BTE Newsletter #14: When Private Markets Goes Wrong, Part 2: Private Credit

Hello again,

I’ve got a few exciting updates to share. Episode 6 of the podcast featuring David Gens from Merchant Growth, a firm providing financing solutions to small businesses, is now live on Apple Podcasts and Spotify. For those who missed it, I shared part one of our conversation in last week’s newsletter.

And just this past Friday, I recorded episode 7 with Josh Will of Virtus REIT, where we talked about the company’s approach and key trends shaping the real estate market. Stay tuned for its release soon.

|

|

Also in last week’s newsletter, I put out a couple feelers about writing more guest articles and doing more events, and I’m happy to say there are already some leads on both fronts. I should have more to share soon.

In the meantime, I’ve talked before about how the media often paints private markets in a negative light. And to be fair, casual readers could easily think I’m doing the opposite, always putting a positive spin on (or simply selling) the space. So as I look to write more for mainstream publications, it's time to show (once again) that I am perfectly willing to shine a light on the dark side of private markets too.

Late last year, I shared a couple of cautionary stories from the private real estate world. Now two recent private credit stories are giving private market skeptics even more fuel. Time to dive in.

Ben

The Case of TCPC

BlackRock is the world’s largest asset manager, with more than US$14 trillion in assets under management as of the end of 2025. While it’s best known for its iShares suite of ETFs, the company has been increasingly expanding into private markets, announcing three major mergers in the space during 2024.

However even before these deals, BlackRock was already active in private credit following its 2018 acquisition of Tennenbaum Capital Partners. Unfortunately, that deal has reportedly struggled. According to a Financial Times report last year, one anonymous source described the integration as a “disaster.”

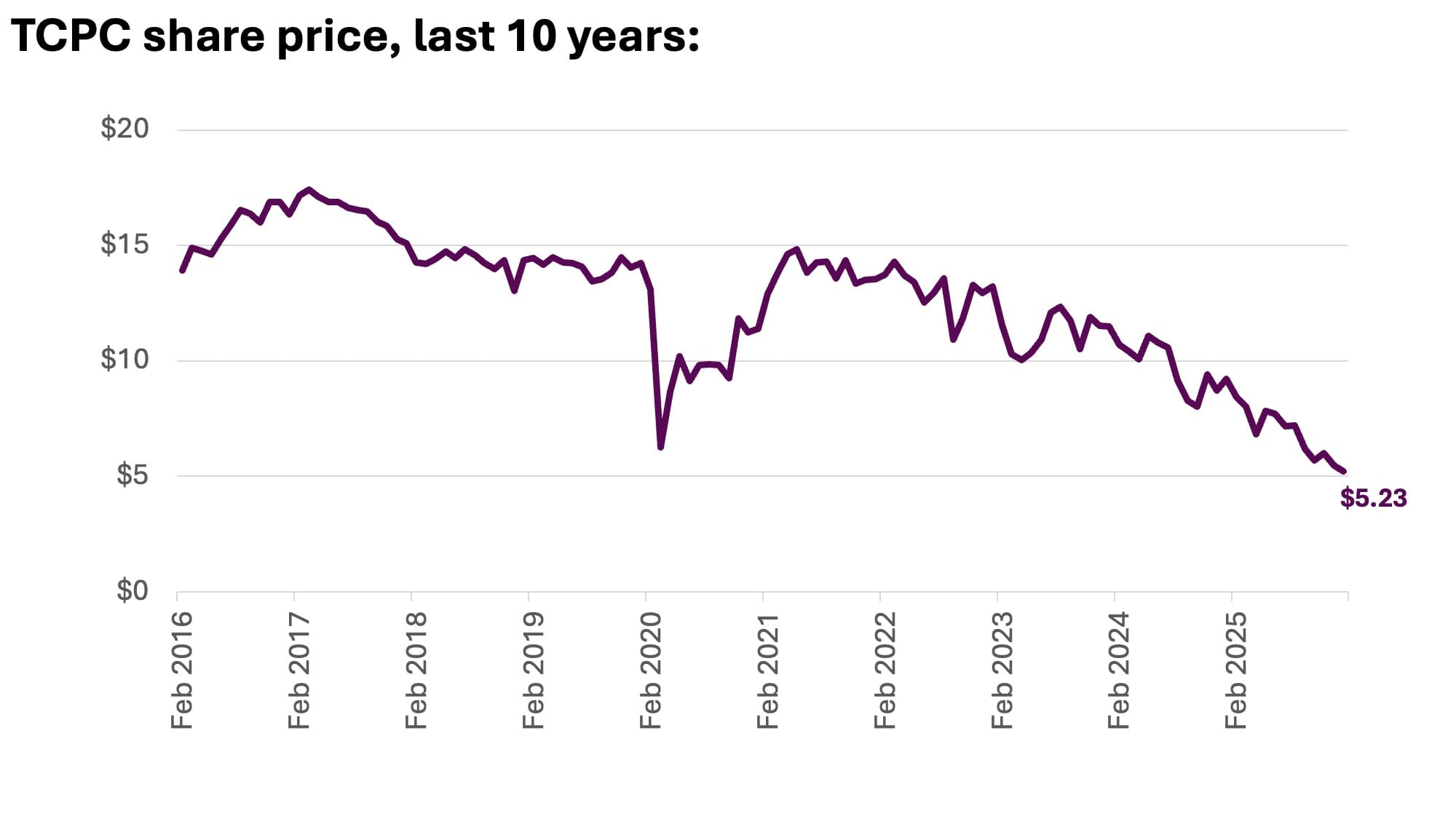

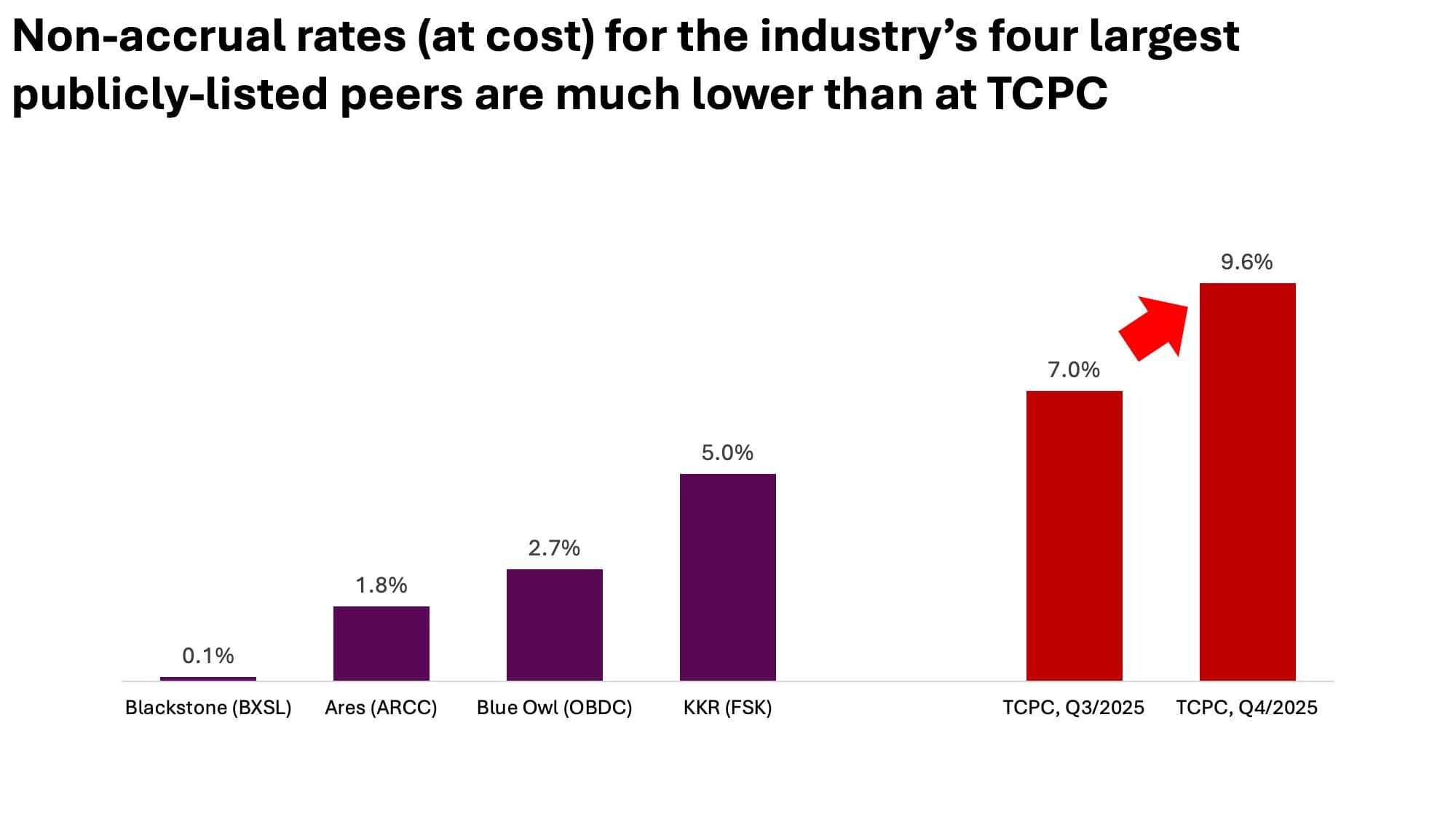

Perhaps the best illustration of this saga is the Nasdaq-listed BlackRock TCP Capital Corp. (ticker: TCPC), which has drastically underperformed since the Tennenbaum acquisition. The fund's tilt toward higher-risk loans has resulted in a significantly higher level of non-accruals than the industry average, and the stock’s performance has reflected that weakness:

The latest development has uncovered more problems. TCPC released an SEC filing on January 23rd warning that the fund's net asset value declined by approximately 19% in the fourth quarter of 2025, as the fund's non-accrual rate jumped from 7.0% of loans (at cost) up to 9.6% during the quarter. Both these numbers are well above comparable statistics for the fund's peers.

TCPC now trades at a 27% discount to its net asset value, after its stock price plunged 13% in response to the announcement. To BlackRock’s credit, the firm reduced its management fee on the fund by one third for the quarter, although this is small comfort for TCPC’s shareholders.

When TCPC releases its full earnings later in February, investors can expect a very lively discussion during the conference call.

The Case of An Unnamed Canadian Private Credit Fund

As a Canadian investment advisor, I prefer not to pick public fights with domestic asset managers, so I’ll keep this fund’s name private. However, in January another Canadian private markets fund suspended investor redemptions, and unlike most others, it wasn’t in real estate but in private credit.

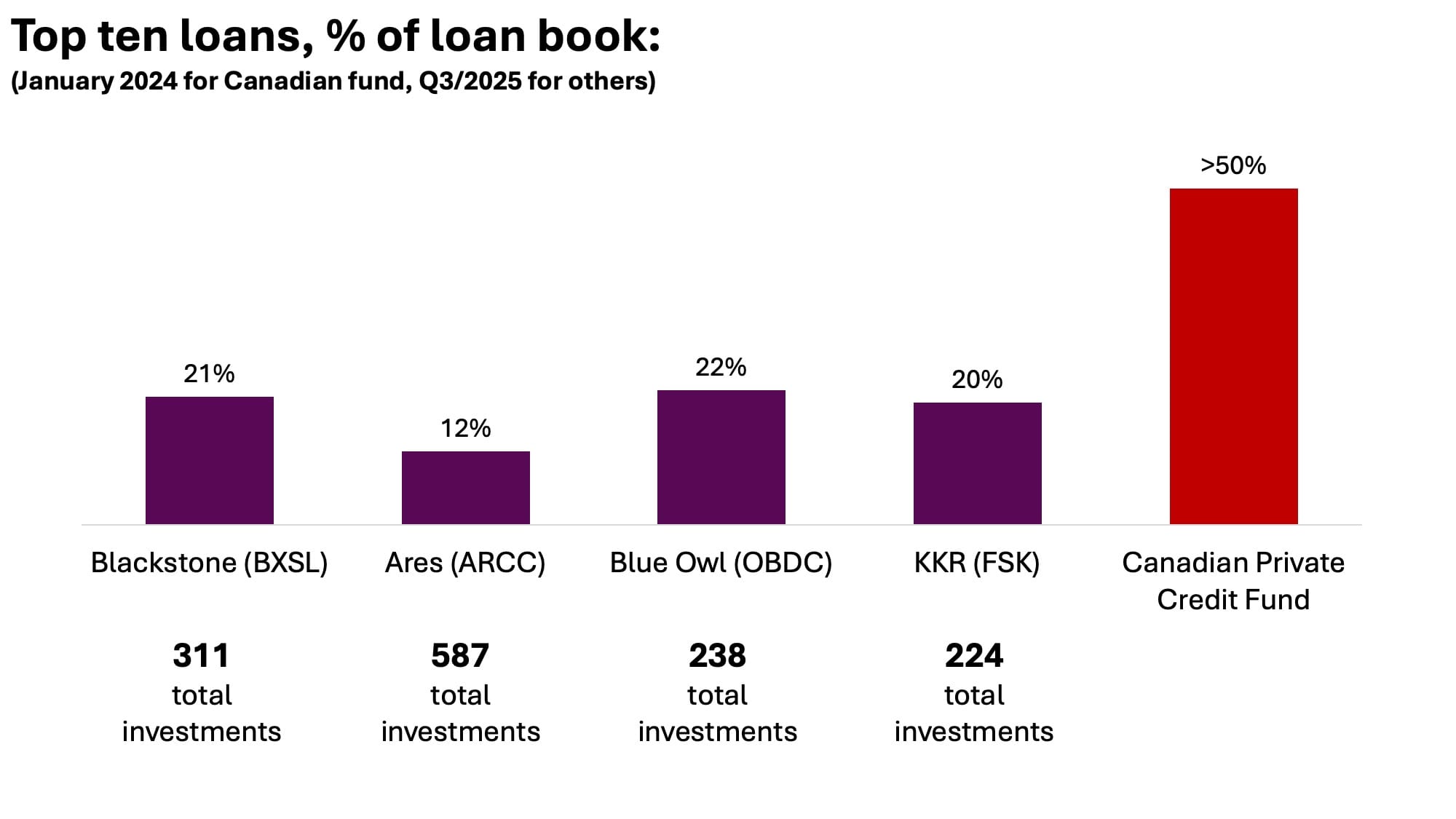

The fund’s main issue stemmed from a single large loan to a company building a diesel refinery. When that company filed for creditor protection in 2023, the impact on the fund’s portfolio metrics was of course very significant, and it also attracted some bad press. According to one report from The Globe and Mail, this borrower represented more than 20% of the fund’s total loan book across three loans. Just as concerning, the fund's top ten loans (including those three) made up over half of the portfolio as of January 2024.

Fast forward to January 2026, and the fund has halted investor redemptions, citing "an overweight single name concentration" in its fund, according to another Globe and Mail report.

This brings up a critical lesson: in credit investing, diversification is especially critical. Unlike in equities, there is no opportunity for a single big winner to offset losses; the best possible outcome is simply receiving principal and interest as promised. That asymmetry makes it difficult to recover from a poor investment, so the most effective protection is to limit concentration risk in the first place.

When looking at the largest publicly listed private credit funds in the United States (the same ones cited earlier), one can see they're far more diversified than the Canadian private credit fund:

Ultimately, this comes down to discipline. When a credit fund encounters an investment opportunity that is too large for its size, the prudent approach is to fund only a portion of the loan alongside other investors (or to walk away entirely). Doing so might result in fewer assets under management and a smaller bottom line. It could mean turning away investor capital. To be fair, that is not an easy decision to make.

However when looking at the large American funds, this issue has clearly been managed a lot better. It helps that the funds are backed by very large companies, thus providing access to robust deal flow, so the funds do not need to rely on a handful of oversized loans to deploy capital. It also helps that these funds represent only a small portion of the their managers' overall assets under management, reducing the incentive to stretch concentration (and reputation) limits in pursuit of growth.

That being the case, Canadian managers still need to raise their game when competing with their American counterparts, as this story unfortunately illustrates.

Dispersion Incoming

In my recent 2026 outlook, I wrote that “the era of easy money in private credit seems to be over, and when weaker platforms stumble, critics will no doubt claim victory.” It’s fair to expect that the latest headlines will add fuel to that narrative, which might make it tempting to avoid the topic altogether as I continue making the case for private markets in investor portfolios (regular readers are undoubtedly familiar with my pitch at the bottom of every newsletter).

But that would miss the point. Stock pickers don’t believe every company is worth owning; they apply discipline and analysis to find their favourite investments. The same principle applies to private markets: success depends not on avoiding the asset class, but on distinguishing quality managers and strategies from those that won’t stand the test of time.

Want to find out more?

Private markets are not for everyone, and come with a number of risks, such as higher illiquidity and less transparency.

However, many of the world’s leading institutions and wealthiest families put a big emphasis on private markets, and recently these strategies have become more available to individuals too. Drawing on my background as an analyst specializing in private markets, I help investors cut through the complexity and understand how to build portfolios incorporating these strategies.

To explore whether these strategies are suitable for you, please schedule a 30-minute virtual meeting below:

|

Email

|

Phone

|

LinkedIn

|

Apple

|

Spotify

|

Disclaimer

Benjamin Sinclair is a representative of Designed Securities Ltd. Designed Securities Ltd. is regulated by the Canadian Investment Regulatory Organization (ciro.ca) and is a Member of the Canadian Investor Protection Fund (cipf.ca). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Benjamin Sinclair is registered to provide advice and solutions to clients residing in the province of Ontario. For more information, please see www.beyondtheexchange.ca/disclaimer/

</span