BTE Newsletter #36: Why Has Real Estate Lagged, and Is There An Opportunity?

Good morning everyone, and Happy Tuesday once again. I hope you're all having a great summer so far.

Usually this is where I'll post all the wonderful exciting things I'm doing, but there's not much to report over the past week...or month. Unfortunately I haven't been to any World Cup matches, nor the Calgary Stampede. Instead I've been spending a lot more time looking after my 5-year-old son, who fell off his scooter and broke his leg at the end of May.

That being the case, I hope to have more podcast episodes out soon, and there should be more conferences once the fall begins. Until then I hope you're all enjoying the summer more than my son.

And speaking of hobbling, I've been meaning to write a thought piece on Real Estate for a little while. The asset class has struggled in recent years, and there's a lot to say on the matter. And more recently, some new interesting data points have come out, so the time for procrastination is over.

Ben

What's Going On With Real Estate?

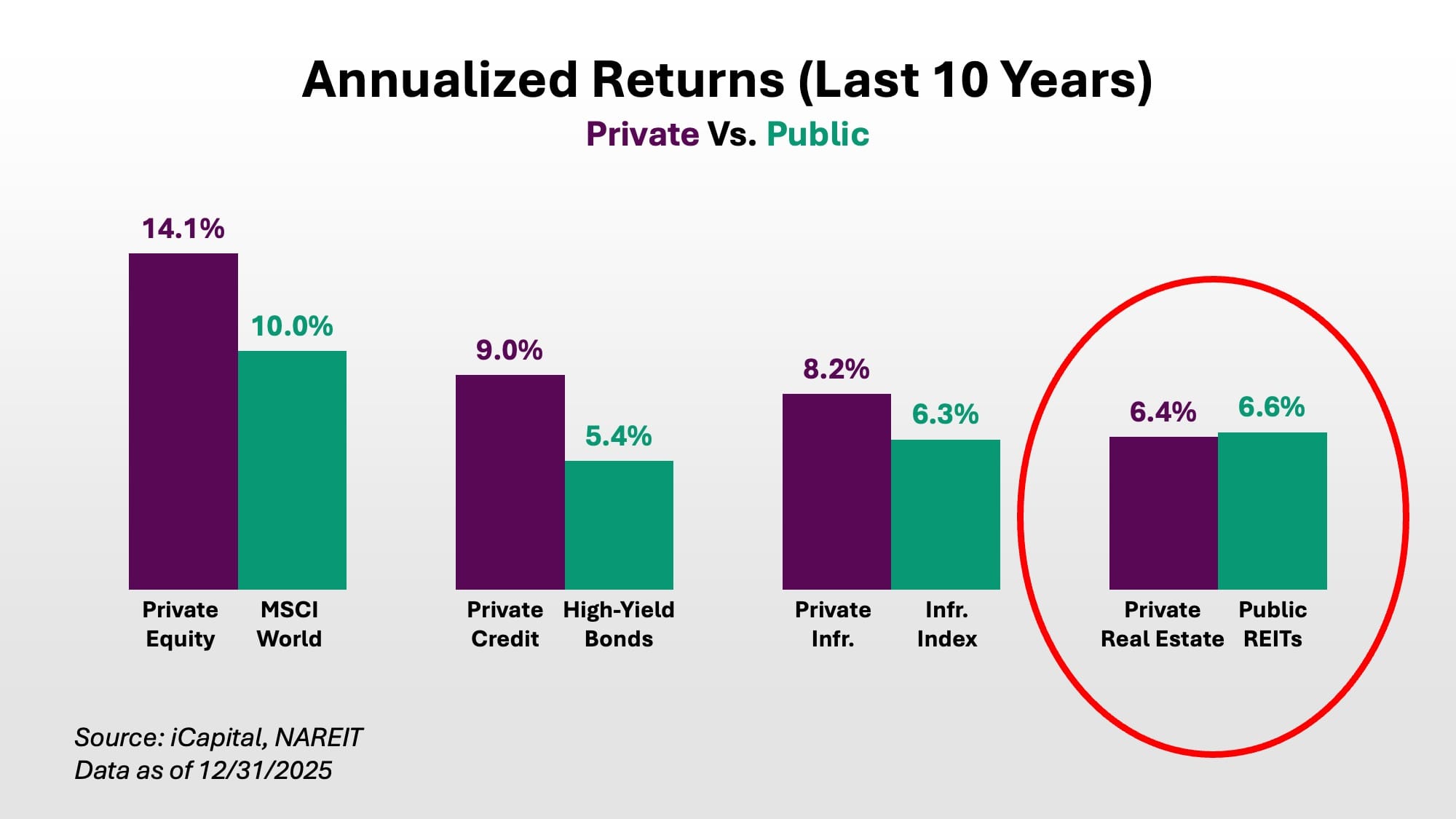

When considering the benefits of Private Markets broadly, it starts with a fairly simple tradeoff: for giving up some liquidity, investors expect better risk-adjusted returns. Historically that's proven to be the case with Private Equity (versus stocks), Private Credit (versus bonds), and Private Infrastructure (versus infrastructure-focused equity indices).

But Real Estate stands out as an exception; the category has not outperformed public REITs. On top of that, Real Estate (public or private) has been the worst performer among those four broad strategies.

Unsurprisingly, Real Estate has had especially weak investor demand in recent years, with relatively little money pouring into the space, on both the institutional side and among individual investors. So that brings up three key questions:

- Why has Private Real Estate not outperformed its public counterpart?

- Why has Real Estate lagged as a category?

- If investor demand is especially weak for Real Estate, is there a case to be made for being contrarian and riding a recovery?

Question 1: Why Has Private Real Estate Not Outperformed Public Real Estate?

There have been many studies comparing public and private assets, and they tend to reach similar conclusions. Private Credit has outperformed its public counterparts across practically all time periods. The same can be said for Private Infrastructure. Meanwhile Private Equity has lagged over the past 5 years but done better over a longer time frame. Yet Private Real Estate hasn't done any better than public REITs. So why has this been the case?

To help answer this question, JPMorgan put out a very good thought piece on the subject a couple of years ago, and they came to two conclusions:

- Public REITs use leverage more aggressively.

- Public REITs have more exposure to high performing subsectors.

Regarding the first point, public REITs have a big advantage over private funds: they can issue long-term fixed rate public bonds. Meanwhile private funds typically finance properties on a deal-by-deal basis using bank debt or private loans. The latter approach provides Private Real Estate with more flexibility (i.e. the ability to default on individual properties without affecting the rest of the portfolio), but this form of financing is also more expensive. JPMorgan found that public REITs have historically used this advantage to operate at higher leverage.

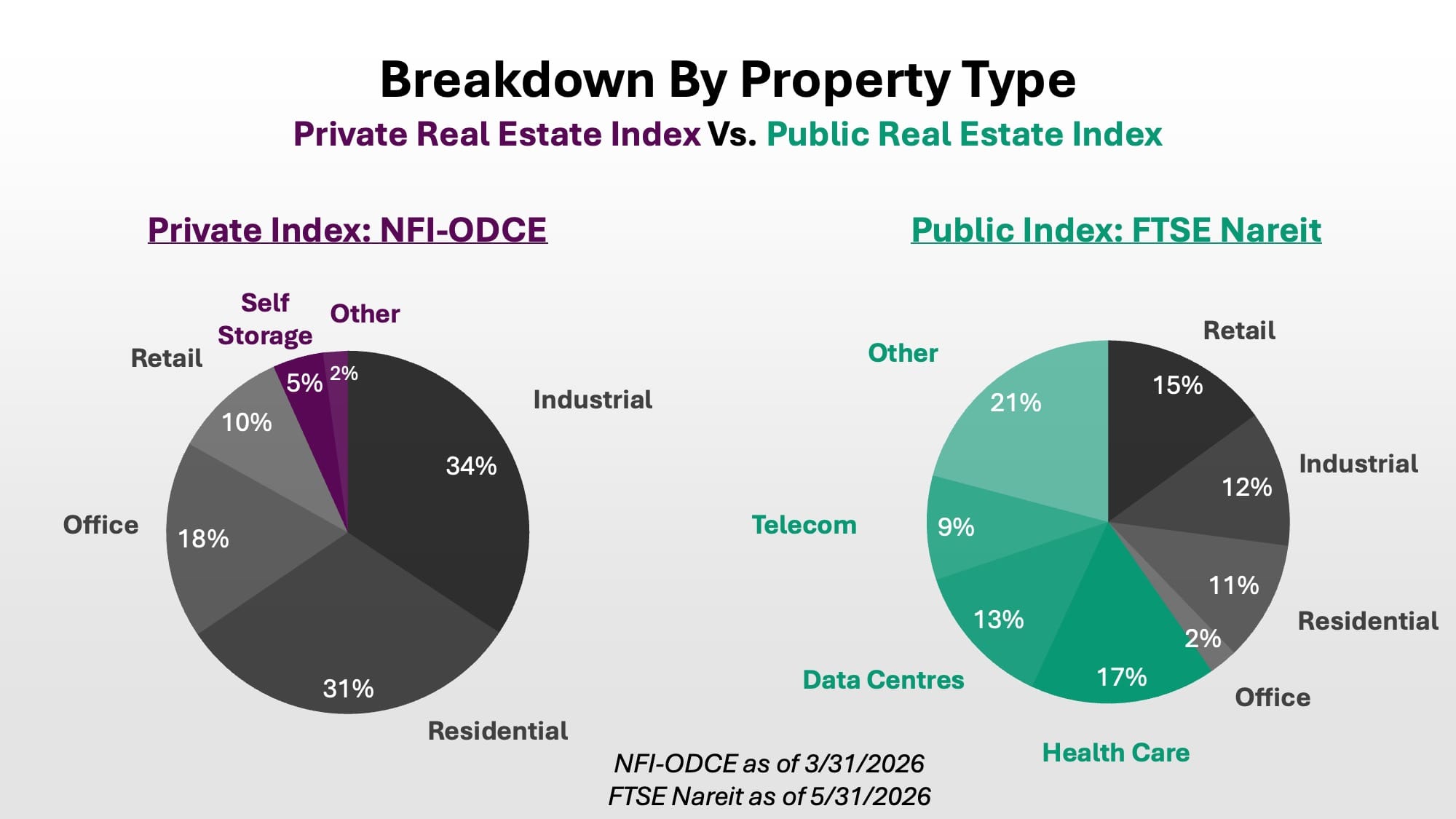

The second advantage public REITs have is what JPMorgan refers to as "Extended Sectors": self-storage, health care, data centres and telecommunications. These sectors are home to some of the best-performing REITs over a long time frame, but private REITs have relatively little exposure to them.

Question 2: Why Has Real Estate Struggled In General?

This question applies to all practically all of Real Estate, whether it's public REITs, private REITs, a new house in Brampton, or a condo in downtown Toronto. And there are a few answers:

- The main answer: rising interest rates, which of course decrease the present value of future cash flows associated with real estate. This dynamic gets worse when using short-term or floating-rate debt.

- Certain sectors have become less relevant post-pandemic, with Office being the best example.

- There has been a severe boom-bust cycle in certain sectors, leading to overbuilding.

- High inflation in 2022-2023 led to higher operating expenses, which is especially problematic in situations where rents cannot increase at the same rate (due to rent control, long-term leases, and/or lack of demand).

These dynamics have not applied to other areas of Private Markets to the same extent. Private Infrastructure largely benefits from inflation-linked cash flows, which was very helpful in 2022-2023, and these assets largely remain under-built. Private Credit is typically floating rate, so valuations were not severely impacted by rising rates. Meanwhile Private Equity has the opportunity to ride various tailwinds, such as the productivity gains from AI and/or rising public market valuations.

Question 3: Is There an Opportunity to Invest in Real Estate?

While Real Estate investments have struggled, there are two arguments to be made for the asset class:

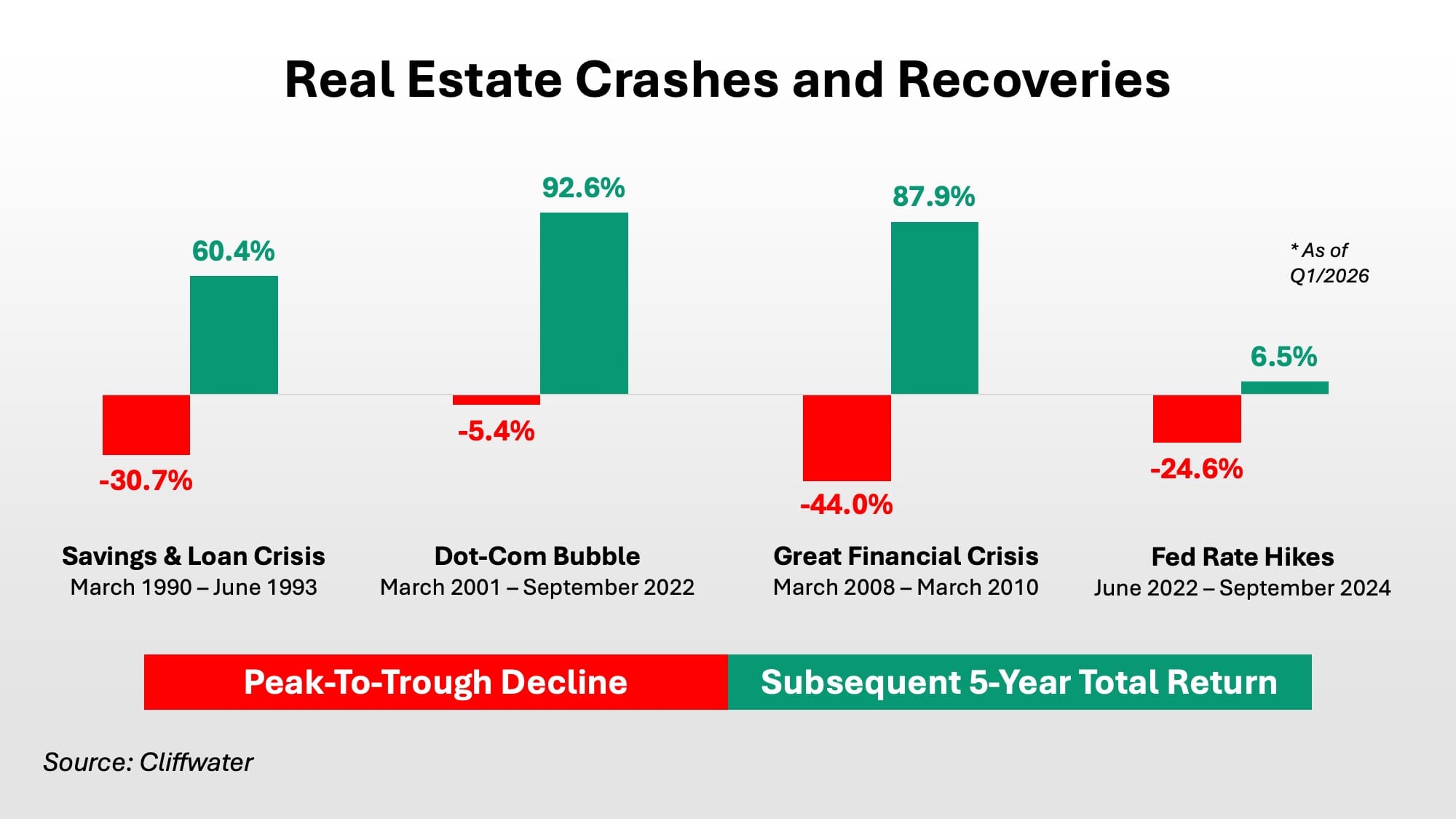

- Real Estate is due for a recovery, and history suggests that this will happen.

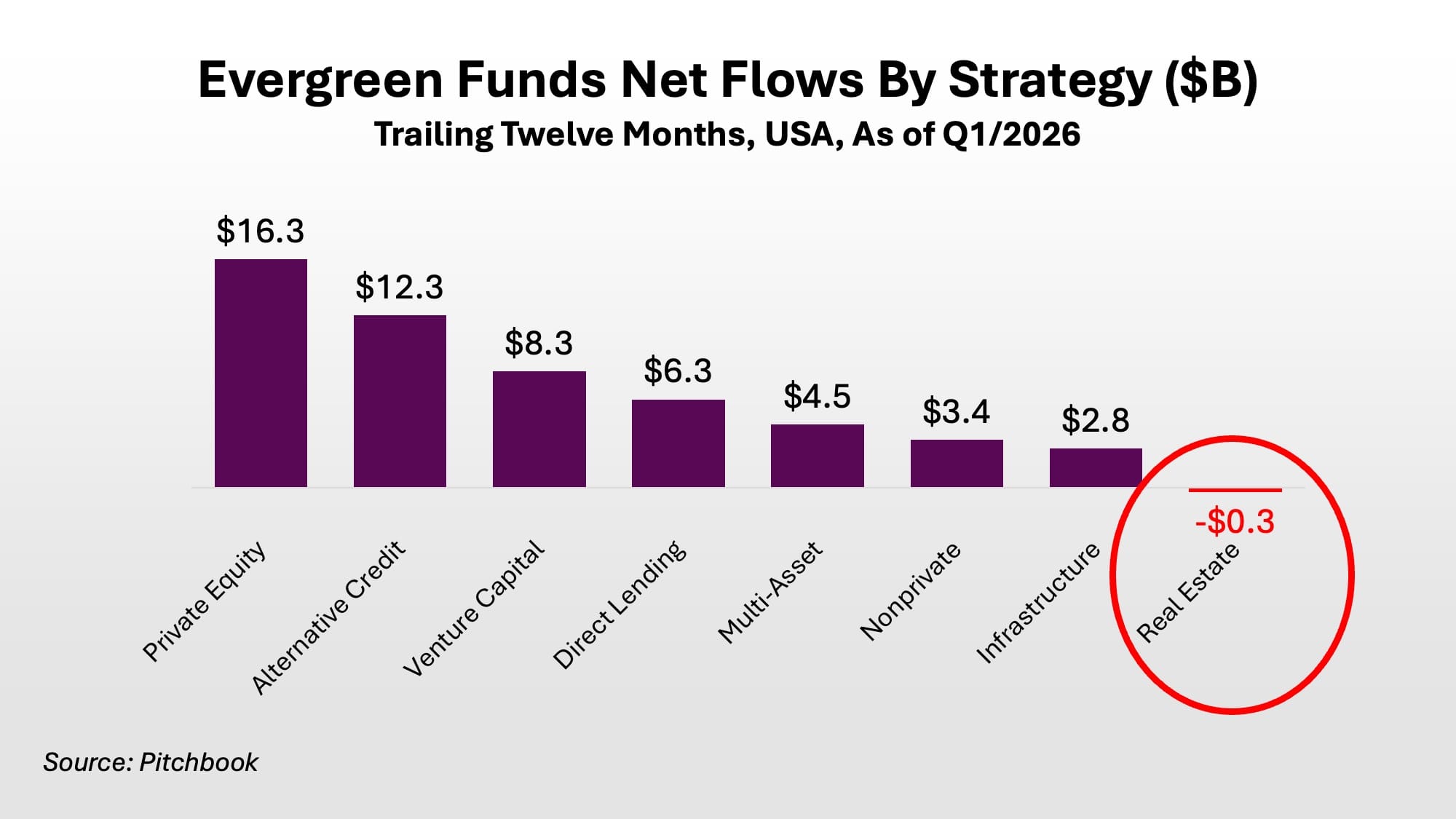

- There is less capital chasing Real Estate, so there's an opportunity for a contrarian bet.

Regarding the first point, history shows that Real Estate has always recovered following downturns. This is partly because prices are depressed at the bottom, and thus have lots lots of potential upside. It's also because there's a lack of new construction during the downturns. Of course it's impossible to predict the bottom, and it can take a while for supply to adjust downwards (since preexisting construction projects may still come online during downturns), but patient and contrarian investors have certainly been rewarded in the past.

Regarding the second argument, there is relatively little appetite from investors for Private Real Estate. And that's a big contrast from other areas of Private Markets, where headlines speak of a "flood" of investor money pouring in. Many commentators have stated (with good reason) that one generally shouldn't chase the hottest asset classes with the crowds, so there's certainly a case for doing the opposite.

There are other factors to consider. One is valuation: in down markets, there's an argument that Private Real Estate funds do not mark down their assets sufficiently (in fairness, home sellers often behave similarly), and the contrarian bet would be better made in the public markets. Another factor concerns breadth; not all real estate funds are the same, and certain strategies have their own unique appeal. I've talked about some of these strategies on my podcast, including Senior Living, Industrial, and Opportunistic strategies.

At a high level, Real Estate is meant to provide diversification to a traditional stock & bond portfolio, and even though that promise not always been met in the past, I still see a role for the asset class to play. If you want more specificity than that, you'll have to reach out 👇

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/