BTE Newsletter #17: In (Mostly) Defence of Blue Owl (Part 2)

Happy Tuesday everyone!

First off, we are now just over a week away from the Innovation in Private Markets event put on by the Chartered Alternative Investment Analyst (CAIA) Association. For those of you who will be in downtown Toronto on March 4th (Wednesday next week), you can follow the sign-up link here. There's no charge for attending.

I also recorded episode 8 of the podcast on Friday, and it was the first episode featuring multiple guests. Thankfully there were no technical issues, and it was a lively discussion on investing in mortgages. I hope to have that one ready within a couple of weeks. If you never want to miss an episode, you can subscribe below:

|

|

Finally, an exciting update on my advisory practice. I have joined a Toronto-based chapter of The Entrepreneur Nation®, which is a networking group for white-collar professionals. The group features a commercial litigator, a forensic accountant, insurance specialists, a real estate agent, a mortgage broker, and a class-action lawyer, among many others.

As it relates to this newsletter, I will always make it about Private Markets, but there may be opportunities to highlight the other members. And if you think the group would be a good fit for you, please let me know.

Ben

In (Mostly) Defence of Blue Owl (Part 2)

Late last year, Blue Owl found itself in hot water when it proposed a merger of two of its private credit funds (OBDC and OBDC II). The proposal would have effectively required investors in OBDC II to take a 14% haircut. Those investors pushed back, Blue Owl backed off, and it generated some bad press for the company. I wrote about the saga in late November.

The news hasn't gotten any better for Blue Owl since. Earlier this month, the selloff in software providers engulfed Blue Owl due to its heavy exposure to software in its lending portfolio.

Then on Wednesday last week, Blue Owl issued a press release announcing the sale of US$1.4 billion of private credit assets. This sale occurred across three funds, including US$600 million from OBDC II, accounting for over a third of that fund's assets. Blue Owl also announced that going forward, the fund will "prioritize delivering liquidity ratably to all shareholders through quarterly return of capital distributions." Some have interpreted this as an outright restriction on redemptions.

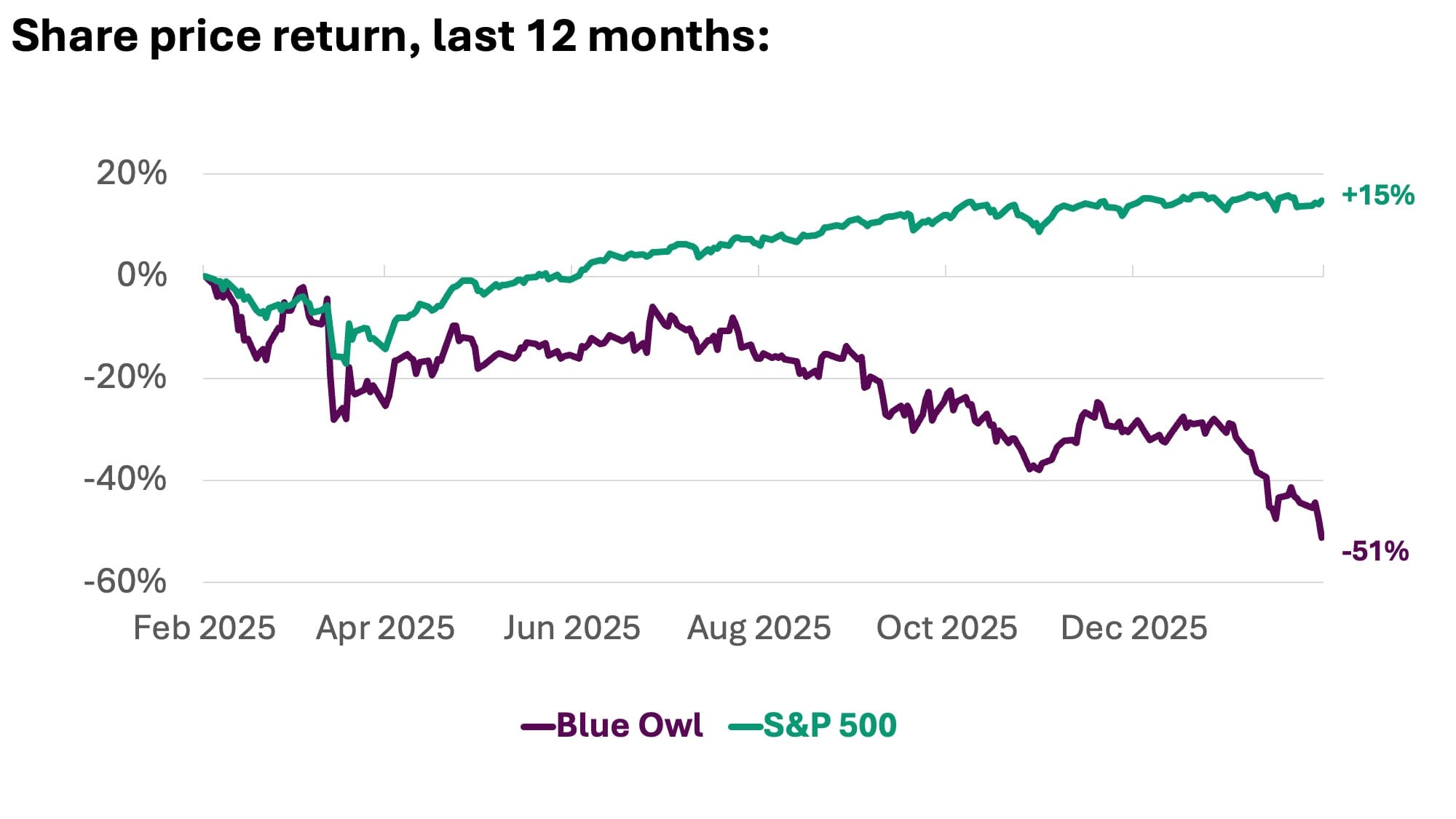

The reaction was swift, with Blue Owl shares tumbling by more than 12% over the next two days amid a flurry of negative headlines. As of the end of last week, the stock was down by more than 50% over the past 12 months.

This isn't nearly as bad as the headlines suggest ...

According to Blue Owl, the media has completely mischaracterized this event, and the company has a case. Below are key clarifications on what actually happened and why the situation isn't nearly as severe as the headlines make it out to be:

- OBDC II is a closed-end fund, meaning it has an end date and an eventual need to provide liquidity to investors. This could be accomplished in one of three ways. One is bringing the fund public, which investors had already resisted last year. Another option is a gradual runoff as loans are repaid, which would take many years. The third option is selling down assets and returning cash, which is what management has chosen. By selling such a large chunk of loans, Blue Owl has significantly accelerated capital return to investors relative to option #2, a far cry from the narrative of dried-up liquidity.

- Related to point #1, Blue Owl plans to continue returning significant capital to OBDC II investors this year, and believes half of all capital will be back by year-end. The distinction is this will be done proportionately to all investors in the fund, rather than through tender offers (in which each investor indicates their interest). This is very different from the experience that other funds have subjected their investors to when gating.

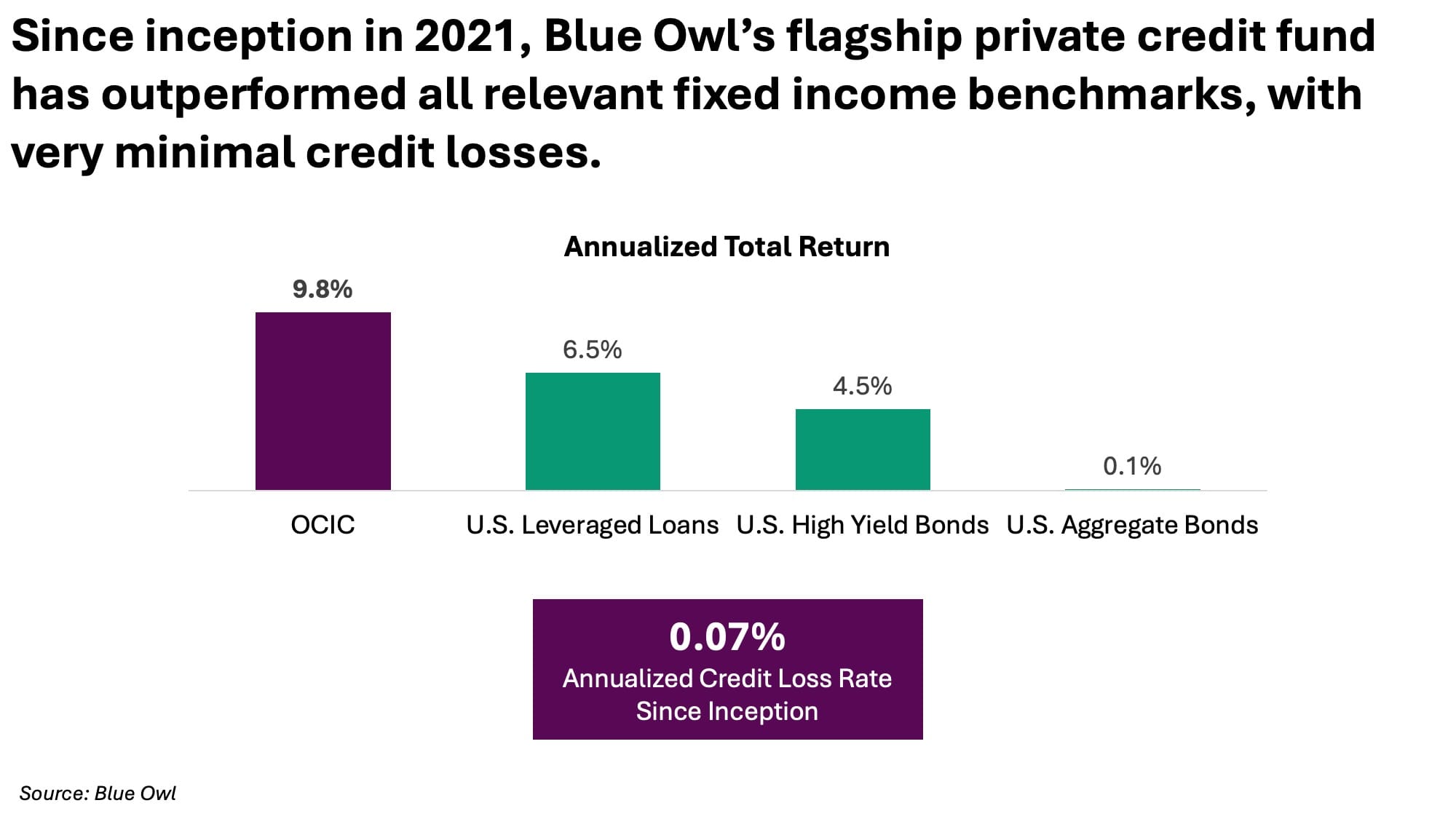

- Blue Owl's largest private credit fund (OCIC) is entirely unaffected, and this is the fund that is marketed to Canadian individual investors. In fact this fund has seen net inflows every quarter since inception in 2021, again a big contrast to funds that are having trouble meeting elevated redemptions.

- OCIC's performance has been solid, whether measured by overall returns or by default rates.

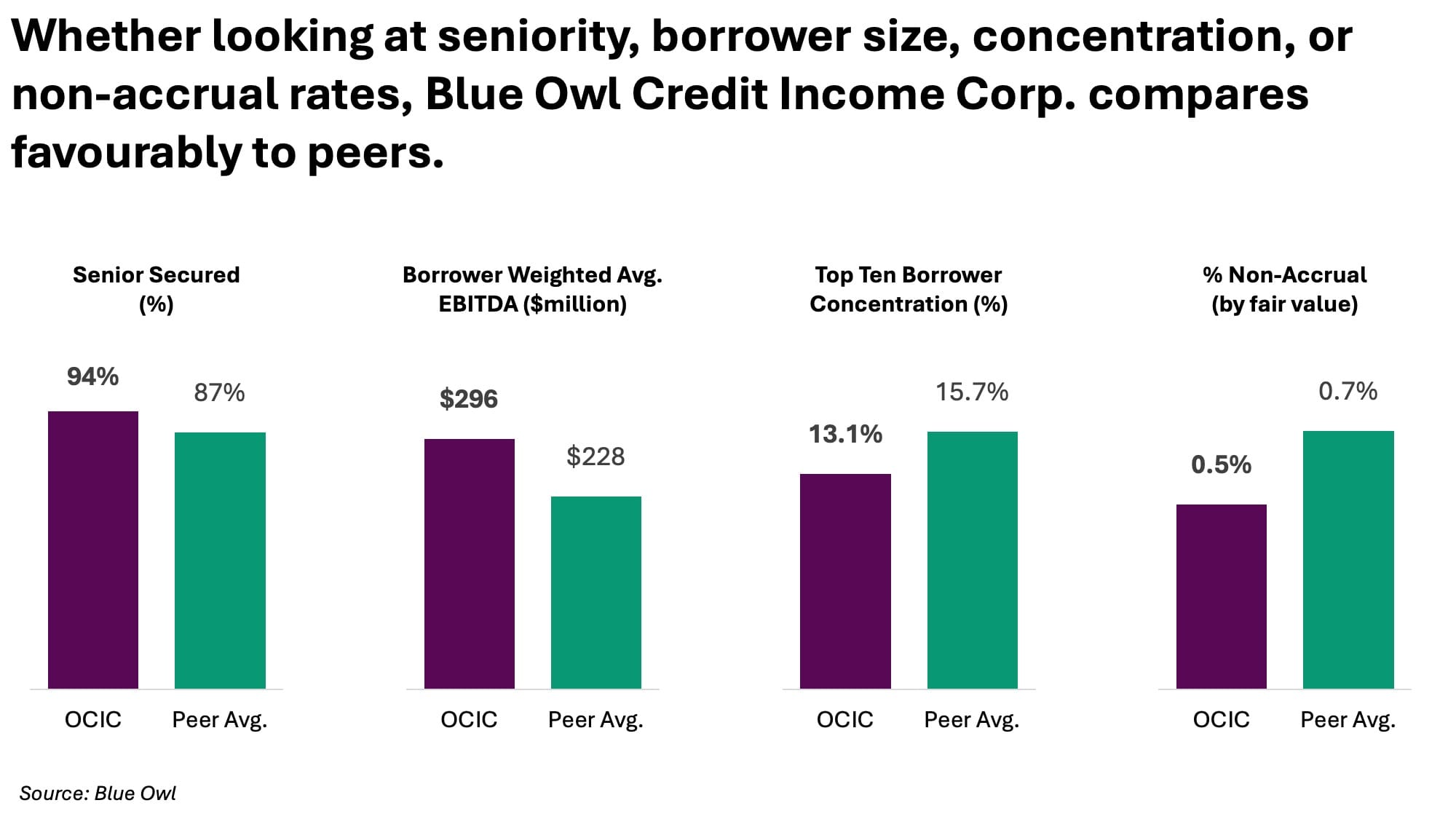

- OCIC's portfolio remains quite healthy based on various measures.

- Blue Owl was able to sell a large chunk of loans at net asset value. The company also claimed that demand was strong enough for a significantly larger sale if one was needed. Again, this stands in stark contrast to gated funds, in which cases the managers typically cite the lack of a liquid market for their assets.

“We're in an environment now where there's a high degree of skepticism about private credit. And unfortunately, that skepticism can be amplified by folks that aren't even in private credit and don't spend any time in the industry and don't hesitate to forward things and amplify them in a way that makes them seem more prominent that they are.”

Craig Packer, Co-President, Blue Owl

... but there's a bit more to the story.

With all that said, there are a few points that investors should keep in mind, and these are points that Blue Owl is not as keen to make:

- There is an argument that Blue Owl cherry-picked its best assets to sell, and that's why Blue Owl did not have to accept any discount when selling the assets. For the record, the company claims this is a gross mischaracterization.

- Blue Owl is still facing the problem that its publicly-traded vehicle (OBDC, not to be confused with OBDC II) trades at a discount of 23% to net asset value, as of the end of last week. It's difficult to make the case for investing in a private credit fund at net asset value when one can invest in OBDC at such a wide discount.

- The company seems to have lost control of the narrative, and has miscalculated the media's response. Arguably this is not the first time that's happened. There's a strong case this happened last fall as well, with the failed merger between OBDC and OBDC II.

- If sentiment ever gets bad enough, then Blue Owl would have to restrict redemptions on OCIC. Arguably this is still a long way off, but redemption activity is largely out of Blue Owl's control, and the past week has not helped. It's something for investors to think about before committing to this fund.

The Big Takeaway

There are a lot of nuances to this story, but the main lesson is one that comes up again and again: private assets come with unique risks relative to publicly-traded securities, and if an investor is not able to handle illiquidity, then they should stay out of illiquid assets.

There's another lesson, and that is the importance of controlling the narrative. If a publicly-traded company loses investor confidence, and the stock price declines, there will typically be a chance to prove the doubters wrong over the long term. But when investors in a private markets fund sense danger, and believe that redemptions will spike, that can easily be a self-fulfilling prophecy.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/