BTE Newsletter #22: Not All Private Credit Is The Same Thing!

Good morning everyone,

Last week I had the pleasure of sitting on a panel at the CAASA Wealth Managers' Forum, alongside Brian Wong of Morgan Stanley, Tom Johnston of iCapital, and (moderator) Guillaume Lavoie of Torys. Together we talked about innovation in product shelves as it relates to private markets, but given what's happening in private credit, the conversation naturally veered in that direction (I was probably most guilty of this).

But there's another side to this story: private credit comes in a bunch of different forms, and very often commentators lump them all into one category. Again I am quite guilty of this, as I try not to put too much jargon in this newsletter. But right now there is a liquidity squeeze in one of the subcategories (Direct Lending), with Apollo and Ares joining a growing list of fund managers restricting redemptions. Meanwhile while there are multiple other Private Credit strategies available to Canadian investors that aren't going through the same thing.

So for this newsletter I wanted to give an overview of (some of) the different categories that all could be referred to as Private Credit: Direct Lending, Asset-Backed Finance, Small Business Lending, Mortgage Investment Corporations, and Venture Capital Debt. All of these categories are available to individual investors in Canada.

Meanwhile on the podcast front, Episode 9 with Jay Simmons of Durum Capital has now been edited and should be released Sunday. A preview of the conversation is below.

Ben

The Many Different Flavours of Private Credit

Direct Lending

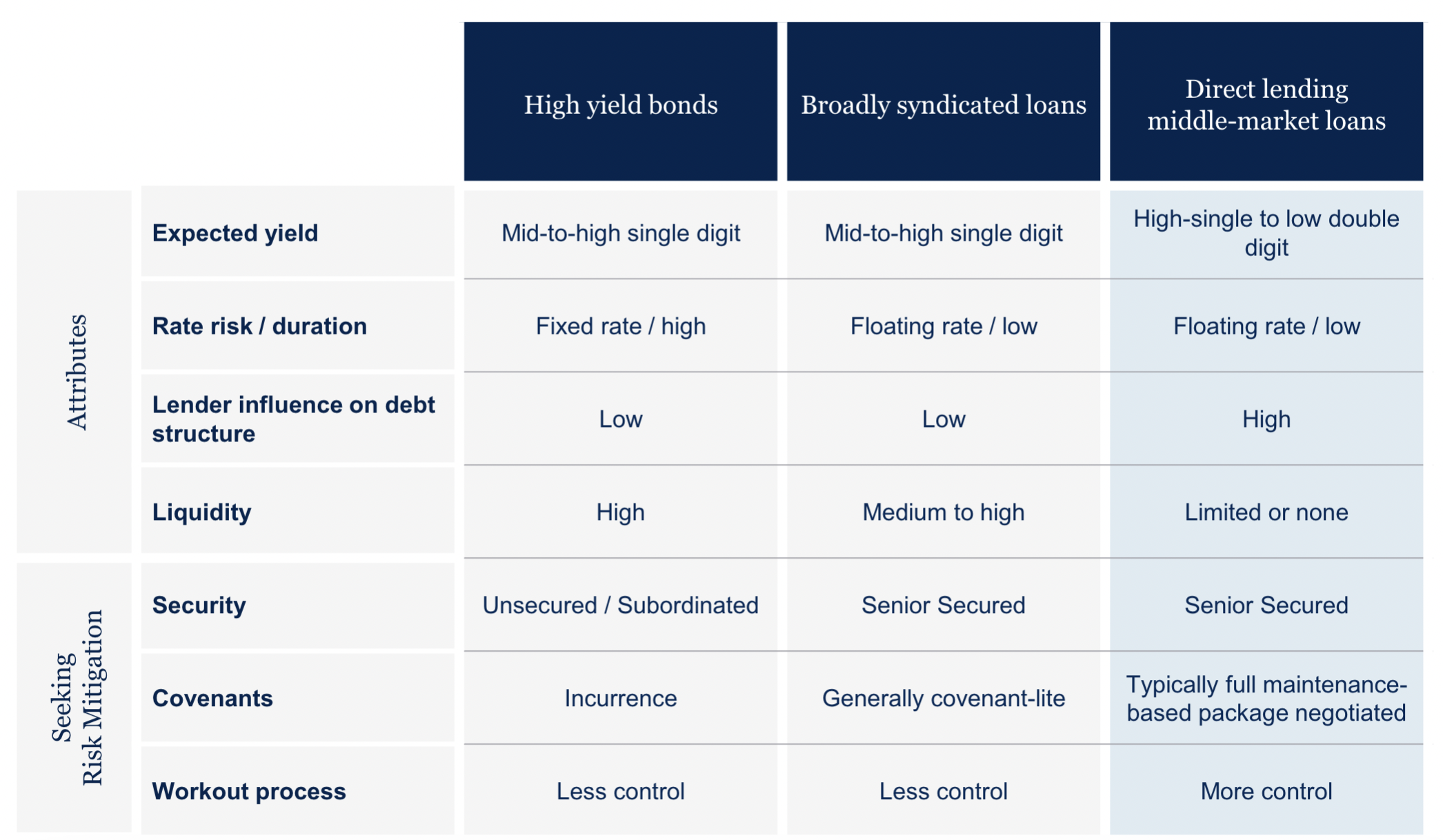

Direct Lending is the largest category within private credit, and the two terms are often used interchangeably. At a high level, Direct Lending is typically floating-rate, senior-secured loans to private equity-backed companies. Term lengths tend to be 5-7 years, matching the typical time horizon for a private equity company owning a business before selling it. Direct Lending competes with Broadly Syndicated Loans (originated by banks, then distributed to a variety of investors) and High-Yield Bonds.

Direct Lending comes with a number of attractive elements for borrowers, the main one being an opportunity to work directly with a small number of lenders, thus creating a more of a partnership approach. This helps at origination, as pricing can be more predictable, and more creative structures are possible. This also helps throughout the term of the loan, especially when the borrower wants to amend the terms or borrow more money.

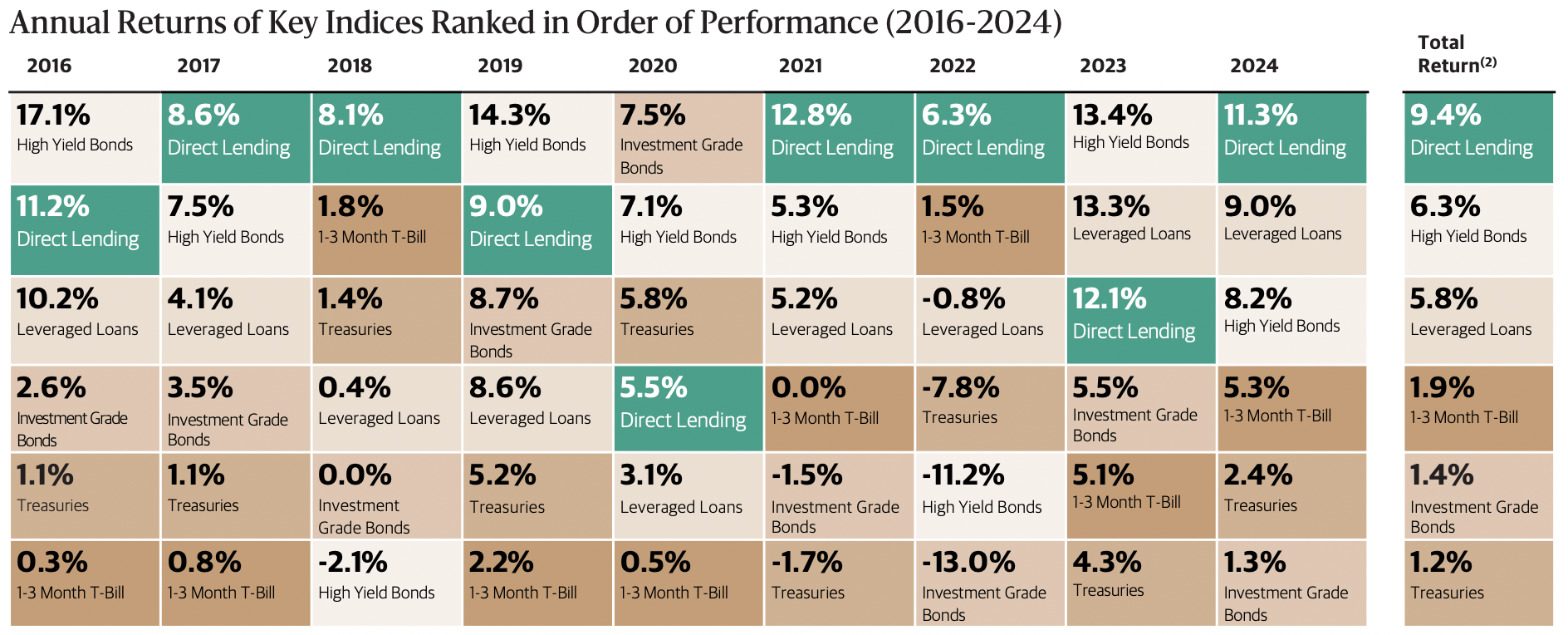

There are also a number of benefits for lenders. Yields are higher and covenants are tighter than other forms of lending, thus helping to protect lenders when the borrower runs into trouble. As a result, historical returns for Direct Lending have been higher and more consistent than other credit strategies.

Of course the major tradeoff is liquidity. Direct Lending is much less liquid than other credit strategies, and the industry is coming to terms with that nowadays. Funds from Morgan Stanley, BlackRock, Cliffwater, Morgan Stanley, Monroe Capital, Ares and Apollo have all (partially) restricted redemptions, as investors rush for the exits.

Furthermore, individual investors typically access Direct Lending through a Business Development Company (BDC) structure, which come with material fee structures and embedded leverage. Some BDCs have a public listing, allowing investors to get constant/immediate liquidity, but the S&P BDC Index has fallen by 25% over the last year as sentiment worsens.

All told, Direct Lending has stood the test of time, and despite some jitters about underwriting standards (particularly in the software sector) performance has continued to hold up well. Private BDCs have arguably become less attractive while so many of them restrict redemptions and while public BDCs trade at such big discounts to net asset value. But the strategy still has its advantages, and is worth watching closely.

Asset-Backed Finance (ABF)

Often referred to as "Alternative Credit", ABF involves lending not to operating businesses, but instead on assets such as auto loans, credit card loans, equipment leases, aircraft, railcars, investment funds, media rights, or music royalties. ABF has traditionally been the domain of banks, but has increasingly been moving towards alternative asset managers as banks look to step back from more capital-intensive business lines.

ABF has a number of advantages for investors. One is the very large end markets, allowing lenders to be more selective. Deals can often be quite complex/bespoke, allowing experienced managers with strong relationships to craft deals to their liking, with attractive yields and ample downside protection.

The other major advantage is the short-term nature of the assets, which are often less than 2 years. This helps significantly with liquidity; as a large portion of the portfolio turns to cash every quarter, the manager can return that cash to investors if redemptions spike. Shorter-duration assets are also easier to value properly, and they allow the manager to be more nimble in response to changing economic conditions.

Small Business Lending

When small business owners look for financing, it can be quite difficult to deal with banks, especially if the borrower has no real estate to use as collateral. But there are private lenders that offer small business financing, and Canadian individuals can invest in these loans. I recently did a podcast with one of the leaders in the space, David Gens of Merchant Growth (which can be listened to on Spotify or Apple), and there are a couple other funds available that focus more on the United States.

These funds can be thought of as private credit with more torque, with higher risk, higher return targets, and more cyclicality. And unlike Direct Lending, this strategy does not use leverage at the fund level to generate returns.

But this category has another advantage, and it's similar to an advantage of ABF: these loans are short-term, typically about a year. So that means the portfolio generates lots of cash as loans are repaid, there's less uncertainty about valuations, and there's more ability to adjust to changing economic conditions.

Mortgage Investment Corporations

Not unlike some of the other private credit categories, Mortgage Investment Corporations (MICs) benefit from offering very short-term loans. In a recent podcast episode with two MIC executives (again one can listen on Spotify or Apple), they explained that their mortgages have a one-year term, and are meant to be a bridge financing option for borrowers that don't fit the rigid lending criteria of banks.

Also not unlike ABF, mortgages benefit from having hard assets (e.g. a house) as collateral, helping to provide ample downside protection in the case of default. Furthermore, a home is so critical to a person's livelihood that they'll typically do whatever it takes to stay current on a mortgage. Contrast that with Direct Lending, where a private equity company may be quite willing to give up on an investment when the associated debt burden becomes too high.

Of course MICs are not risk-free. They are still lending to borrowers who are unable to get cheaper financing from banks. A really bad real estate cycle could also eat into collateral values. If a MIC ventures into higher-risk categories, such as construction loans, that could also spell trouble for investors.

Venture-Capital Debt

Lending to venture-capital backed companies is one of the highest-risk forms of private credit, if not the highest. The borrowers typically reinvest the bulk of their cash flow back into the business, leaving little wiggle room for debt servicing. When it comes time to pay back the loan, the borrower would usually have to raise another round of capital, which is never guaranteed.

There are ways that lenders mitigate these risks. One is by demanding lucrative terms, whether that be higher interest rates, some sort of equity participation, or both. Loan-to-value ratios are also quite small in VC Debt, typically sub-20%, so there's lots of equity cushion underneath the lender if the borrower has trouble raising more capital.

It's also worth mentioning that this market opened up significantly with the failure of Silicon Valley Bank in 2023. SVB was a major player in VC Debt, and while the bank's downfall was due to other factors, removing a large lender from the market created a void that other players have been happy to fill.

Conclusion: Private Credit Is NOT Just One Thing

This was not meant to be an exhaustive list; there are many other forms of private credit, such as junior/mezzanine financing, distressed debt, commercial real estate debt, and litigation finance. There are also differences based on geography, size of borrower, and vintage years. Institutions have the most choice, but individual investors in Canada have access to a broad range of strategies too, including all of the categories summarized above.

As it relates to this newsletter, normally I try not to have such an academic tone, and this information is available from multiple sources. But with tonnes of headlines talking about worries related to private credit, I think it's worth going over some of the different strategies, especially when just one of them is causing all the scary headlines.

Podcast Preview: Episode 9 With Jay Simmons

Ben Sinclair

My guest today is Jay Simmons, founder, chairman, and CEO of Durum Capital, a Calgary-based alternative asset manager with investments in land development, industrial real estate, carbon markets, energy, and an industry-agnostic Opportunities Fund.

Jay started his career in financial restructuring and insolvency at Deloitte. He has also led a power-focused private equity fund and has held multiple leadership positions in the oilfield services business, all prior to founding Durum in 2012. Jay, thank you very much for joining me.

Jay Simmons

Morning, thanks for having me.

Ben Sinclair

So I was wondering if we could start by talking about your first position in financial restructuring and insolvency. That must have come with quite a few lessons coming out of school. So can you talk about those lessons and how they shaped you in the rest of your career?

Jay Simmons

That's a great question. So I came out of Deloitte and doing accounting was the most unnatural thing I'd ever done. It was quite painful for me. And so when I passed my uniform final exam, which is what it was called at the time, I had already arranged to move myself down to the insolvency group. At Deloitte they called it the Financial and Special Services group.

And literally I moved down there the millisecond I could, the day I got my results back, which was quite fun. Leaving the doldrums of audit and stepping into this area where they have companies that are in trouble, and problems happening all over the place, you actually get to go in and run these companies very, very early in your career, because somebody has to take it over. When it's insolvent, it's been passed over to a monitor or a receiver. So there are lots of different things to learn around all of that.

A couple of the big takeaways that came from it is the value of a company quickly goes to zero when it gets into trouble. If you think of the companies in the marketplace that trade at a serious multiple over the book value of the firm, they'll trade at a cashflow multiple or something like that. Those same companies will trade at a discount to NAV when they have solvency issues. And so that spectrum of value difference is really quite interesting. And for me, it's become a little bit of a lifelong challenge to try to step in and find ways to capture that delta between the two.

So that's one piece that came out of it. And the second piece that came out of that, and a couple of other lessons in life, is that the caliber and quality of governance around businesses really matters. And generally there's a repeating pattern of companies that get into trouble of having boards at the helm that are not very good, or basically no governance at all.

So it's a great spot to start. You get to see all the bad things happening and there's lots of upside to be had out there, but it's good to stop to take a look at all the bad things that can happen. And it builds a really good risk response in an individual, or for me, I think it did that.

Ben Sinclair

Fair to say that seeing all these bad things has helped you avoid them in your positions later on?

Jay Simmons

Yeah, my first adventure in the nature of trade, we turned around an oilfield services firm. And I remember when I turned 30, we had 300 employees and I thought I was a guy about town. And then I lived through a decline in energy prices. And when I was 31 I almost had a bankruptcy, which I didn't, thank God, but what a great time to get that experience in life.

By that I mean all the insolvency pieces, and then going out and taking a chance and hitting it really well. Things turned out great for us. And then the market turned in the opposite direction. And actually I would say we had governance issues in our little shop too. So I was getting a bunch of the good lessons that came from all of that stuff.

Ben Sinclair

Well, this wasn't the last downturn in the oil market that you would have to deal with. Maybe we could jump to the founding of Durum Capital then. What was the opportunity that you saw in the marketplace and what led you to found Durum Capital?

Jay Simmons

So prior to Durum Capital, there were a couple chapters. I had a private equity firm that invested in companies that had something to do with deregulation of the power markets in Alberta. And we had done well with that firm. I'd made some money and basically had gone off on my own and was doing my own investing of my own dollars at that stage of the game.

It was me and an analyst, essentially investing my own dollars. We had sold a few companies at one time and a lot of them were startup in nature and fairly high risk ventures. And I had a couple little kids at home, and my wife and I decided that maybe we should take a little bit more of a conservative path.I was looking for more solid, secure assets and decided that real estate would be a good spot for me to try to focus.

I could use my personal strategic edge in being able to work my way through things that are in trouble, and restructure companies to navigate my way through some real estate that was in trouble. So there were a few different firms that we looked at. We did find one that had all kinds of problems with it. They'd completely run out of cash. And so I restructured that entity and that was the creation of Durum Capital. So these were longer, more mature, patient assets for me while I had little kids at home and had to be a responsible person for a period of time.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/