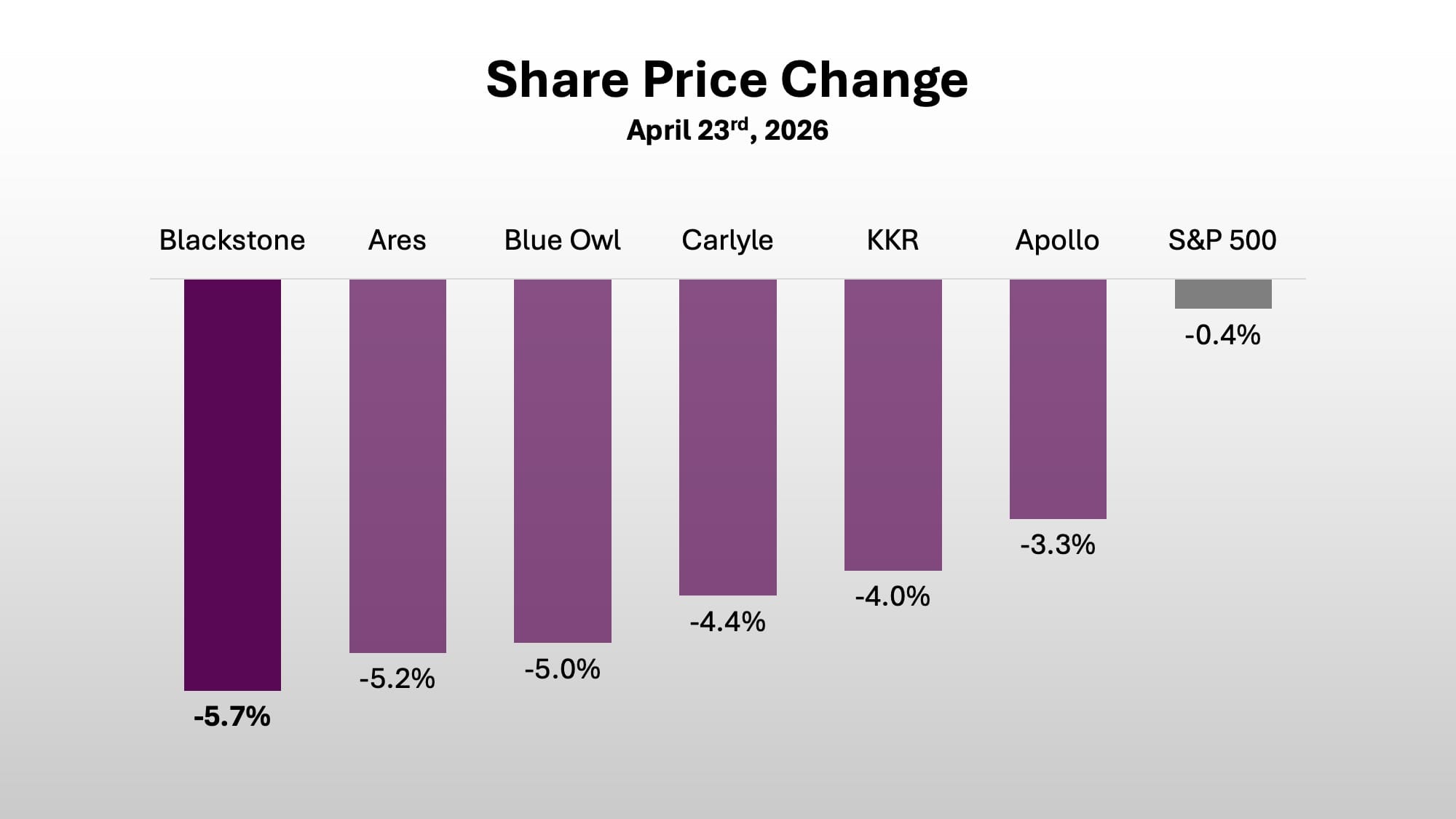

As for the main story, Blackstone kicked off earnings season for the alternative asset managers last week and slightly beat estimates. But the stock was down nearly 6% in response, and the results dragged down share prices for Blackstone's peers too. The main issue is the Credit/Insurance segment, which is seeing relatively weak fundraising and investment performance. Much of these issues are industry-wide and were well-known going into the quarter, but the results evidently did nothing to calm investor fears.

So below I'll take a closer look at Credit/Insurance, including the biggest problem loan that Blackstone is grappling with: Medallia. Whether this loan is a "cockroach" or more of an isolated incident is one of the biggest questions facing the alternative asset management industry right now.

Ben

A Closer Look at Blackstone

Blackstone reported Q1/2026 earnings on Thursday morning, with Distributable Earnings per share coming in at $1.36. That number was up 25% year-over-year and beat estimates by $0.02. Yet the stock sank by 6% the next day, and also pulled down share prices of other alternatives asset managers. So what exactly is going on?

The Credit/Insurance Segment

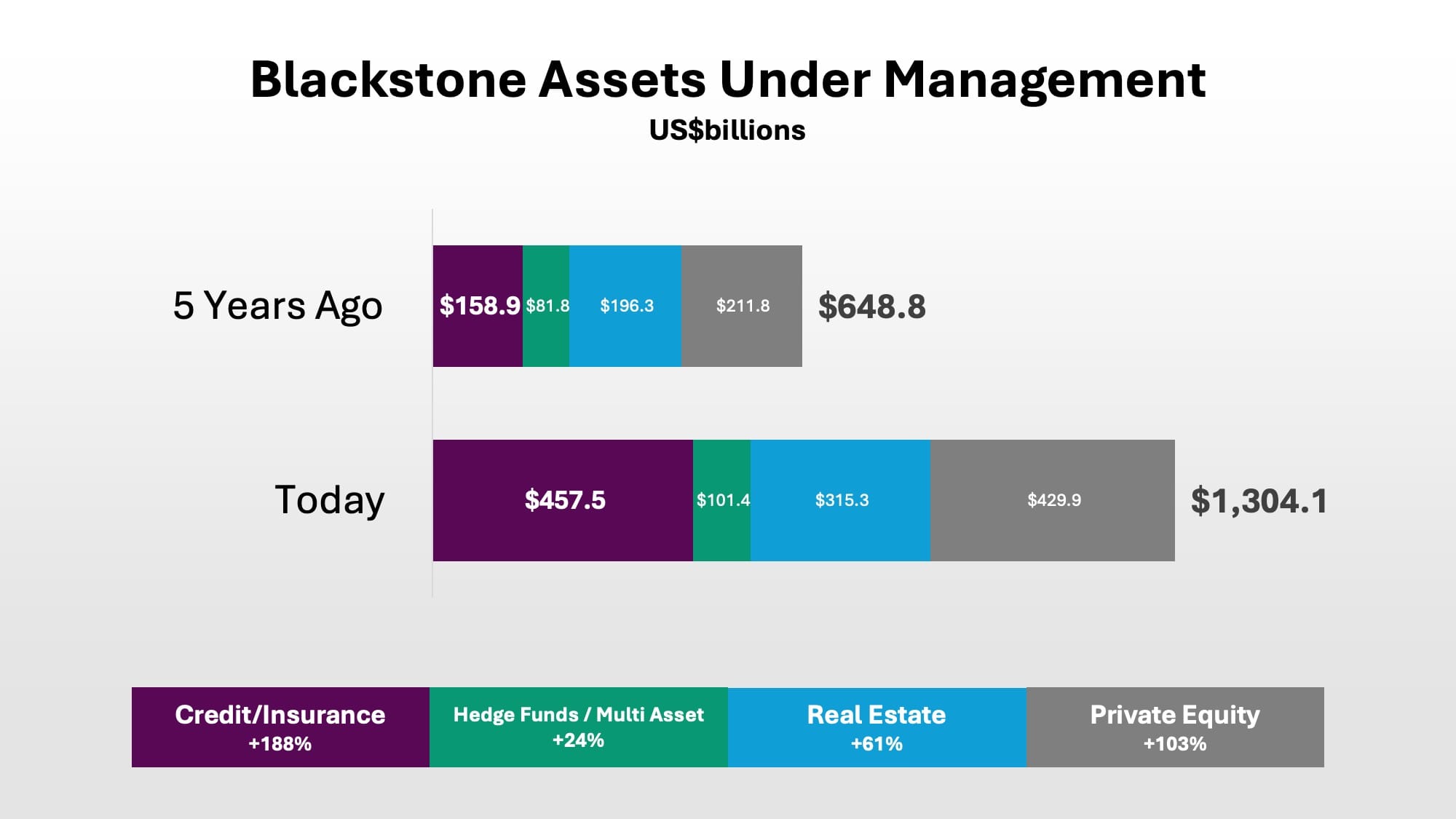

While alternative asset managers are often labeled “private equity companies,” Credit is the largest segment for many of them. Blackstone is one of these companies, with the Credit and Insurance segment now representing 35% of total assets under management, up from less than 25% five years ago.

So with Credit and Insurance being the largest strategy and the key growth driver, it's understandable why the segment would drive Blackstone's stock price ... both on the way up and the way down.

Another Spotlight on Credit

The issues in Private Credit industry-wide have been widely covered over the past 12 months, including by this newsletter. Major stories have included a couple high-profile bankruptcies last year, an unfortunate "cockroaches" comment from Jamie Dimon, two PR missteps from Blue Owl, fears about AI disruption in the software space, and a redemption queue in Private Credit funds forming this year.

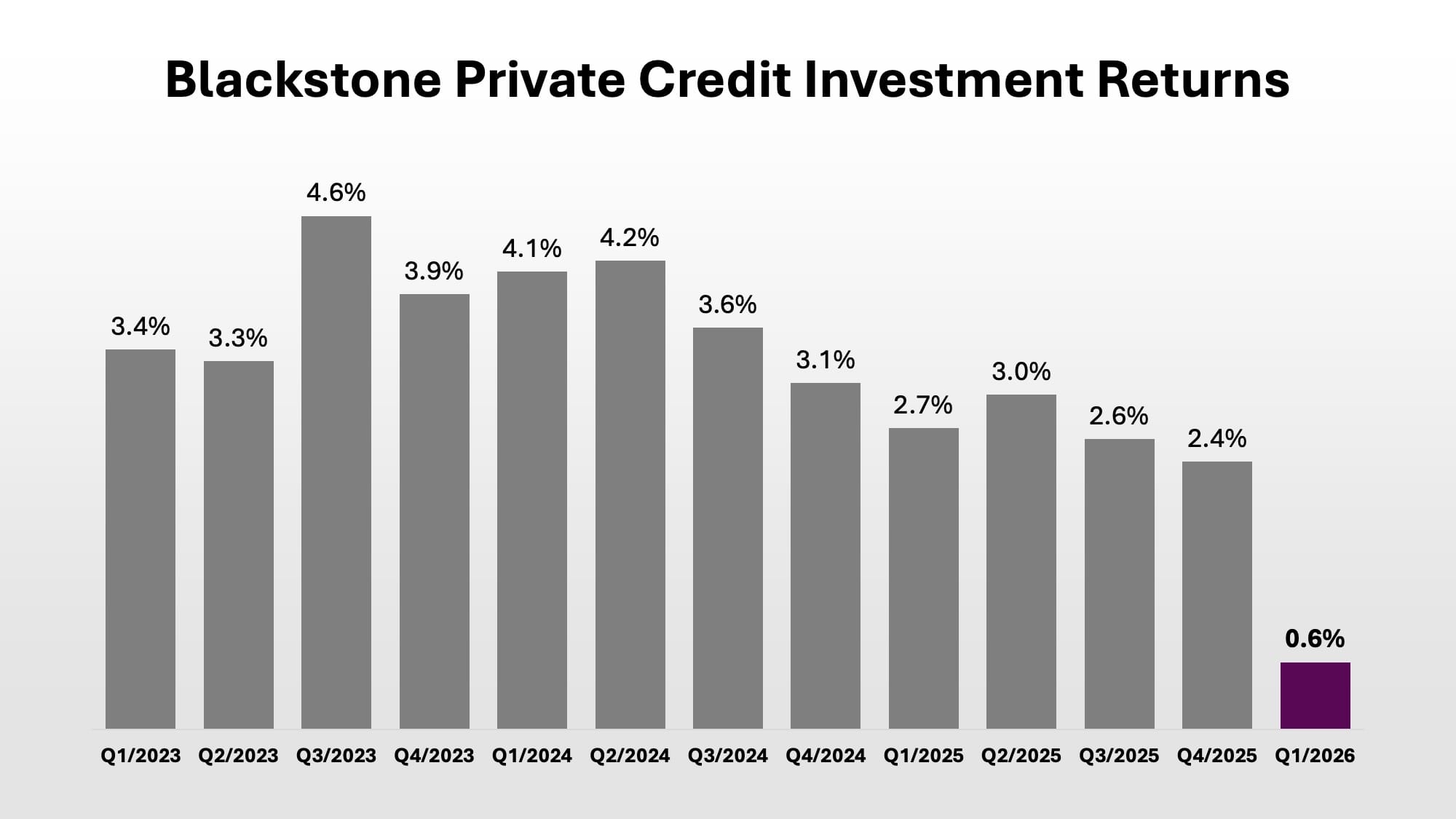

For the most part, these trends have only affected fundraising and sentiment in Private Credit, while investment performance has been quite solid. But in Blackstone's case, investment performance in Private Credit also turned sour in Q1, and given all the negative headlines about the asset class, the timing couldn't be worse.

Blackstone makes the case that even the most recent number is better than the leveraged loan market, which declined by 0.5% over the same period. But Q1's performance is still well below Blackstone's standard, especially since the numbers in the chart above are gross of fees.

Part of the problem has been out of Blackstone's control, particularly in the software space. As fears of AI disruption have grown, Private Credit loans in the space have traded down, even if those loans are not delinquent. Yet Blackstone is dealing with a couple of problem loans as well, and investors are worried whether these are part of a larger pattern (dare we call them "cockroaches"?).

The biggest one, and the one that's getting the most attention, is Medallia.

Medallia: A Big Price To Pay

Medallia is an Experience Management Software Platform, and according to its website, "unifies every customer signal and applies industry-leading AI to deliver the intelligence and outcomes today’s leaders need to transform their business." In plain English, the company analyzes customer feedback data to help companies improve their customer experiences.

Thoma Bravo, arguably the world's most respected software-focused private equity firm, purchased Medallia for $6.4 billion in 2021, a premium of nearly 30% to the company's 30-day unaffected average stock price.

This was at a time when valuations were especially high, particularly for technology companies, and the Medallia transaction was a case in point. Based on the company's guidance at the time, Thoma Bravo paid 11 times revenue, even though Medallia was also guiding for a 4% adjusted operating loss. Medallia had longer term targets of 20%+ subscription revenue growth, with a 20%+ adjusted operating margin, and presumably Thoma Bravo thought they could achieve those numbers as well, at a bare minimum.

Since Medallia was not yet profitable, it could not afford the debt levels typically seen in buyout transactions; Thoma Bravo had to finance about 70% of the deal with equity. With such a big equity cushion, lenders presumably felt safer and were willing to take a longer-term outlook, especially with a sponsor like Thoma Bravo at the wheel.

Of course with the benefit of hindsight, that turned out to be a false sense of security. Reports indicate Thoma Bravo is about to hand over Medallia to Blackstone and the other lenders. With $3 billion of debt currently outstanding, this would make Medallia the largest Private Credit default in history.

Is Medallia a SaaS Cockroach?

One of the big questions is whether this is simply an AI disruption story. According to Blackstone, the answer is no. The company's head of private credit, Brad Marshall, said back in February that Medallia's problems were "not because of anything related to AI, but due to what we believe to be execution-driven issues." As for Thoma Bravo, co-founder Orlando Bravo did not cite AI for Medallia's woes but instead quite simply said "we made a mistake, and that caused us to pay too much."

Other commentary has suggested that Medallia's problems are more structural. The company evaluates customer experiences largely based on survey data, which will always lead to biased results, since it relies on the people who went through the trouble to give feedback. Medallia has recognized the problem, and has moved to modernize the business, but that can only happen so fast, and meanwhile new competitors don't have the same legacy issues. In any case, Medallia clearly didn't move fast enough for Thoma Bravo or the lenders.

It's way too soon to conclude whether or not Medallia is a "cockroach." AI disruption certainly did not help Medallia as it tried to fend off newer competitors, but for a company that likely had structural issues, and execution issues, and was purchased for too much at the peak of the cycle, one cannot jump to any immediate conclusions. But time will tell.

BTE Podcast: Ralph Desando Interview (Preview)

Ben Sinclair

My guest today is Ralph DeSando, Deputy CEO at Yorkville Asset Management. Ralph joined Yorkville at its inception in 2010 and has led the growth of the firm's healthcare fund into one of Canada's leading healthcare investment platforms. In addition, Ralph has worked at Deloitte in its tax department, and was also an instructor at UofT's School of Continuing Studies in the area of credit and market risk management. Ralph, thank you very much for joining me.

Ralph Desando

My pleasure, Ben.

Ben Sinclair

So first, could you talk about your background prior to Yorkville? What was the path for you that led to joining a startup asset manager?

Ralph Desando

So my background at Deloitte was in tax, and I worked a lot with families in terms of their corporate reorganizations, acquisitions, estate planning, and generational transfers. I was always very entrepreneurial. I wanted to do it for myself.

Then when Hussein [Amad] was starting Yorkville, he asked me to come join him and I was actually in the middle of working with the family at Southbridge to build out a REIT for them. So it was serendipitous that basically the timing worked out. As Hussein was starting Yorkville, I was working on this healthcare project for Southbridge. And so with the skill sets that Yorkville brought to the table in terms of licensing, money management, and analytics, it really was a great fit for both of us to do this project together. And that's really how it started.

Ben Sinclair

And can you talk about the founding of Yorkville, the opportunity that you guys saw in the healthcare space, and how the firm evolved from 2010 onwards?

Ralph Desando

That’s a very good question. Healthcare has always been a fundamental pillar of the organization and its beliefs. We as an organization have always believed that healthcare can't just be fixed by the government alone and that it really is a partnership between the private sector and the government to build out an infrastructure that can actually benefit Canadians as a whole. That's the pillar of the organization. And that's really why the healthcare fund has fit so well with what we're doing.

When we build client portfolios, the healthcare fund becomes a very important part of that because of the consistency of the returns, the stability of the fund, the government contracts. So it helps with portfolio construction in a sense that it gives that volatility mitigation, it gives that consistent income, and provides access to a market that really isn't otherwise available to investors because of the significant barriers to entry that healthcare in Canada presents.

Ben Sinclair

Now most of the healthcare fund is in senior living. Can you talk about the nuances of that strategy?

Ralph Desando

Senior living, when we first started the fund was at a point where the infrastructure across Ontario had significantly aged, to the point where it was no longer useful for today's environment. The government had set aside a program where 35,000 beds needed to be redeveloped into modern standards. And we looked at that as an opportunity to build out a business, build out a fund, and really create change in the healthcare space. So that was the beginning and the reason and the rationale why, and we've been able to be extremely successful in achieving that change and improvement in Canadian healthcare.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/