BTE Newsletter #25: Not All Private Equity Is the Same Thing!

Good morning once again,

First things first, I'm happy to report The Globe & Mail published my second op-ed. It was a follow-up to this newsletter piece, in which I highlighted some of the pitfalls for senior citizens in private funds, particularly when those funds are gated.

Also, most of you know that I'm quite active on LinkedIn, and this is how people typically find the newsletter too. So I'm always looking for more ways to reach people through the platform.

A couple weeks ago, I posted my first infographic on LinkedIn, and got a very good response. It seems people like the bite-sized information in visual form (makes sense) so I've committed to doing a lot more. But I can't promise they'll all make it into this newsletter. So if any of you are still not connected to me on LinkedIn, feel free to reach out. My profile is here.

Not long before the infographic, I wrote a newsletter piece called "Not All Private Credit Is The Same Thing!", along with a goofy ice-cream-themed cover image. It was in response to some reporting that I saw as missing the nuanced differences between different Private Credit strategies. That also got a positive response, so I thought it would be good to write an overview for the various categories within Private Equity. Not unlike the Private Credit piece, this one is relatively high level. Hope you enjoy it.

Ben

The Many Different Flavours of Private Equity

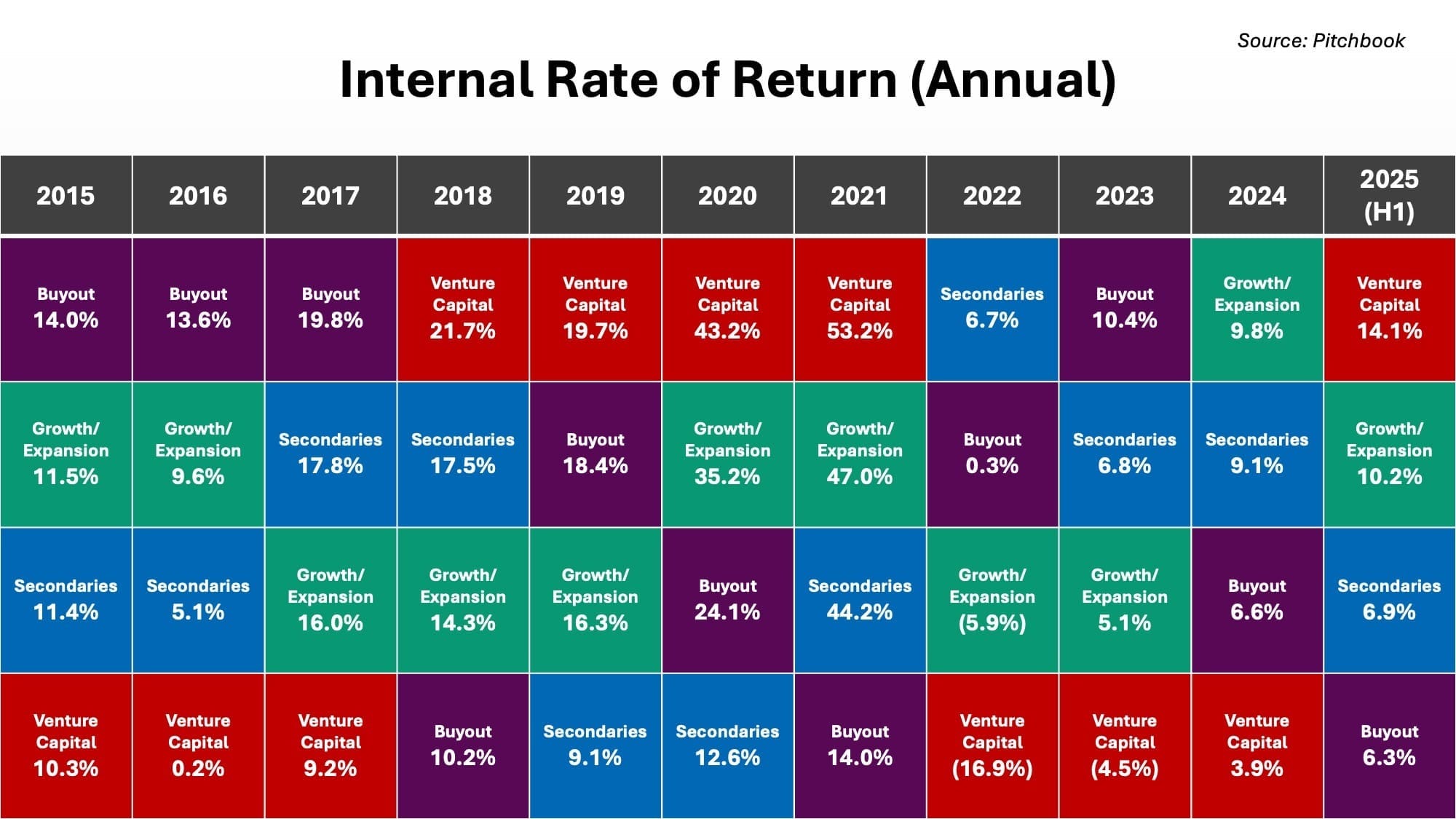

Not unlike Private credit, any other asset class for that matter, the media tends to paint Private Equity with a very broad brush. Headlines and articles rarely distinguish among the many distinct strategies in the space, each of which has its own underlying dynamics. The quilt chart below makes this clear: performance varies widely across strategies over time, and even this illustration only scratches the surface.

Below we take a look at each of the strategies in the chart:

Buyout

Buyout is the largest segment within Private Equity, and the two terms are often used interchangeably. In a typical “leveraged buyout,” a Private Equity firm acquires a business using substantial debt, then looks to improve the business's operations and profitability. The firm usually holds the business for five to seven years, though holding periods can vary, before exiting through an IPO, sale to a strategic buyer, or a secondary transaction with another private equity firm.

Historically, Buyout funds have outperformed public markets, although comparisons depend heavily on methodology. Buyout returns look less compelling relative to high flying benchmarks such as the S&P 500, but look better versus more diversified indices such as the MSCI World. Buyout performance has also lagged public equities in recent years but has outperformed over longer horizons. Meanwhile some studies compare Buyout to a levered public index, arguing this is more of an apples-to-apples assessment given the leverage used in Buyout transactions; again doing so makes Buyout returns look less appealing.

That being the case, leverage used in Buyout transactions has come down substantially. Back in the 1980s, a typical transaction would be financed 90%+ by debt. By the 2010s, that number had sunk into the 50s. Then when interest rates climbed in 2022, and businesses were not able to handle as much leverage, that number sunk below 50%. Furthermore, Buyout firms argue that they focus on relatively stable businesses, and these businesses are thus able to handle more leverage than the typical public company.

For evergreen funds and individual investors, there is a compelling case for Buyout exposure. Investors already own stakes in businesses through public equities, so Buyout funds can serve as a comparable yet less liquid alternative. Buyout strategies also tend to offer greater stability than Venture Capital or Growth Equity (see below). In addition, the evergreen fund structure allows firms to hold investments much longer than traditional drawdown funds. Without the pressure to exit within a fixed timeframe, Buyout firms can be more attractive acquirers, as founders are often more comfortable selling to long-term owners.

The drawback is that Buyout investments are far less liquid than public equities, and it remains to be seen how significant that limitation will become. Buyout firms thus require a steady stream of quality deals to deploy new capital efficiently, and they also may face challenges generating enough liquidity when investors seek redemptions. We’ve already seen similar pressures emerge in Private Credit, an asset class that is more liquid and stable than Buyout.

Venture Capital & Growth Equity

Venture Capital (VC) is arguably the most dynamic category within Private Equity, home to many of the industry’s most transformative success stories. VC focuses on investing in fast-growing businesses that typically do not generate free cash flow and therefore require additional funding as they scale. Unlike Buyout strategies, leverage plays a minimal role, and returns tend to be far more uneven, often driven by a small number of home runs. One can see this in the quilt chart above, where VC returns finish first or last in every year.

Two big trends have shaped VC in recent years. One is its growing presence in later-stage companies, as more firms delay or skip public listings entirely. The other, more recent trend is the surge in AI investment, which now dominates VC funding activity. Both have been especially visible this year, with large AI firms such as OpenAI and Anthropic attracting massive rounds of private capital ahead of potential IPOs.

Growth Equity sits squarely between Venture Capital and Buyout. The strategy focuses on acquiring minority stakes in fast-growing, established companies that use little to no leverage. These businesses are generally self-sustaining and not reliant on raising additional capital to reach their next stage of growth, which makes Growth Equity a more balanced approach between early-stage risk and mature-company stability.

But these strategies are quite tricky for individual investors to buy into through evergreens. Individuals are generally less accustomed with VC's lumpy return profile, which can make the experience very unnerving. Deal flow and liquidity can also be a significant constraint, particularly at unfavourable points in the cycle.

Some firms have experimented with offering these strategies to individuals, including via secondary investments (see below), but it is still too early to judge how successful they will be. It may be appealing to gain exposure to the next SpaceX, OpenAI, or Stripe, yet investors should be cautious about chasing the latest “shiny object” without fully understanding the risks and dynamics involved.

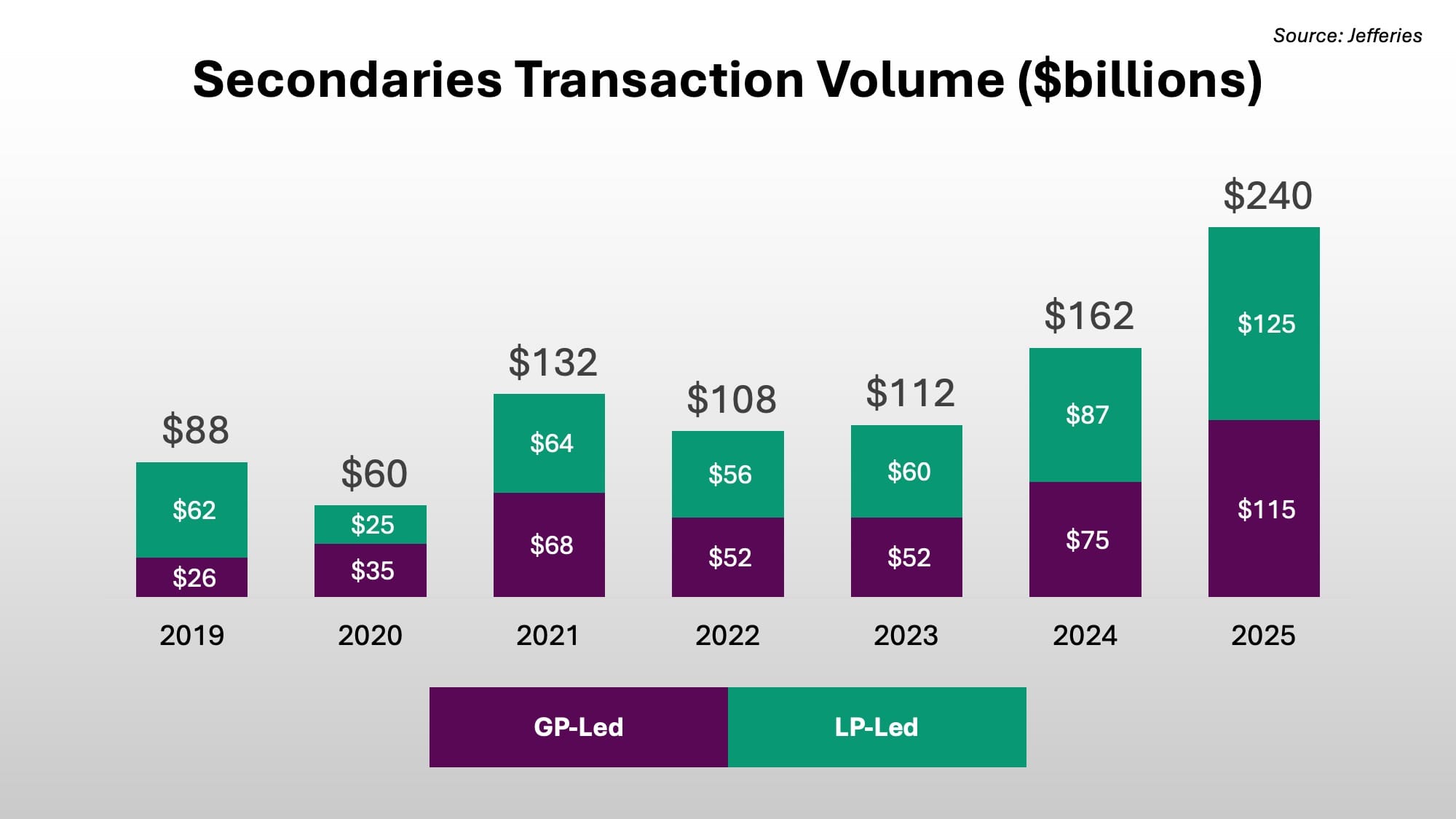

Secondaries & Co-investments

In private markets, “secondaries” are transactions where an investor buys an existing interest in a private fund or its underlying assets from another investor, rather than committing new capital to a fresh (“primary”) fund.

This can take a couple of forms. In an “LP-led” secondary, a buyer acquires a fund interest directly from an existing fund investor. In a “GP-led” secondary, one or more assets in a fund are moved into a new vehicle, and the original fund investors get a choice between taking cash or rolling their investment into this new structure. Because most investors opt for cash, GP-led secondary buyers step in with fresh capital to fill the void.

The secondary market has grown rapidly in recent years, particularly in the GP-led segment, as more funds have struggled to generate liquidity through traditional exits. Secondaries activity, once concentrated primarily in Buyout, has also moved into other strategies, including VC/Growth, Credit, Infrastructure, and Real Estate.

Co-investments, by contrast, involve an investor participating directly in a specific deal alongside a lead manager, effectively buying into that manager’s underlying investment. In both secondaries and co-investments, success depends heavily on strong relationships with other managers, thus providing access to high-quality deals. Speed and flexibility are also critical, since many of these transactions are time-sensitive and/or complex.

Secondaries and co-investments are arguably the most appealing approaches for individuals and evergreen funds. For starters, Secondary strategies tend to be more stable than traditional Buyout funds, because they generally involve purchasing seasoned portfolios after the original investors have navigated the early execution and underwriting risks. They also often offer greater liquidity and diversification than a single Buyout fund, particularly when the Secondaries manager has deep relationships with other managers.

Many observers also argue that there is still not enough capital dedicated to Secondaries, especially as more fund investors seek liquidity through the secondary market. A similar dynamic is playing out in Private Credit, where managers are under pressure to create liquidity to meet redemptions.

The main point sticking point is valuation, especially in LP-led transactions. In an evergreen structure, managers may acquire fund interests at a discount and then immediately mark them up to par. That can provide a short-term uplift for existing investors in the secondary fund, but it weighs on longer-term returns, and also leaves new investors effectively buying in at an elevated valuation. Secondary managers counter that this dynamic represents only a small portion of their overall return profile. In addition, this issue is far less pronounced in GP-led secondaries and is generally not a concern for co-investments.

Conclusion: Take Your Pick

It is no longer sufficient to simply decide to invest in Private Equity; much like in Private Credit, investors now face a wide range of strategies and structures to sort through. This overview is not exhaustive, and institutional investors in particular can access additional niche strategies, as well as choose between large-cap and small-cap managers or different geographies.

At the same time, media coverage will likely continue to gloss over the differences between strategies in Private Equity. That is understandable, since detailed distinctions between strategies will never generate clicks. However when making investment decisions, it is important to understand the basic differences among these approaches, just as investors would differentiate between sectors, styles, or regions in public markets.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/