BTE Newsletter #18: "selective reassurance from a commentator who is not a disinterested party."

Good morning everyone, and I hope your week is off to a great start.

First things first, this is the last call for the Innovation in Private Markets event put on by the Chartered Alternative Investment Analyst (CAIA) Association. The event takes place tomorrow at 4pm, and it's free and open to everyone. So if you'd like to attend, the sign-up link is here.

This week's newsletter features a preview of episode 8 with Faheem Tejani and Ches Hagen, both leaders at Mortgage Investment Corporations (MICs). It's the first episode with multiple guests, so I'm glad there were no technical hiccups. The full interview features topics such as:

- The background of both guests and their firms.

- What is a MIC?

- How do mortgages fit into an investment portfolio?

- What type of borrowers do MICs serve?

- What are some of the safeguards used by MICs to protect against losses?

I hope to have the full episode released on Sunday, subject to approval from compliance of course. In the meantime, as always, you can follow along here:

|

|

Ben

Some Thoughts on the Blue Owl Back-and-Forth

On Monday last week, I got my first op-ed published, so a big thank you to Investment Executive and Advisor.ca for working with me. I look forward to writing lots more.

The article was about Blue Owl and their ongoing saga in private credit, a subject that has received plenty of commentary in the past few months, including a couple of times in this newsletter (here and here). In this case I felt the press had been quite harsh in its criticism of Blue Owl (and not for the first time) to the point that the narrative had become distorted, and the company seemed alone in its own defence. So I thought a piece highlighting some counterarguments in support of Blue Owl would be useful.

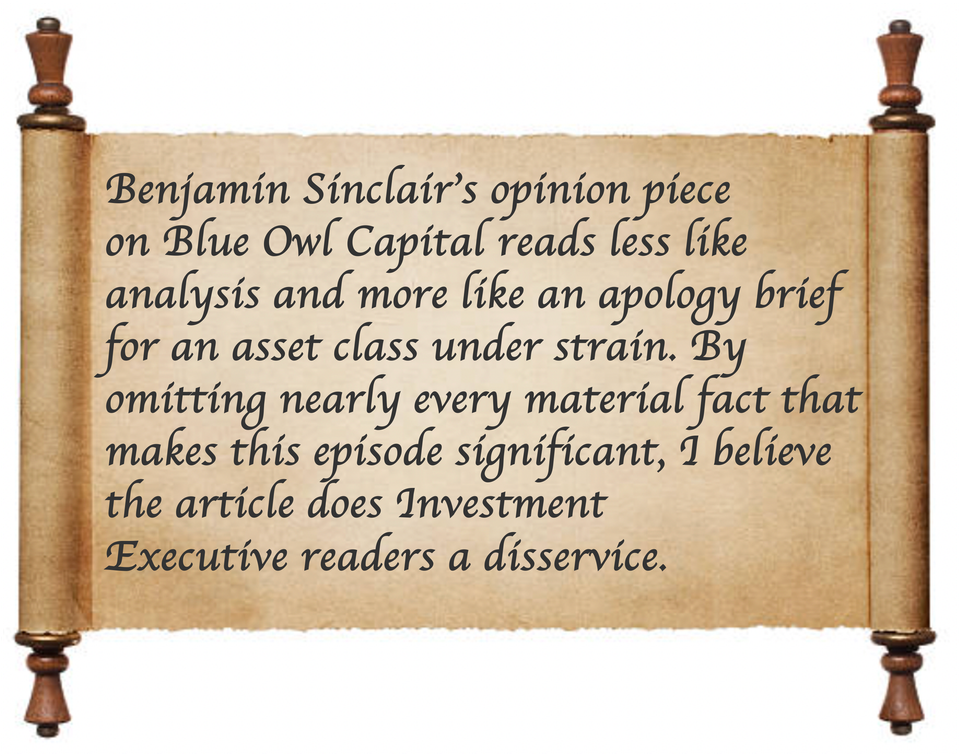

Others disagreed. In particular, there was a scathing rebuke published the next day, which is where the title and feature image of this newsletter came from.

As should be clear by now, I'm not looking to shy away from this, even when some of the language is quite aggressive. After all, that's the internet, so if I'm sharing my opinion in these arenas, I should be able to handle some criticism too. And while I'm at it, why not have a little fun too? I certainly enjoyed making the scroll.

As it relates to Blue Owl, I don't feel the need to publish a rebuke to the rebuke. I view some of his arguments as distorted too, as he views mine, but I'll let him have the last word.

The fact is, this story is quite complicated, with a lot of nuances. No article is going to capture the entire story on its own, without being a massive essay. But if you're just looking for a couple viewpoints, you can see my article on Advisor.ca or Investment Executive, and you can read his rebuttal by typing the words from the scroll into Google.

Faheem Tejani , Capital Asset Lending &

Ches Hagen, AP Capital (Preview)

Ben Sinclair

In this episode, we have a first with multiple guests, both leaders in the private mortgage space. First, we have Faheem Tejani, President at Capital Asset Lending, which provides non-traditional mortgages for single-family homes in Ontario. We are also joined by Ches Hagen, CEO at AP Capital, which also provides non-traditional mortgages for single-family homes, but this time in Western Canada. Faheem and Ches, thank you very much for joining me.

So Faheem first, can you tell me a little bit about your background and how you got into the mortgage space?

Faheem Tejani

Great, well thank you very much Ben, for having me on your podcast. I look forward to having this discussion with Ches.

So I actually started my career in investment banking. In my former life, I actually took a company called EQ Bank public. Back when I took them public in 2004, there was no income verification for banks. It was pretty much equity-based lending, which is what we do today. A friend of mine had started a business. He was a mortgage broker, a successful mortgage broker, and he had gotten into the lending space in 2009. And we connected in 2013.

What I was able to bring was the capital markets functions. So helping to put a board in place, getting introductions to banks, as well as facilitating some investors putting in capital. And so I've been involved in this business since 2014. And then I moved full time. I left my job at the bank in 2018 and I joined as President in 2018 at Capital Asset Lending. We've been around since 2009. As you mentioned, we're focused on Ontario only single family homes. And we have north of $1.2 billion in assets.

Ben Sinclair

And Ches, same question for you.

Ches Hagen

Thanks Ben, thanks for having me. I'm Ches Hagen, AP Capital. I'm one of the co-founders of the firm. We started AP back in 2007. My background actually is more in the technology sector. So when I finished post-secondary, it was dot-com bubble days. At that point in 1999, 2000, it was a matter of “you gotta be in tech.” So I went into the world of technology.

The way in which I then pivoted into the world of lending, which we do here at AP Capital, is that I maximized my RSPs. I invested them in mutual funds. I was quite frustrated with mutual fund performance. And one of my best friends from almost high school days was a mortgage broker. I called him up one day, and I said, "Hey, how do I get my RSPs out of mutual funds and into real estate?" because he and I had owned some real estate and done well with it.

And he said, "Well, let's start a MIC." My answer was "What's a MIC? I'm looking for a place to invest. I don’t want to start something." I'd already sort of been in that tech world. So that was the birthing of AP Capital, almost by accident you might say. And so he had the real industry experience. I had a little bit more of the willingness to kind of roll up my sleeves and dot the I's and cross the T's on on the governance side and the side of developing the business out.

So in the early days, he really focused on lending, I really focused on capital raising, and it's been a story of 18, almost 19 years of developing it from the ground up, you might say.

Ben Sinclair

Can you answer your own question now? What is a MIC?

Ches Hagen

Well, it was developed in the 1970s by the federal government. They thought that Canada needed some more mortgage options, so they created the Mortgage Investment Corporation. Essentially, it's a financial institution that's unlike a credit union or a financial institution called a Schedule I bank in that we don't take deposits and we don't offer checking accounts or credit cards.

Rather, we take investment dollars from investors and then we turn that into a pool of funds that we then can advance in the form of mortgages. There's a definition around the Canadian Tax Act that tells us what we can and cannot do as a MIC but a couple of those primary things are that we can only lend on Canadian real estate, and we have to be a going concern operator with a vast number of shareholders. We are registered fund eligible so we can take RRSPs and TFSAs.

Maybe I'll pause there because I can get really windy but essentially we are a lender that's unlike banks and credit unions for real estate, primarily residential real estate in Canada only.

Ben Sinclair

Why don't I bounce it back to Faheem then for another question which may have a long-winded answer. Can you tell us about the case for investing in mortgages?

Faheem Tejani

One of the benefits of mortgages is when you look at it as an alternative investment it's a very easy asset to understand. Most people have experience with mortgages. So that makes it very easy when you're speaking to an investor, they appreciate what they're investing in.

When you look at it, the appeal is you get equity-like returns, but you don't have the volatility of equity markets. So if you think about MICs or Mortgage Investment Corps, they're really fixed income vehicles. You get a steady stream of income. Most of us pay monthly distributions on or about the same time in the month.

Most of us have static NAVs, so if you think about portfolio volatility, it reduces portfolio volatility while still giving you an attractive return. And then the other thing is, because we're in the residential mortgage space, the residential real estate market is probably the most liquid market. Aside from condos, if you look at single family homes in general, it’s a very liquid asset class compared to other asset classes in real estate such as commercial, such as industrial.

For example, if a house is anywhere between $600,000 to $1 million, there are lots of people that can afford that type of house. It's when you get into higher-end homes or higher-end mortgages where there are fewer people that can buy those. And that's why when you look at it, you're getting liquidity, you're getting a premium over where GICs are, and you're getting equity-like returns for little to no volatility.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/