BTE Newsletter #15: Is the SaaS-Pocalypse Coming For Private Markets (Part 1)?

Hello again, and Happy Tuesday!

I have some exciting news to share! In early March, I'll be moderating a panel at a CAIA event in downtown Toronto. The event will be at Vantage Venues, at 150 King St West on the 27th floor. If you'd like to join, please let me know and I can add you to the list.

In the meantime, last week we saw a slew of earnings releases come out from the alternative asset managers, and the market reaction was decidedly negative. I should have more to say on this next week (there will be no podcast to preview, so I can dedicate the whole space to it), but I've got some initial thoughts below.

I've also edited episode #7 of the podcast with Virtus REIT President Josh Will. A preview is below, and the full episode should be released this weekend (subject to compliance approval as always). And to make sure you never miss an episode, as always you can subscribe here:

|

|

Ben

The "SaaS-Pocalypse" and Alternative Asset Managers

Last week saw a flurry of earnings reports from alternative asset managers, and the market reaction was not exactly positive. On Thursday, Blue Owl stock fell by nearly 4% after reporting earnings. On the same day, TPG fell by more than 4%, KKR fell by more than 5%, and Ares fell by 11%. The market had already reacted negatively to Blackstone's earnings the previous week, sending those company's shares down by 3%.

Even before earnings were released, shares in the space had done quite poorly. The VanEck Alternative Asset Manager ETF is now down by 12% on the year. So what's going on?

Well, a big reason concerns the so-called "SaaS-Pocalypse", in which AI is increasingly seen as a disruptive threat to enterprise software companies. For instance, this image is from a Forbes article on Wednesday, and shows the 7-day stock price performance for some of the hardest-hit companies:

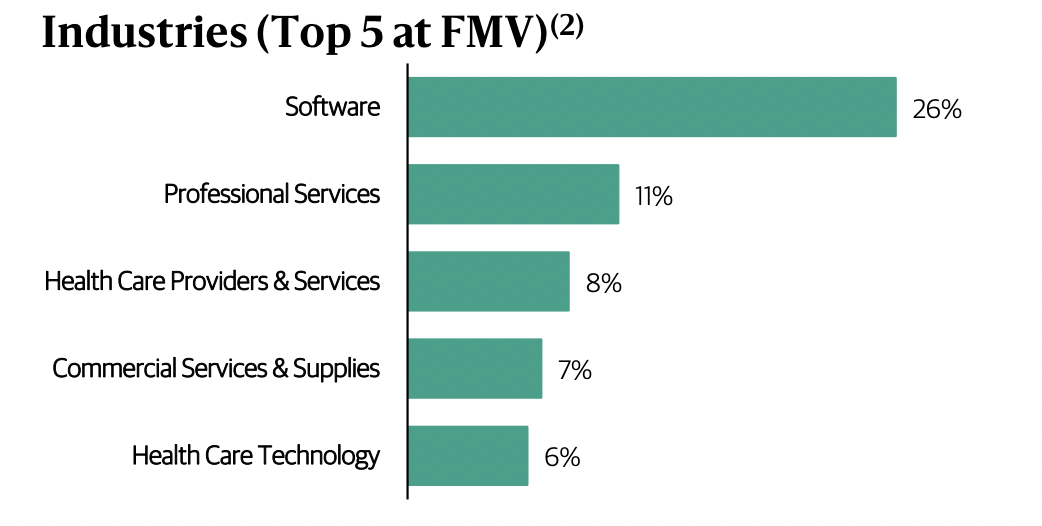

As it to relates to alternative asset managers, these companies invest heavily in enterprise software, both on the private equity and the private credit side. For instance, this chart shows the top 5 sectors in the Blackstone Private Credit (BCRED) fund, which is the largest private credit fund in the industry:

During the conference calls, the alternative asset managers made various arguments about why these fears are overblown:

"We don't have red flags and point of fact, we don't have yellow flags. We actually have largely green flags. The tech portfolio continues to be the most pristine amongst all of our portfolios, amongst all of our subsectors."

- Marc Lipschultz, co-CEO, Blue Owl

"Software is about 7% of our AUM, and that is with, I would

say, a highly inclusive definition of software. And so our concentration is well below our industry, well below broad equity and credit

indices. And the market right now, and as you know, this happens when there's this much emotion all at once, is painting everything

with one brush. We would just caution that not all software investments are the same."

- Scott Nuttall, co-CEO, KKR

"They sit at the center of companies' tech stacks. They manage complex workflows. They benefit from ownership and collection of proprietary data that they've built over many years with diverse customer bases. They operate in highly regulated industries like health care and financial services. So again, it is interesting to see how the markets are thinking about software companies as all being equal and not really understanding the difference between companies that could get disrupted by AI in places like digital content creation or data analytics and visualization versus like real entrenched enterprise systems."

- Michael Arougheti, CEO, Ares

There are a couple other things worth pointing out:

- When it comes to private credit, software loans are typically very senior in the capital structure, with quite low (<40%) loan-to-value ratios. So there would need to be very significant asset impairment before these loans go bad, as Mr. Lipschultz pointed out during the Blue Owl conference call.

- In many cases, AI will be a benefit to software. It can save on software development costs, make salespeople more efficient, and unlock new revenue streams. The key for any software company is to be adaptable enough to embrace AI, and also to be irreplaceable for its clients. For instance this could come from proprietary data, or from operating in a highly regulated environment.

All told, there will certainly be disruption from AI in the software space, but the market seems to be painting a broad brush on this trend. In the case of alternative asset managers, the market also seems to think these companies will be blindsided, which seems especially unfair. In many cases, it's the alternative asset managers that are the best sources of the latest trends.

I'll have more to say on this next week.

Josh Will, Virtus REIT (preview)

Ben Sinclair

Joining me today is Josh Will, president of Virtus, which operates a diversified real estate fund focused on quality cash flowing properties in secondary and tertiary markets across Canada and the United States. At Virtus, Josh's primary role is to develop and execute sales and marketing initiatives to grow the Canadian investor network. Josh has over 15 years of experience holding executive positions at international marketing and investment firms, all in the private real estate space. Josh, thank you very much for joining me.

Josh Will

Thanks for having me today, Ben.

Ben Sinclair

So Josh, you heard me introduce you there, and I was wondering if you could give me a little bit more colour on your background and how you ended up at a place like Virtus.

Josh Will

Yeah, sure.

I think I have a similar story to a lot of people as they look back on 20 years being in a career and they go, “how did I get here?”. It's kind of like that talking head song from the 80s.

I actually went to school to become a teacher. That was supposed to be my career path. I had a passion for history and philosophy and geography and all that. But the time was about 2002, 2003, and there weren’t a lot of jobs for teachers in Ontario. So I did what a lot of young people did at the time, I went to Western Canada because that was where the oil boom was happening.

And this is kind of a long story, Ben, but basically I had this massive student loan and no career prospects. So I needed to go where the opportunity was, and that was to go work in the oil patch. And I was lucky enough to land a gig pretty quick. I mean, the pay was good back in those days and I was able to pay off my student loan relatively quickly.

And the one thing that I noticed about Calgary and Alberta at the time is that it was a land of opportunity and I was a recent grad. So I literally just threw on a nice shirt, clean shoes, went around to various investment firms, oil companies, all that kind of stuff, looking for an office job because I was educated and looking to learn.

I ended up getting a job basically in the mail room of this land-based real estate investment company that bought raw land in the path of future growth. And I worked there for about seven years, always in a marketing capacity, learning about how to market investments, market real estate investments, market exempt market securities, private stuff. And a lot of the Canadian private markets industry started out in Western Canada because of the oil and gas boom.

Ben Sinclair

So you were there during the financial crisis then, what was that like for you?

Josh Will

That was a whole other thing actually. Imagine selling US-based real estate in 2007 through 2009. Those were tough times. Let's just start there. We were a sales firm and an investment firm, and we had to quickly pivot into a marketing firm and let people know that this too shall pass. As you know, markets are cyclical and there is always light at the end of the tunnel. It's not always a freight train.

And we were able to bear down. Obviously we had to make some very difficult decisions internally to cut costs and things like that so we could weather the storm. And at the company I was at, they did a great job with that.

They were able to do that and they're still operating today. But it was a trying time. I mean, it's not unlike many other cyclical dips we've seen. Even this year in real estate, it's taking a lot of tongue lashing in the papers and in the media. I'd say it's almost comparable to that time 15 years ago. Actually, 17 years ago now, I guess.

Ben Sinclair

Can you tell me about the origin story of Virtus?

Josh Will

Virtus is an interesting story. I think we all have an interesting story about how businesses start, and the peaks and valleys throughout the timeline.

So the company's actually been around since 1985. My partner Aurelio [Baglione] started the company in 1985 or 1986 under a different trade name back then. He's an Italian person. So he changed the name to Virtus, which is an Italian term for strength, commitment and integrity. The guy holds himself accountable to that and that's what he named the company after.

I was lucky enough to partner with Aurelio in 2018 because I used to have my own exempt market dealer and I was in the market to sell it, because I wanted to just focus on asset management. And that's when I met a number of different individuals that I looked at selling the firm to. Ultimately, it was Aurelio that came in and said, “why don't we partner together and start our own REIT?”. And that's what we did. So we started a REIT at the end of 2019, the start of 2020.

If I can digress here and tell you a little bit about our launch, that was pretty interesting. So we decided to partner in 2019. It took a little while to get everything set up, and we had a big investor presentation. I think it was at Morton's downtown. There were going to be about 50 people there, all of the accredited investors that had been with us along the way. And it was set up for Thursday, March 19th, 2020. As you can imagine, that event never happened, because three days prior to that was when Ontario shut down and that was the beginning of the COVID lockdowns.

So we pretty much fell flat on our face from a capital raising standpoint in 2020 and didn't raise any money that year. And then going into 2021, things started to open up. As you can recall, people were getting back to going outside, getting in their cars, and driving places. So we went back out to market and started raising some money and started the REIT then. And it's been a pretty interesting journey for these last five years.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/

</span