BTE Newsletter #16: Is the SaaS-Pocalypse Coming For Private Markets (Part 2)?

Hello again, and Happy Wednesday! Because of the long weekend, this issue is a day later than usual.

A gentle reminder for those of you interested in innovation in private markets: I'll be moderating a panel on the subject on March 4th at 4pm. The event will be at Vantage Venues in downtown Toronto. Anyone interested can let me know, or you can follow the sign-up link here. There's no charge for attending.

Regarding the podcast, episode 7 has now been released, featuring Josh Will of Virtus REIT. In the interview, we discuss (among other things):

- His background and the origin story of Virtus

- How Virtus approaches the real estate market, looking for distressed sellers and overlooked assets

- Some unique perspectives on fundraising, as well as the current "troubles" facing the private real estate space

- His answer to a question from the previous guest, David Gens of Merchant Growth

|

|

Finally, in last week's newsletter I touched on the "SaaS-pocalypse", in which worries about AI disruption have caused software company (and alternative asset manager) stocks to plunge. I promised that the next newsletter (i.e. this one) would discuss it further. So here it is.

Ben

What to Make of the "SaaS-Pocalypse"

Software-as-a-Service companies have long been regarded as some of the best businesses in the world, with highly-recurring revenue, sticky customer relationships, minimal capital expenditures, and very high incremental margins.

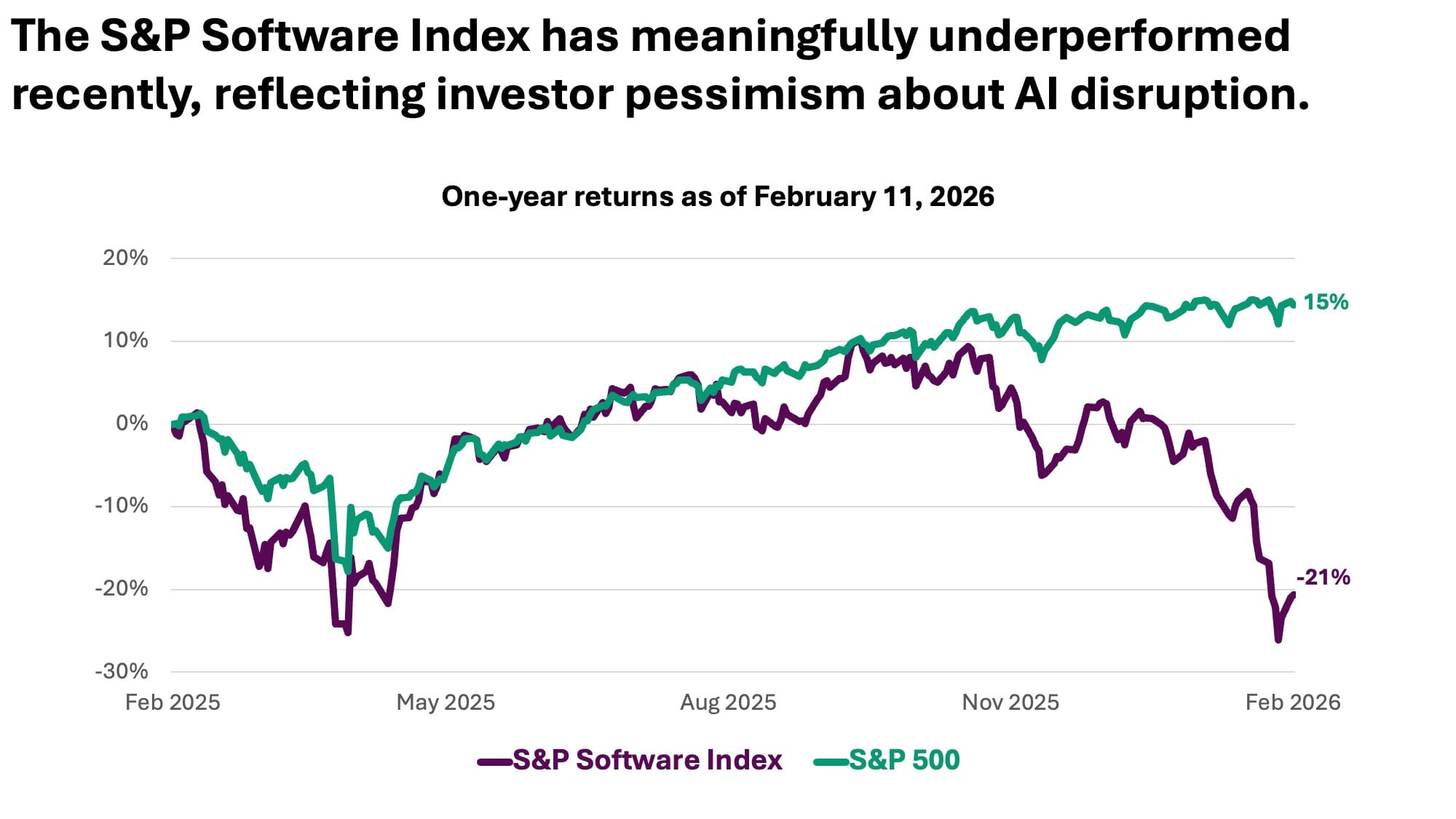

But since the launch of ChatGPT, investors have been questioning what AI means for the future of SaaS. In a worst-case scenario, companies could use large language models or AI-native upstarts to replace the work previously done by legacy SaaS providers. Those murmurs grew louder last fall as SaaS stocks began to meaningfully underperform the S&P 500. Then in early February, Anthropic’s release of a Claude plugin capable of document review and legal analysis marked another turning point, and it triggered a broad selloff across the SaaS sector. In an ominous note, Goldman Sachs strategist Ben Snider warned that the worst may be yet to come.

"One lesson from historical examples of industries facing disruption risk is that share price stability requires stability in the earnings outlook. Newspapers, for example, faced risk from technological disruption as the internet grew in the early 2000s. The share prices of the group declined by an average of 95% between 2002 and 2009."

Ben Snider, Chief U.S. Equity Strategist, Goldman Sachs

The selloff has spread to alternative asset manager stocks as well. These firms have been active investors in the SaaS sector, which aligns well with private equity and private credit due to its predictable, recurring revenue models. In private equity specifically, where leverage tends to be higher than in public markets, the downside impact can be more pronounced.

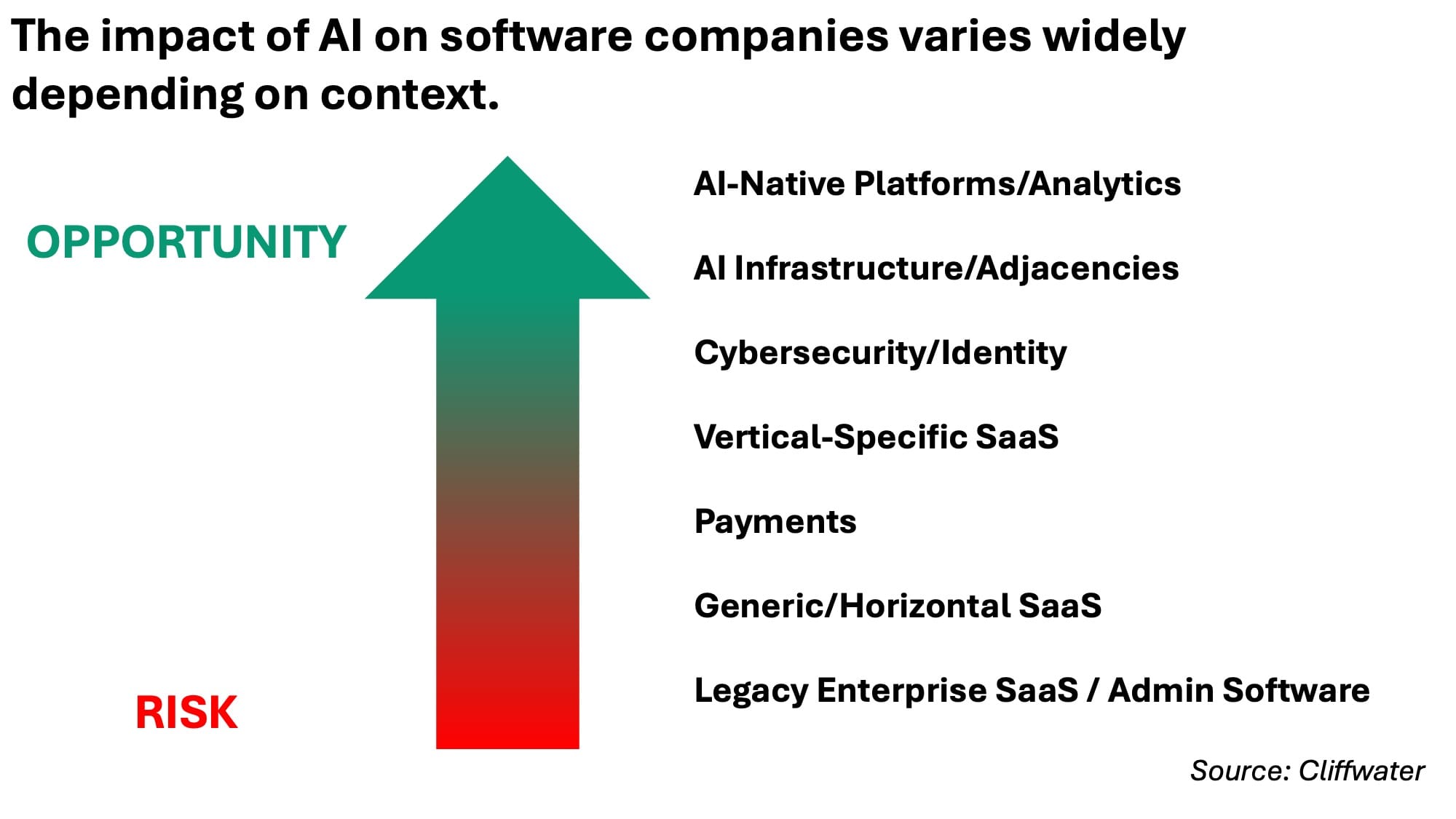

Even so, several mitigating factors suggest that investors, including Mr. Snider, may be overreacting. It is true that some SaaS companies will face meaningful disruption, but many are well positioned to adapt. And for the strongest players, the rise of AI agents represents not a threat, but a major opportunity.

Why the Best SaaS Companies Have So Much Staying Power

High Switching Costs

Anyone who uses software in a workplace setting knows that ripping out existing systems is a tremendous pain, and in many cases practically impossible. The disruption to daily operations, the training required for staff, and the inevitable implementation hiccups all create strong inertia in favour of the status quo.

This effect is more powerful when software is deeply integrated into existing workflows. Once a platform is connected to other tools, automated processes, and reporting systems, replacing it is no longer just a matter of buying a new license. It becomes a complex project involving IT resources, change management, and operational risk, which raises the bar for any potential new vendor. This is especially the case for software that supports a specific industry (so-called vertical market software).

Switching costs are higher still when software controls proprietary data. The risk of data loss or misinterpretation further discourages companies from moving away from incumbent providers, even when new solutions appear more innovative or cost-effective on the surface.

Security and Governance

Security and governance are central to the value proposition of established software providers, particularly in environments where errors or breaches carry serious consequences. Vendors that can demonstrate robust security practices and a reliable track record are therefore at a significant advantage. This becomes especially important in sectors such as financial services, healthcare, defence, and the public sector, where sensitive information and mission-critical operations are involved.

As a result, organizations are often reluctant to experiment with unproven tools for core workflows, even if the technology appears more advanced. This creates a powerful moat for incumbent SaaS vendors that have already invested heavily in regulatory alignment, and it makes displacement by newer AI-native tools much harder than it might first appear.

Vendor Consolidation Over Point Solutions

A growing number of organizations are choosing to consolidate around a smaller set of software vendors rather than stitching together a patchwork of point solutions. This shift is driven by a desire to reduce integration complexity, lower vendor management overhead, and simplify security and compliance reviews.

This trend plays directly to the strengths of established vendors. They typically enjoy deeper, longer-standing relationships with decision makers in procurement, IT, and business leadership, which gives them a built-in advantage when contracts come up for renewal or expansion.

Scale further reinforces this position. Larger incumbents have the resources to invest aggressively in AI features, or to acquire the most promising upstarts and integrate them into their existing suites. This allows them to respond to competitive threats while still presenting customers with a single, unified platform. In a world where buyers increasingly value simplicity, security, and strategic partnerships, that combination can be another powerful moat against new AI-native entrants.

The Opportunity for SaaS Companies From AI

AI features can become a meaningful new source of revenue for SaaS companies. Instead of simply enhancing existing functionality, AI can unlock entirely new modules, premium tiers, and add-on services that customers are willing to pay for. Examples include intelligent assistants embedded in workflows, automated document drafting and review, or smart recommendations that materially improve efficiency or decision-making. In many cases, these features can be priced separately from the core product, creating an incremental revenue stream on top of existing subscriptions.

Over time, this is likely to evolve into outcome-based pricing models, where customers pay not for access to software, but for the value it delivers. Rather than charging a flat fee per seat, vendors can price based on tasks completed, documents processed, leads converted, hours saved, or other measurable business outcomes. This aligns incentives more closely between the vendor and the customer, and it reduces friction for adoption, since buyers can tie spending directly to realized benefits.

If AI allows software to take on more of the actual work, rather than just organizing or tracking it, the economic pie gets a lot bigger. The addressable market is no longer limited to what companies are willing to spend on tools for their employees. It expands to include a share of the labour and process costs that AI can automate or augment. For SaaS providers that successfully design and execute outcome-based pricing models, this could translate into structurally higher revenue potential and deeper integration into their customers’ operations.

Private Markets Companies Are Especially Well-Positioned

Concerns about AI disruption have increasingly been directed at private markets managers as well, but in many cases this concern looks misplaced.

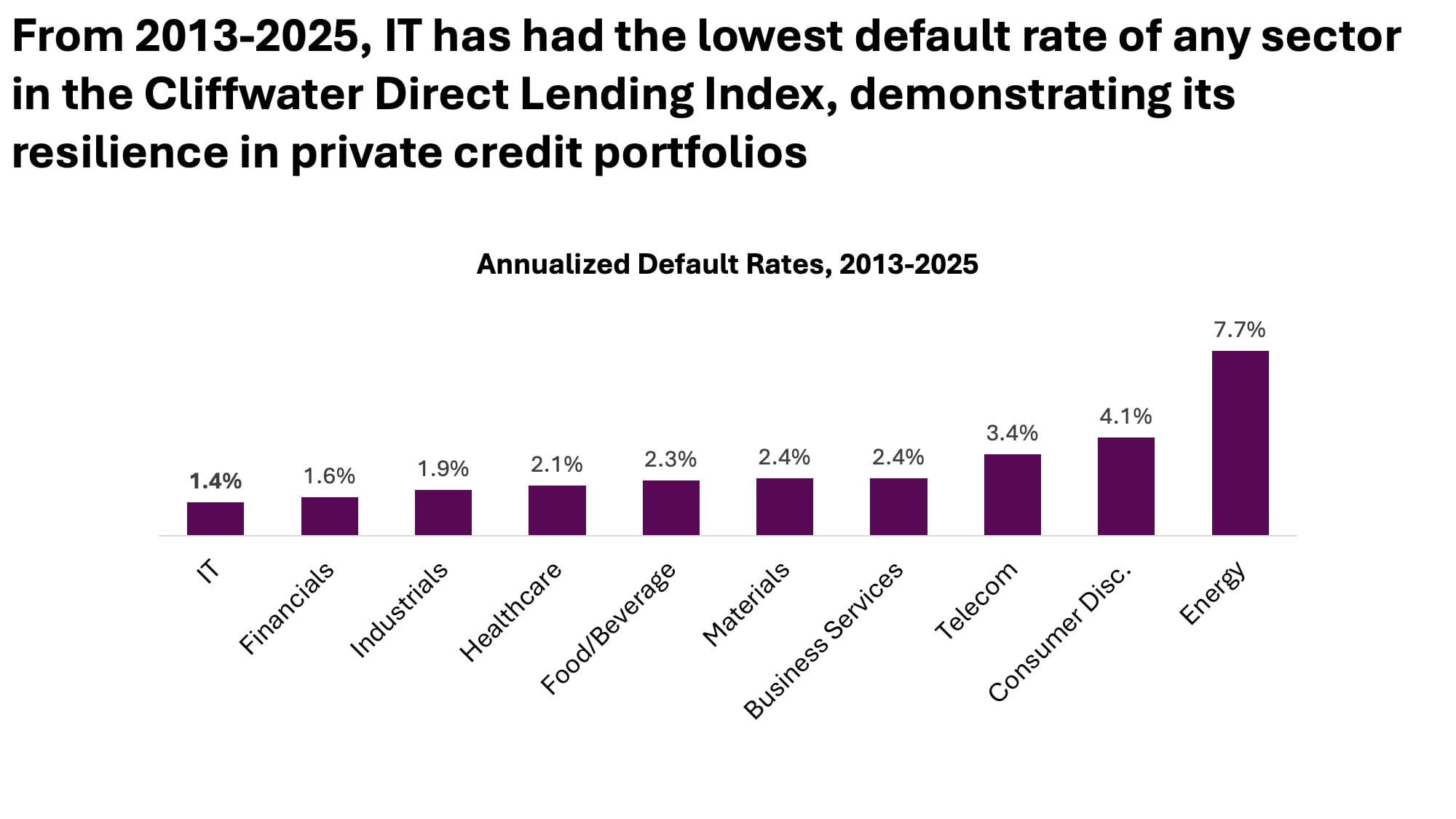

On the credit side, the worries appear particularly inappropriate. Private lenders to software companies typically structure loans with conservative terms, including low loan-to-value ratios that are often below 40 percent, which provides a substantial cushion against valuation shocks. These software credit portfolios have historically been among the most resilient performers, in part because lenders focus on recurring revenue, retention, and cash flow visibility when underwriting, rather than headline growth stories. Even in a world where AI introduces new competitive dynamics, those core attributes remain highly relevant to credit quality.

On the equity side, private equity sponsors bring capabilities that can help software companies navigate and even capitalize on the AI transition. Leading sponsors provide strategic guidance, operating playbooks, and dedicated resources that support product repositioning, pricing changes, and AI feature integration. These firms were thinking about AI, automation, and data-driven products well before the launch of ChatGPT, and they now act as conduits for best practices across their portfolios.

Some of the most thoughtful perspectives on AI in software have come from private equity companies such as Vista and Thoma Bravo, whose entire franchises are built around investing in software businesses. For companies backed by sponsors like these, AI is less an existential threat and more a new chapter in a long-running value-creation playbook. In this context, Ben Snider's analogy to newspapers seems particularly misguided.

"If you don’t have sovereignty and dominion over workflows and datasets, you don’t have a right to exist as an enterprise software company."

Vista Equity Founder/CEO Robert Smith

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/