BTE Newsletter #20: A Liquidity Squeeze For Private Credit

Good morning everyone,

Those of you who know me best are aware that I am a Baltimore Ravens fan. The reason why is a long story, but I've been cheering for them just over 20 years now, which encompasses my entire adult life.

And last week, my team became the subject of widespread scorn and ridicule. This is another long story, but for those unaware, they entered into a trade agreement with the Las Vegas Raiders for star player Maxx Crosby. This was effectively a handshake agreement, and was not yet set in stone. So when Crosby failed a physical, the Ravens backed out of the deal, then quickly signed another top player at the same position. While the team was acting within its rights, detractors say that Crosby's medical condition was already well-known and the Ravens were acting in bad faith.

Ironically, private credit investors are asking for their money back too, in very large numbers. Not unlike the Ravens, they are also acting within their rights. And there are more parallels between the two situations: they are chaotic, unprecedented, and generating lots of catchy headlines.

Of course they're very different stories. But as someone who cheers for the Ravens and commentates on private markets, I can't help but see the irony and draw the parallels when these two things happen at the same time.

So if you're looking to read more about Maxx Crosby or the Ravens, you can find lots of material on ESPN. For the circus in private credit, my thoughts are below, and I should also have some more guest op-eds out soon. Stay tuned.

Ben

Some Thoughts on the Private Credit Liquidity Squeeze

For those of you unaware of the background, there have been a series of storylines since last fall that have cast private credit in a negative light. In each case, I wrote about it for this newsletter, arguing that the media was mostly being too harsh in its criticism:

- The collapse of First Brands and Tricolor, followed by Jamie Dimon's "cockroaches" remark.

- Blue Owl's aborted merger attempt of two private credit funds.

- The sudden share price drop for software companies, driven by AI-related fears.

- Blue Owl's latest moves with one of its private credit funds, OBDC II.

This last storyline in particular has led to a spike in redemption requests in private credit funds. In early March, Blackstone's private credit fund BCRED announced it would meet all requests, but only with the support of cash injections from the company's balance sheet and employees (see below for more detail). Then BlackRock announced that it would restrict redemptions on its private credit fund within its HPS subsidiary.

Last week the hits kept coming. Cliffwater announced that redemption requests on its private credit fund reached 14% of the total fund value, and that only half of these requests would be honoured. Morgan Stanley followed soon thereafter with a similar announcement. As of this writing (Sunday), we've yet to hear from Blue Owl itself.

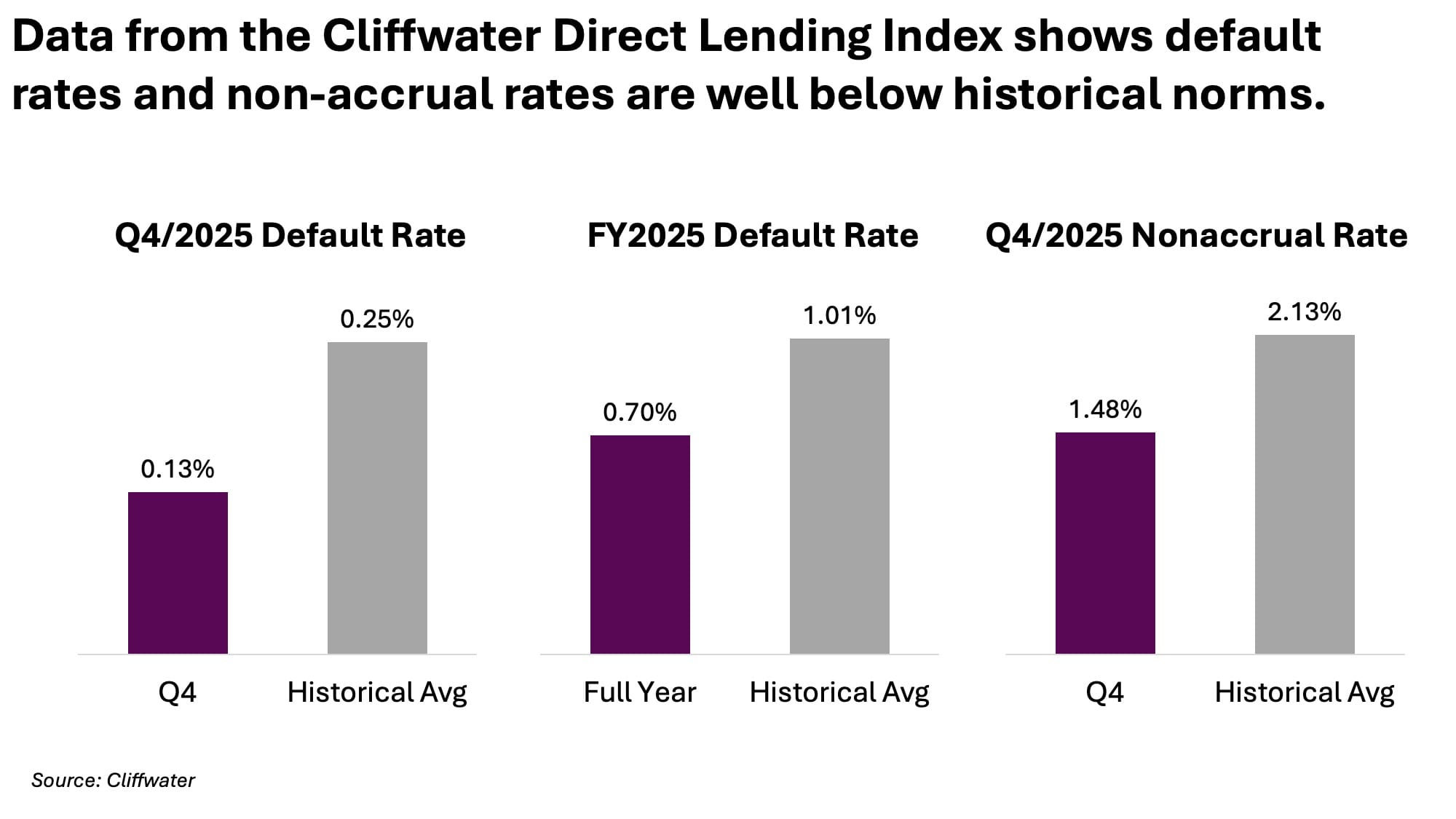

This is not caused by defaults or by performance

As private credit grew at a breakneck speed, the industry's biggest detractors warned that too much capital was chasing too few opportunities, and that this would lead to a loosening of underwriting standards, followed by a painful default cycle. But that has yet to materialize.

These results are even more remarkable given the pressure private credit has faced in recent years. Five years ago, interest rates hovered near zero, equity valuations were stretched, and inflation was on the verge of skyrocketing (as were interest rates).

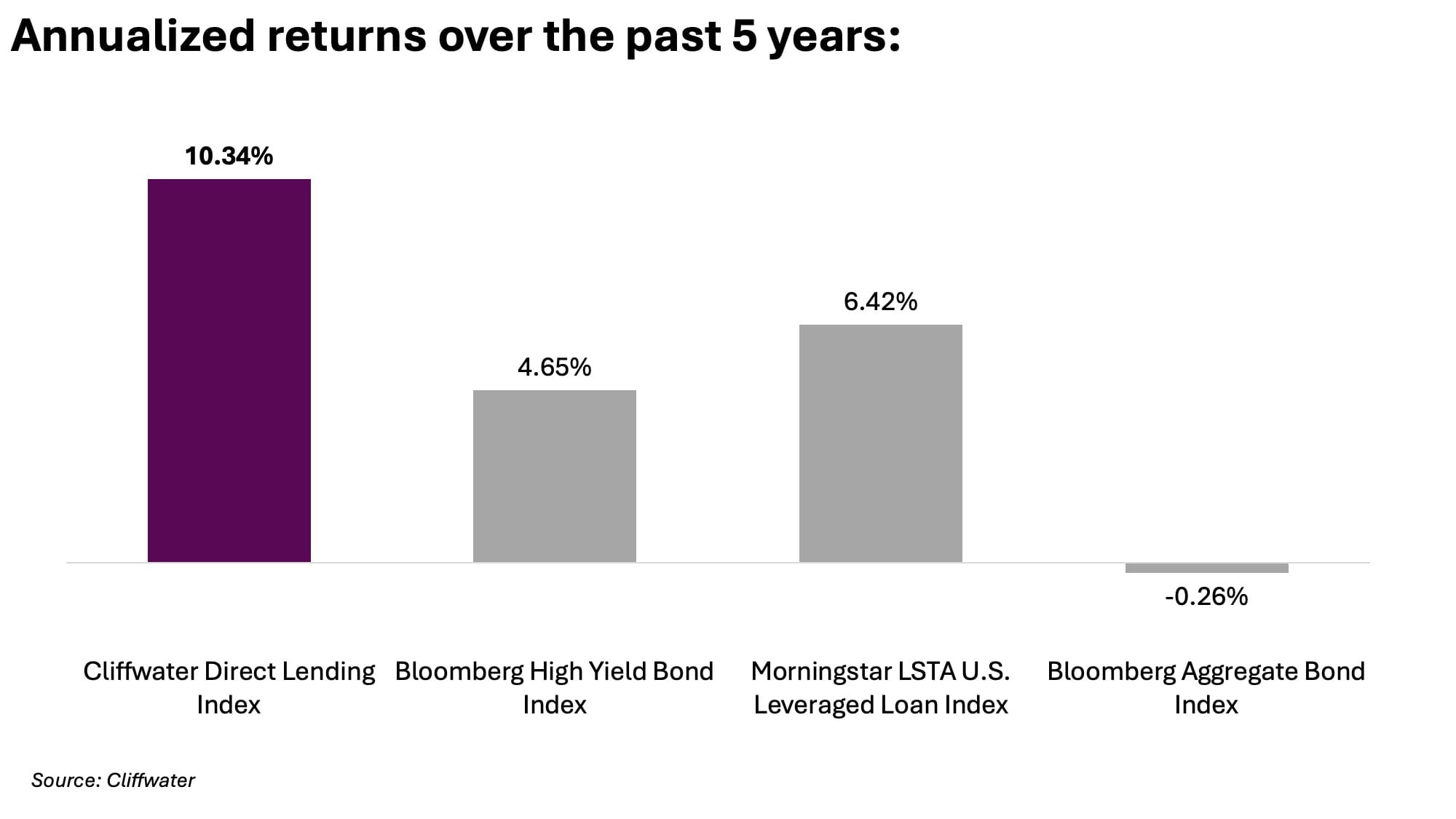

For an industry built on providing floating-rate loans to highly leveraged private equity-backed companies, it’s no wonder many expected a wave of defaults. Yet that reckoning never came. Now with rates easing again, private credit has not only weathered the storm but also delivered superior returns compared to traditional fixed-income asset classes (the chart below is as of YE2025).

How the Industry Can Respond to This

The irony of the current private credit shakeout is hard to miss. The industry is complaining that the headlines are divorced from reality, yet the headlines are also driving a difficult reality, as jittery investors respond by asking for their money back.

Still, there are some ways that managers can respond:

Don’t hesitate to gate.

Gating used to signal poor liquidity management, questionable valuations, or portfolio weakness. So up to this point, managers would typically pull out all the stops to avoid gating.

A perfect example occurred at the beginning of this month. Blackstone's flagship private credit fund BCRED was facing aggregate redemption requests exceeding 7% of the fund, which was higher than the 5% quarterly limit. But Blackstone was determined to meet all the requests, and avoid the fate that had befallen its real estate fund BREIT just a few years earlier. So BCRED got a US$400 million injection from Blackstone's balance sheet and employees.

But since then, redemption requests have been even higher at other funds managed by BlackRock, Cliffwater and Morgan Stanley. And all these funds responded by gating. None of these three funds had faced scrutiny prior to this month; it's clear they've been swept up in an industry-wide storm.

In a way, these funds are giving each other cover, and removing the stigma of gating. So with that said, firms shouldn't feel the need to do what Blackstone did.

Be opportunistic where others can’t.

When the private credit market expanded at a breakneck pace, there were legitimate concerns about looser underwriting and compressed spreads. Now the pendulum may swing the other way. Some funds are already trying to sell portfolios to meet redemptions, and liquidity is retreating just as financing needs remain high.

For managers with dry powder, this is precisely the setup that creates strong vintages: less competition, better terms, and assets trading at discounts. Whether through acquiring secondary portfolios or deploying fresh capital into a tighter market, selectivity and discipline may provide big rewards for opportunists.

Refine the message.

When I talk about private markets, I get the question all the time: "what happens if I want all my money back?" ... and the answer I give usually goes something like this:

"Under normal circumstances, investors have a chance to cash out once every three months. But if too many investors ask for their money back at once, they are effectively told to get in line."

I think that's quite a simple message, one that investors are able to digest, and it doesn't overpromise anything. But I suspect other investors got a message much more promissory. Perhaps the message didn't involve the possibility of gating, or if it did, it may have been accompanied by "but I don't think that will happen" or "that hasn't happened before for this fund". I suppose I can't prove this, but the recent wave of redemption requests signals that the messaging was too ambitious in some cases.

The good news is that now there's a real-world example that advisors can point to, and advisors can ask clients what they would do if the gates come up. If the answer is "it doesn't matter, I'm in it for the long term, as long as the investments perform I don't need my money back any time soon", then private markets may be much more appropriate.

This is a job for advisors first, but asset managers need to be part of the solution too. Because if they don't coach advisors to set realistic expectations, then that raises the risk of their own fund gating every time there's a new stress event.

What the Industry Will Look Like on the Other Side

As an advisor who focuses intently on this space, I am not upset by what's happening (whether you choose to believe me is another matter).

Put simply, this industry needs to get to a place where investors are realistic about what they're getting into. There also needs to be a filtering out of weaker managers. And there also needs to be better education/knowledge among advisors about these strategies. Once these things happen, the industry will be in a far better place, which I would be happy about not only as an advisor, but as a Canadian too.

If this episode helps bring the industry in the right direction, I'm all for it.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/