BTE Newsletter #19: AI, Conductors, and Meat Puppets

Good morning once again everyone,

Wednesday last week was the Innovation in Private Markets event, and for all those who attended, I hope you enjoyed it as much as I did. There was a good crowd and a lively discussion, with just enough disagreement between the panelists (more on that below).

As for the podcast, the full episode featuring Faheem Tejani and Ches Hagen of Capital Asset Lending is now live on both Apple and Spotify. Newsletter subscribers can download a transcript of all podcast episodes here.

In this episode, we covered the following topics:

- The background of both guests and their firms.

- What is a MIC?

- How do mortgages fit into an investment portfolio?

- What type of borrowers do MICs serve?

- What are some of the safeguards used by MICs to protect against losses?

|

|

Meanwhile, there's also a big developing story: private credit funds are under serious strain, in the wake of negative press surrounding Blue Owl. As I write this on the weekend, the latest development is BlackRock gating a private credit fund on Friday as redemption requests exceeded 9% of the total fund. By the time I write about this next week, I expect the story to have developed further.

Ben

The One Topic of Contention at the CAIA Event: AI, Conductors, and Meat Puppets

During the panel session at the CAIA event last week, a word was used to refer to the early adopters of private markets: conductors. Such advisors (I would consider myself to be one of them) are not looking for a turnkey solution such as a fund-of-funds; they are looking to pick their own investments, and they tie that into their brand.

I then brought up that 20 years ago, conductors may not have been picking their own private markets investments, but they were instead picking their own stocks or mutual funds. And one could argue that today, it's become far more difficult for advisors to differentiate themselves by selecting the best within these categories. Outperforming the market has become much more difficult, and put simply, investors have rightly become less willing to pay up for stock pickers.

So I asked the obvious question on stage. If I consider myself to be a conductor in private markets, will the same thing happen to me? Will I become more irrelevant, especially as AI levels the playing field between those who have more understanding/experience with private markets, and those who don't? Will I become a "meat puppet", as one panelist put it (presumably meaning someone whose intellect is irrelevant or nonexistent as AI does all the real analysis)?

This is where the opinions on stage started to diverge.

Why I May Become a Meat Puppet

One of the panelists made a very familiar argument, one that is being made in most other industries too: AI is coming for our jobs, and our analytical ability will eventually be practically obsolete.

Furthermore, private markets are beginning to look a lot more like stocks and bonds. There is already a vibrant secondary market for private markets assets, with over US$200 billion traded last year. Private assets are also being combined with public assets, either in single funds or as part of model portfolios, thus enabling much greater access. A newer trend is the advent of private market indices for evergreen funds, with firms such as MSCI, Morningstar and Cliffwater leading the charge. If the indices catch on, then one could start to see private markets derivatives, and/or ETFs. Meanwhile there are efforts to bring daily pricing to private markets funds, as part of initiatives to get private markets strategies into 401(k) retirement accounts.

The big question is whether one will eventually be able to invest passively in private markets, the way one can invest in the stock market through an ETF. If this does become possible, with AI helping advisors implement a passive strategy, it's not inconceivable that conductors such as myself will face some real headwinds.

Why Private Markets Are Different

While private markets are gradually looking more and more like public markets, the fact is there are still big differences, and true convergence is a long way off.

For starters, the subscription process is still very cumbersome, data is not centralized, and there are still big differences between the specifics of each fund. In many ways, we are still in the Wild West in private markets, requiring careful analysis to separate the good from the bad. There are also still big differences in private markets access at different investment dealers (and I consider Designed Securities, where I am, to be among the best).

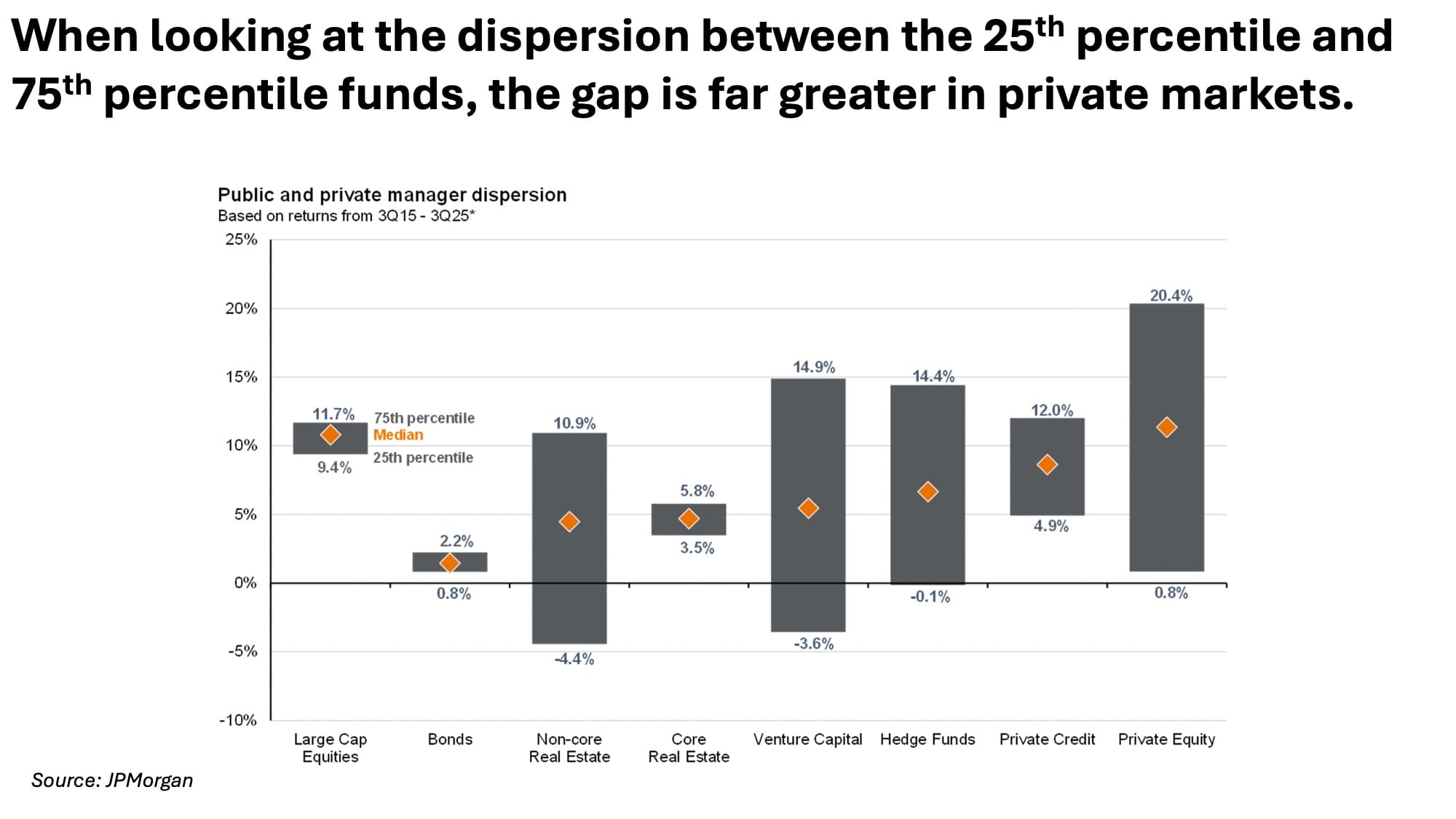

Furthermore, there is still a very wide performance difference between the best and worst funds; this gap is much larger than in public markets. So the stakes are much higher when selecting between funds, and the rewards for strong analysis are materially better than in public markets.

A Long Way Off

This ties back to the theme of the event: Innovation in Private Markets. And the fact is, there has been tonnes of innovation over the past 10 years, but there's still a very long way to go. So I may end up becoming a meat puppet eventually, but I don't have to worry about that for a long time.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/